13 / 28

13 / 28

July 2015 — Office Properties Quarterly —

Page 13

Market Drivers

Courtesy Cresa

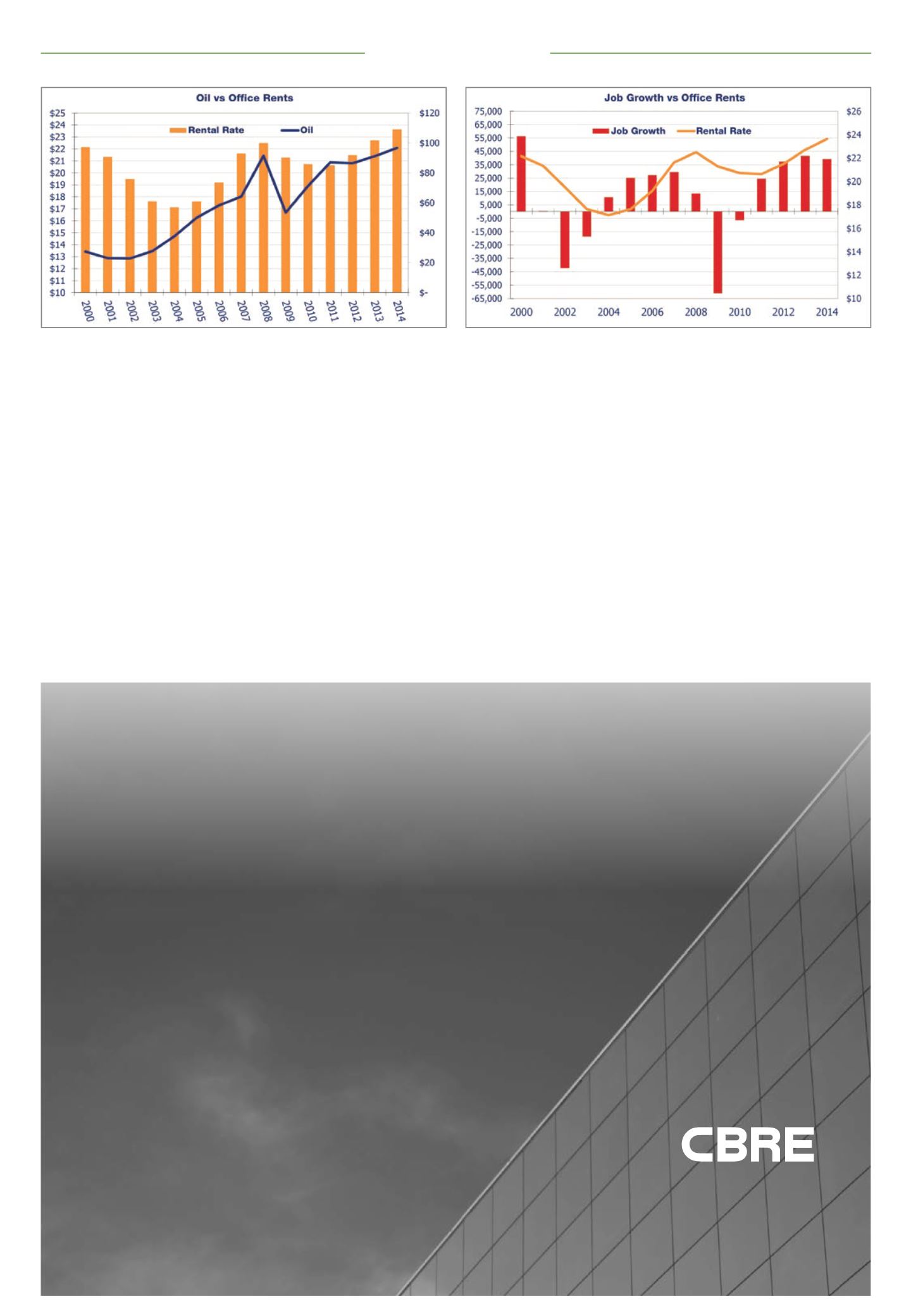

Job growth and office rental rates in metro Denver.

Courtesy Cresa

Oil prices and office rental rates in metro Denver.

cbre.com/denver cbre.com/fortcollins cbre.com/coloradospringsUNRIVALED

TALENT.

UNMATCHED

RESULTS.

With a passion for everything that makes our state so

special, our firm is the unrivaled leader in commercial

real estate services in Colorado. Strategic, forward-

thinking and results-driven, our 500 professionals are

committed to delivering the best to our clients and the

community we serve.

For more information on how CBRE can assist you with your

commercial real estate needs in Colorado, please contact:

Pete Schippits

Senior Managing Director

+ 1 720 528 6440

opportunities for other sectors, said

Harrington.

An interesting comparison to the

sublease space now available is the

850,000 sf of space that came on

line at 1801 California St., when the

Qwest and Century Link deal was

finalized in late 2012 and early 2013.

That much space was the equivalent

to one or two new office buildings

coming on line, but didn’t cause

nearly as much conversation, said

Johnson. And downtown Denver is

leasing up that space right now.

“I think this is a healthy enough

downtown that we’re going to be

able to absorb this excess space,”

said Charlie Lutz, Cresa senior advis-

er. “There’s a lot of positive things

trending in Denver right now.”

With that in mind, don’t expect

rental rates to change anytime soon.

Compared with the 1980s, building

owners have a different mental-

ity, said Johnson. In the 1980s, 13.5

million sf of new product came to

market, which contributed to the

dramatic spike in vacancy. Presently,

there is about 3 million sf under

construction. These new buildings

are under no pressure to reduce

rents unless difficulties in lease-up

are experienced after completion.

Of all the current office product

downtown, most of the buildings

are 90 percent leased or better, with

many of the leases extending seven

or eight years out. These owners

don’t need to panic, and they don’t

need to respond in a rate-slashing

way, Johnson said.

A white paper published by Cresa

examined the relationship between

rental rates and oil prices. The

results were inconclusive:

• 1985-1986: Oil prices dropped 45

percent and rent rates dropped 15

percent

• 1990-1993: Oil prices dropped 32

percent and rent rates increased 19

percent

• 1996-1997: Oil prices dropped 42

percent and rent rates increased 6

percent

• 2008: Oil prices dropped 42 per-

cent and rent rates dropped 11 per-

cent.

However, the same study found

a direct correlation between job

growth and rent. The University

of Colorado Leeds School of Busi-

ness is predicting the state will add

between 30,000 and 35,000 new

jobs. (It originally predicted the

state would add 45,000 jobs, but

readjusted after oil prices dropped.)

This correlation would predict

Denver office rates will continue

to increase. “It’s still positive job

growth,” Johnson said. “More jobs

means more companies need to

lease more space.”

In the 1980s, Denver saw 13.5

million sf of new supply delivered,

which is almost half the office

space in the CBD – the current total

is 25.8 million sf, according to NGKF

statistics. Up until 1985, demand

outpaced supply; after 1985, the

opposite was true. Following 1986,

there was no new construction until

2000, and from 2000 to the present,

a total of 4.1 million sf of new office

product has been completed. Den-

ver is witnessing a much healthier

balance of supply and demand this

time around.

s