12 / 28

12 / 28

Page 12

— Office Properties Quarterly — July 2015

Market Drivers

by Michelle Z. Askeland

About 97 percent of all Colorado oil

and gas firms are located in down-

town Denver, specifically Lower

Downtown and the central business

district, which makes it natural to

wonder how the decline in crude oil

prices is affecting the office market.

The Denver office market is much

stronger than it was during previ-

ous oil price drops, and the drop is

not predicted to have much, if any,

impact to the overall marketplace.

So far, just under 600,000 square

feet of space is available for sublease

since the price decline, said Tim Har-

rington, executive managing direc-

tor in the Denver Newmark Grubb

Knight Frank office. The overall CBD

market is comprised of about 25.8

million sf, so that space represents

less than 2 percent. This dip has not

affected rental rates. “I think that

there’s a very good chance that it

won’t affect rates,” he said. “I think

that some of these sublease spaces

will get backfilled, and it’s not going

to be as negative an impact as it

once was back in the 1980s.”

The main reason for this outlook

is the diversification of the market.

Today, the oil and gas industry rep-

resents 10,446 jobs in downtown

Denver, and 11 percent of all private-

sector jobs, according the Downtown

Denver Partnership’s Economic

Impact of Downtown Denver Oil

and Gas Industry study. Taking into

account indirect industry firms,

the sector takes up 5.1 million sf of

office space or 22.6 percent of the

total office space downtown.

Back in 1985, when prices dropped

and Denver office vacancy soared,

the industry alone accounted for

about 32 percent of the market,

which made the city vulnerable,

Harrington said. Denver experienced

some of the highest vacancies in

the world at that time, hovering

between 30 and 32 percent. As the

market struggled to recoup, full-ser-

vice office space in brand new, Class

A buildings ranged from $12 to $15

per sf. In the early 1980s, the same

product would be in the $20 range,

he said.

Today, government, financial insti-

tutions, communications, engineer-

ing, legal and accounting sectors

all account for at least 10 percent

of the market makeup. “We’re so

well diversified,” he said. “Denver is

extremely healthy.”

The current vacancy rates are

headed toward 10 percent, said

Bruce Johnson, Cresa managing

principal. By Cresa’s definition, a

healthy vacancy rate is between

10 and 15 percent, in which case

the market is at equilibrium and

it is neither a landlord nor tenant

market. The oil and gas industry

would need to give up an exorbitant

amount of space to swing the vacan-

cy rates past the 15 percent mark.

This available oil and gas sublease

space – which has been put up by

four or five companies – presents

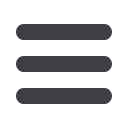

Denver enjoys the benefits of diverse marketCourtesy Newmark Grubb Knight Frank

Seven different industry sectors each account for at least 10 percent of the Denver market makeup.

Houston.

The Houston office mar-

ket, which is comprised of 286 mil-

lion square feet, currently has a

vacancy of 11.6 percent. After expe-

riencing banner years from 2012 to

third-quarter 2014, the city may be

at the tipping point of being a fun-

damentally stable environment to

something less stable in the office

sector, said Brandi McDonald, New-

mark Grubb Knight Frank executive

managing director in the Houston

office. “The true story will come out

in the Q3 and Q4 reports,” she said.

“Companies are not making deci-

sions right now if they don’t have

to,” she said. “It is our prediction

that our fundamentals will begin to

decline severely when Q2 and Q3

numbers come out. And I believe

they’re going to decline into the

first two quarters of 2016. Then we

predict an upturn by the end of 2016

and returning to a more healthy

environment in 2017.”

The city delivered 4.4 million sf

in the first quarter and there is 14.9

million sf still under construction,

said McDonald. The 70-plus pro-

posed buildings will not have a shot

at breaking ground on a speculative

basis until the city records at least

four consecutive quarters of sub-

stantial absorption, she said.

In the 1980s, 85 million sf of office

was delivered, but in the last 30

years, since the 1985 crash, Houston

only built 102 million sf of office.

“We have 11 corporate campuses

under construction now, nine of

which are energy companies,” she

said. “Those 11 corporate campuses

make up over 12 million sf coming

on line,” she said.

In the 1980s, oil and gas made up

80 percent of the office-user sec-

tor in Houston. Today, the industry

makes up 50 percent. “I believe that

we’re not going to see anything

compared to the ’80s because our

demographics have shifted and

we have mature developers who

remember lessons learned,” she

said.

Alberta, Canada.

The Alberta office

market consists of roughly 97 mil-

lion sf, and most of the office spaces

are in Calgary and Edmonton. Cal-

gary has roughly 63 million sf of

office, with 41 million sf located

downtown and the rest in suburban

areas, said Agron Miloti, president

and broker of the Calgary Newmark

Grubb Knight Frank office.

New Class A product tends to have

the city’s lowest vacancy rates. Since

the drop in oil prices, Class A build-

ings are reporting 9 percent vacancy

and Class AA buildings are at 7 per-

cent. “The real vacancies we’re see-

ing are in B and C Class buildings,”

he said. “Our C Class buildings are

about 17 percent vacant, so overall

vacancy downtown Calgary is right

now roughly 11 percent.” Miloti says

a healthy market is somewhere

between 7 and 10 percent vacancy.

In Calgary, oil and gas compa-

nies and related service companies

account for roughly 75 percent

of leased space. “So we really do

depend on oil prices being up there,”

he said.

“The strange thing, and the posi-

tive thing for Calgary, is that the

rates have not dropped that much,”

he said. “They’ve dropped roughly

between 8 and 10 percent. So the

landlords are still holding onto the

rates. If prices stay the same, it will

be difficult for them to do that.”

Calgary has about 4 million sf

under construction and about 90

percent of that space is spoken for.

Edmonton’s downtown is much

smaller than Calgary’s, even though

both cities have a population of

about 1.1 million. About 16.7 million

sf is located downtown and 10 mil-

lion sf is located in suburban areas,

totaling roughly 26.7 million sf of

office property.

Edmonton’s economy is more

diverse than Calgary’s economy.

There is a stronger government

presence, which takes up roughly

25 percent of the office space. An

additional 20 percent is used by

other professional sectors. The rest

is made up of oil and gas services

companies, he said.

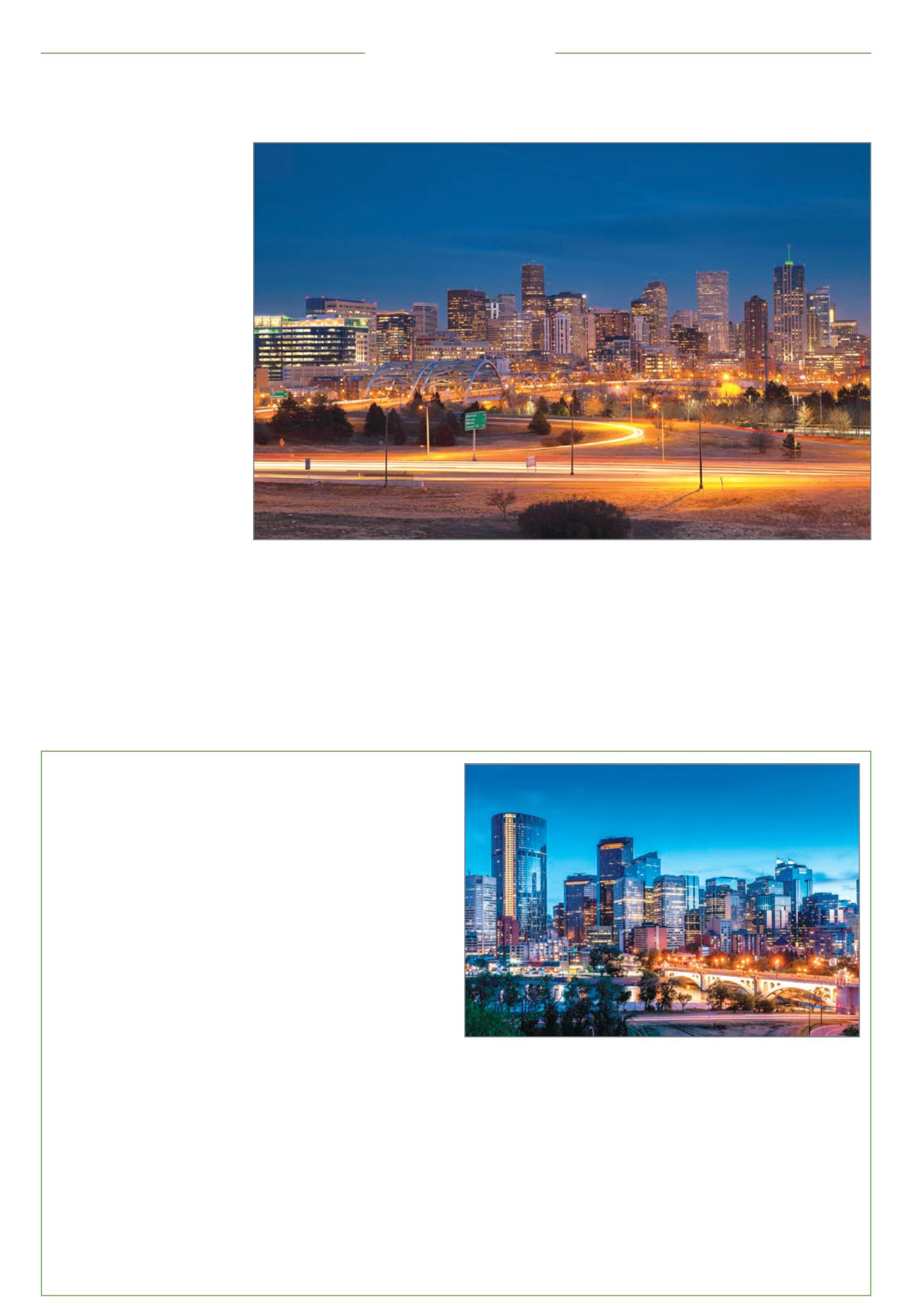

How does Denver compare to other hubs?Courtesy Newmark Grubb Knight Frank

Oil and gas companies and related services account for 75 percent of leased Calgary

office space.