8 / 28

8 / 28

Page 8

— Office Properties Quarterly — July 2015

Market Update

T

he Colorado Springs office

market was crawling slowly

out of the recession for the

past several years and finally

is reaching a point of stabili-

zation and growth. There are a cou-

ple of key components to the market

that are critical to understanding

future trends.

First, in all three office submar-

kets – central business district, north

Interstate 25 corridor and the airport

area – a significant portion of the

overall product type was constructed

in the mid-1980s, and the general

consensus of the marketplace is one

of “tiredness” for these buildings.

This perception has two distinct

responses by the market; the first

of which is downward pressure on

lease rates as landlords must get

aggressive economically to compete

and buy tenancy. The second is an

overall flight to quality whereby

tenants are gravitating toward the

newer, higher-quality assets.

In some ways, we are in the

middle to end of a marketwide shift

wherein many of the historically

competitive buildings in the office

market have become functionally

obsolete. These properties either

will become owner-user buildings

going forward or stagnate until they

are repurposed. This movement

toward new, higher-quality build-

ings that we have seen over the past

five years has an adverse effect on

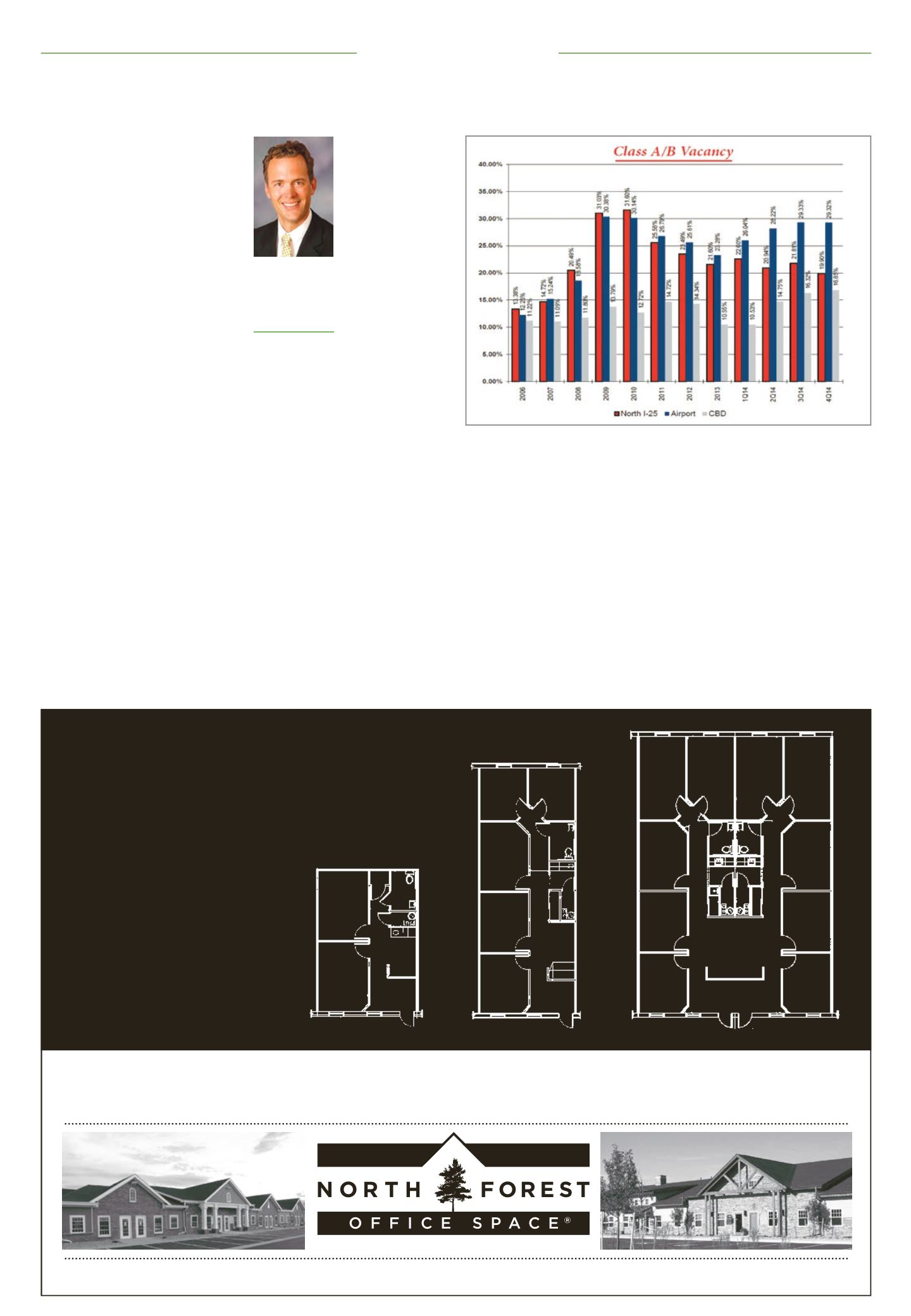

the vacancy numbers, which aver-

aged 20 percent vacancy between

2009 and 2014. In reality, when we

break out the truly competitive sub-

set of office buildings in each of the

submarkets, the

vacancy rate is in

the 12 to 14 percent

range and dropping

(albeit at a modest

pace).

The other compo-

nent affecting the

market is the dis-

crepancy between

the lease rates that

are acceptable to

the landlord (mar-

ket rates) and the

cost of the tenant

improvements,

which seemingly

have increased at a noteworthy pace.

When looking at the total Class A

and B office market, consisting of

approximately 9 million square feet,

the current average asking lease

rate is $13.20 per sf triple net. Note

that this rate is an average and does

include a handful of buildings, about

15 percent of the total market, that

are priced in the sub-$10 range in

order to attract value users who are

not as quality concerned.

With tenant improvements in the

$25 per sf range and in many cases

(certainly for first-generation space)

construction costs climbing well into

the mid-$40s per sf, simple math

dictates that these are transactions

that any prudent landlord would not

execute. While on the surface this

seems like a problem easily solved

by either the tenant coming out of

pocket for TI, the lease rate increas-

ing or an amortization into the lease

rate, this stumbling block is causing

disruption in the deal cycle. It may

be several months before the market

adjusts and accepts these costs ver-

sus rate discrepancies and the solu-

tions become acceptable as “the new

market.”

As we look into the future of the

office market for Colorado Springs

with the affects of the two afore-

mentioned trends, we predict a

continued strengthening market

for landlords and a tighter, more

competitive and less tenant-favored

environment for users. The vast

majority of the tenant activity in the

past several years was from compa-

nies with a local presence expanding

and relocating within the market-

place.

As we move through 2015 and

beyond, we anticipate additional

job growth from new companies

relocating and expanding into Colo-

rado Springs. Given the demand

for the higher-quality product and

the increase in TI costs, we antici-

pate continued rent increases and

a growing gap between the higher-

and lower-quality buildings. While

Colorado Springs never will reach

the velocity of markets like Denver,

the lease activity, absorption and

overall market demand is steadily

increasing and all indications are for

that momentum to increase into the

foreseeable future.

s

Colorado Springs market stabilizes, looks to growPeter Scoville

Principal, Cushman

& Wakefield/

Colorado Springs

Commercial,

Colorado Springs

At North Forest Office Space, we make leasing easy.

We offer affordable lease rates and guaranteed pricing with no hidden costs and upscale amenities.

Your clients can lease what they need today, and then add space as they grow.

Professional, medical and dental space in Brighton, Commerce City, Westminster, Firestone & Thornton • (303) 862-6367

• northforest.comDENVER • BUFFALO • ROCHESTER • AUSTIN

Offer your clients

office space

that grows

with them.

Courtesy Cushman & Wakefield