4 / 28

4 / 28

Page 4

— Office Properties Quarterly — July 2015

Minimum Bid $50 psf -----

Previous units were sold between $165-$210 psf

LOCATION

Located within 4 miles of the new St Anthony’s

Medical Campus and few blocks from US-285

with easy access to C-470 and great visibility

from Kipling Street with near traffic count of

100,000 VPD.

More Info Available at: www.PrestigeAuction.com/CREJ0011-877-612-8494

3 UNITS AVAILABLE

Unit 108 - 1,600 sq ft

Unit 207- 3,222 sq ft

Unit B (208-209) - 4,450 sq ft

HIGHLIGHTS

Great access and visibility from Kipling

Adjacent to new and busy retail center

Near Federal Center, 285/Hampden, C-470

Busy intersection with strong traffic counts

Newer construction with modern architecture

Private entrances with dramatic window lines

This is your chance to capture a fantastic deal for your next business

location or to lease out and increase your portfolio.

All three units will be sold on this date to the HIGHEST BIDDER.

Property will

ABSOLUTELY

SELL

once minimum bid is met.

AUCTION

July 31, 2015 1pm

2535 S Lewis Parkway, Lakewood, CO 80227

OFFICE CONDO

PREVIEW

DATES:

Saturday, July 17th

Saturday, July 24th

11:00am - 2:00pm

3%

Broker

CO-OP

Investment Trends

D

enver’s office investment

sales market saw robust

activity during the first five

months of 2015 with capital

coming from national insti-

tutional buyers and private capital

investors in Denver and elsewhere

around the country. This activ-

ity continues from 2014, creating

an imbalance of supply-demand

and resulting in multiple, compet-

ing offers in this arena. For many

institutional investors, acquisition

parameters put Denver in the fore-

front of searches due to the region’s

thriving economy and attractive cli-

mate. Local owners, users and inves-

tors are betting on Denver as well,

making it an incredibly tight market.

A number of significant office

sales took place during the first and

second quarter. This includes a new

record sale of the Village Center Sta-

tion in Greenwood Village that sold

to KBS REIT for $326.50 per square

foot, the highest price per sf in the

southeast market. The property is

a mixed-use office and retail space

with an attached parking structure.

The price may seem high to some

onlookers but, with rising construc-

tion prices and downtown’s highest

sale price north of $600 per sf for

the office buildings flanking Union

Station, this may be considered a

deal.

Cap rates for office investments

averaged around 7.1 percent in 2014

and, so far in 2015, remain at 7.1

percent, according to Real Capital

Analytics. Value-add buyers are

prevalent in the marketplace; how-

ever, the demand

for assets with

higher vacancy

rates and proper-

ties in need of

significant renova-

tions has peaked.

Some properties

are being marketed

with pro forma

higher cap rates,

trying to capitalize

on the low office

investment inven-

tory and promising

potential buyers that leasing will

improve.

A recent transaction in the south-

east suburban market was the sale

of Park Meadows Corporate Campus,

a vacant building just south of Park

Meadows Mall. The property was

vacant since its 2009 construction.

A local private investor recently

purchased the property for $118 per

sf, recognizing the low cost of the

property compared with its replace-

ment cost. The new owner will lease

the property to medical and general

office tenants.

Downtown, 1515 Wynkoop recent-

ly traded for $560 per sf. This office

and retail building, which houses

restaurant Fogo de Chao and office

tenants include Chipotle, Policy

Studies Inc., and Green, Manning

and Bunch, is approximately 370,000

sf and was 97.5 percent leased at the

time of sale. The building received

multiple offers, and exemplifies true

institutional demand for core assets,

not only in Denver, but also in the

Western United States, said Geoff

Baukol of CBRE, who represented

the seller.

It is well known that Denver

is growing, with the population

increasing 1.74 percent in 2014. This

growth is attracting many compa-

nies that want to hire the talented

workers who move to Denver for the

lifestyle. Many companies prefer to

own rather than lease, yet it is a dif-

ficult task to buy when there is this

much competition. There are still

owner-user deals in the market, and

though some properties are highly

competitive, others are available and

remain good investments.

The office investment sales trends

should continue through 2015 if

interest rates remain favorable.

Concerns affecting investment sales

include multiple construction proj-

ects coming on to the market and

excess space returning to the mar-

ket for sublease from the oil and gas

industry.

s

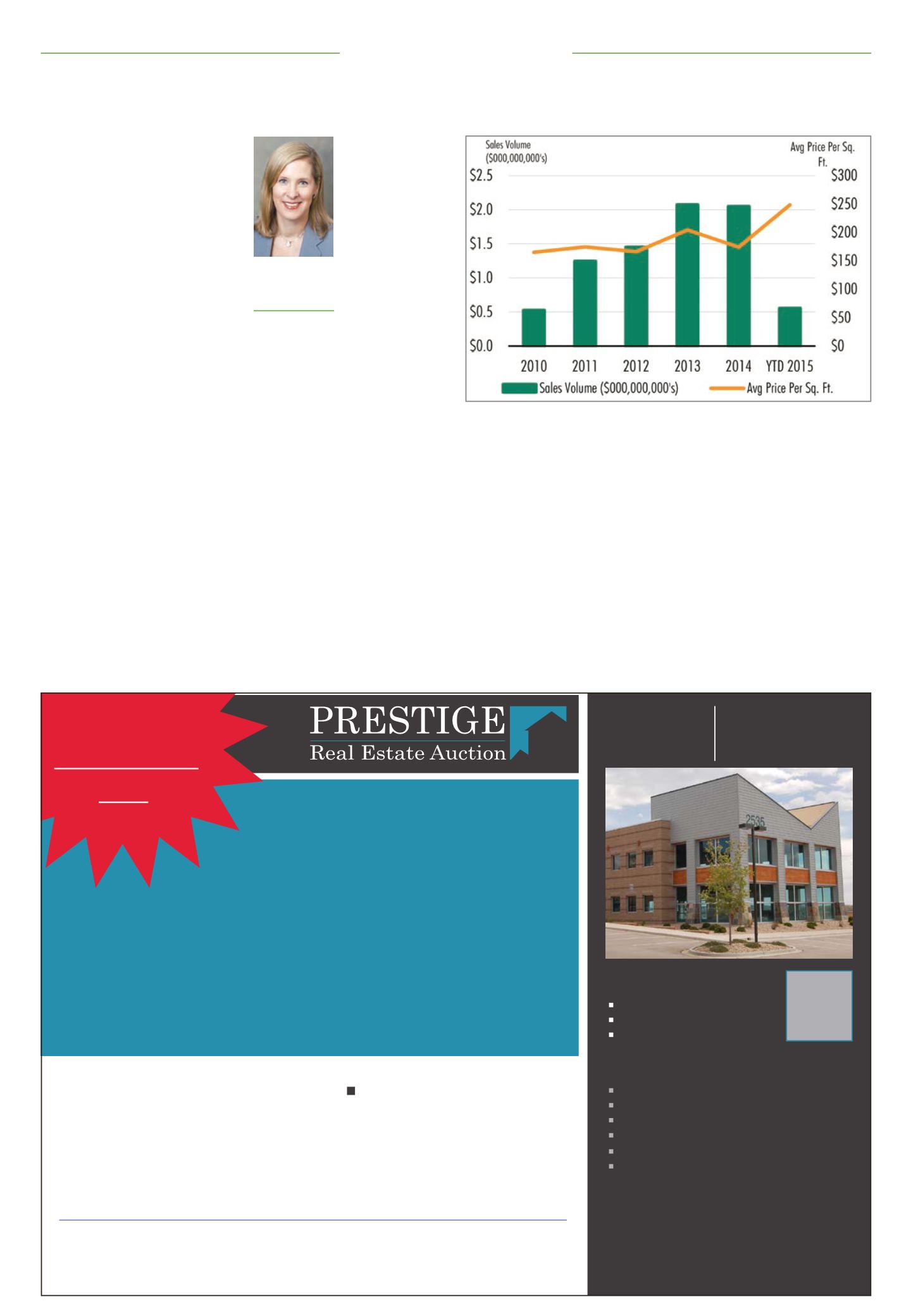

Mile High City investment sales trending highMonica Wiley,

LEED AP

Associate,

CBRE, Denver

CBRE Research, Q1 2015

The graph illustrates sales volume in the past five years along with average price per

square foot on the right column and indicated by the orange line. The pace is steady for

continued sales volume similar to the past two years but average price per sf is increas-

ing due to demand.