9 / 32

9 / 32

January 2015 — Office Properties Quarterly —

Page 9

F

or the past 20 consecutive

quarters, Denver has seen an

unprecedented rise in rental

rates in downtown and subur-

ban office markets. Currently,

rents downtown are at record highs,

with no clear relief in sight. For ref-

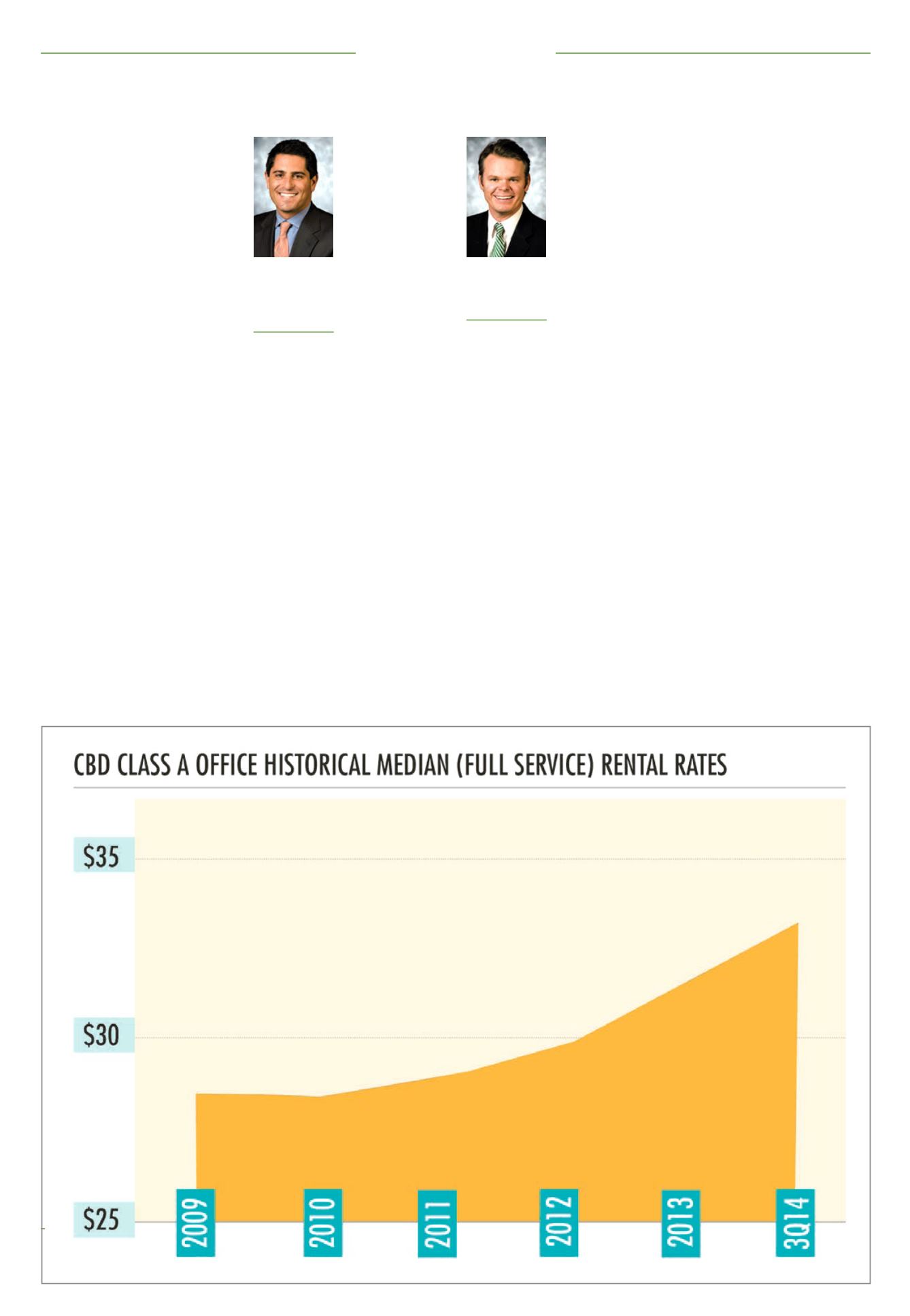

erence, the median asking rate for

a central business district Class A

space today is $33 per square foot,

which represents an 18 percent

increase from the previous cycle’s low

in 2009, when CBD vacancy hit 19

percent. Since then the CBD submar-

ket has absorbed 2 million sf.

Hear me now, and believe me later:

There is still value to be had in this

historically hot office market. But

first, some color.

The market has seen major upticks

in the past, specifically between

2003 and 2007, when investment

sales activity was at a then all-time

high. During this period, when com-

pared with today’s landscape, we

didn’t see the level of demand and

absorption, the changing dynamic of

tenants in the market or the overall

popularity of downtown Denver as a

new home for companies (e.g., Ardent

Mills, DaVita, Transamerica, On Deck

Capital). Furthermore, historically low

interest rates have given investors

the confidence to “stretch” to acquire

assets, driving values higher.

Since the previous cycle’s trough

in 2009, many factors have led to

Denver’s slow and steady climb to

prominence. Activity in the energy

sector improved with new oil and

gas discoveries in the Bakken and

Niobrara shale plays. Venture capital

firms looked to place their money in

startup companies, taking advantage

of new developments in technol-

ogy. Many of these

employers who

incubated in Boul-

der have moved to

downtown Denver

for a deeper tal-

ent pool (e.g., Send

Grid, Rally Soft-

ware). Amenities

in the form of new

restaurants, hotels

and transportation

gave businesses

more to offer their

employees. B-cycle

and ride-sharing

programs have made it easier to

navigate the growing downtown area.

And last, but certainly not least, the

renovation of the historic Union Sta-

tion put Denver on the global map

as a major player in the competition

for large corporate offices (e.g., IMA

Financial, Antero Resources, First

Western Trust, Hogan Lovells).

Similar to previous growth cycles,

investors are finding great opportu-

nity in the form of rent growth, and

have begun to pick off the low-hang-

ing fruit, sometimes even reaching

for the tops of the trees, as evidenced

by the sales of the two Union Sta-

tion wing buildings for $600 per sf.

There is now more than 1.4 million sf

of speculative office product under

construction downtown or will be by

the middle of 2015. All of these new

projects are commanding lease rates

in the $45 per sf full-service neigh-

borhood, which allows the existing

buildings to “draft” off these prices

and raise their own rates.

All of the above improvements

spelled trouble for those tenants

who basked in the glory of their rela-

tively inexpensive

overhead for the

previous five years

or so. In addition

to the competitive

hiring landscape

facing most com-

panies, they are

now confronted

with an even more

daunting challenge:

how to find a spot

that won’t inflate

the second-largest

expense item in

the budget. We suggest the following

eight considerations:

1. Rethink the way you approached

office space in the past.

Traditional

industries, such as legal, financial

services, oil and gas and even…ahem…

commercial real estate houses, are

finding new and creative ways to

maximize efficiency, while keeping

employees happy and engaged. Con-

sider the value of a more open layout

with less enclosed offices, more open

and collaborative workspaces, and

even hoteling options for those who

spend less than 50 percent of their

time in the office.

2. Keep an eye out for landlords who

bought low,

thus giving them the

opportunity to “reach” for tenants

that are currently occupying space in

buildings that have recently sold at

those higher value numbers.

3. If you’re a technology firm or other

Lower Downtown type,

consider this

– buildings in the central core and

Uptown, which often are less expen-

sive than LoDo, can create an envi-

ronment that fosters creativity by

tearing out ceiling grids and tiles, and

installing new and clean spiral duct-

work similarly found in the renovated

warehouses. One traditional office

building is taking a unique approach

by adding a patio with pingpong

tables and corn hole sets; another is

adding a rooftop deck.

4. Believe it or not, the investment sales

market could work in a tenant’s favor

by

finding landlords who need to lock

down that one last tenant before they

put the building up for sale.

5. On that note, seek out landlords who

have significant tenant turnover

on the

horizon and could use more stability.

6. If you don’t absolutely need to be

downtown,

look to the periphery in

areas such as the Golden Triangle,

River North, Highlands, Santa Fe Arts

District or other areas that offer more

relief in the way of base rents, operat-

ing expenses and parking.

7. If you’re a startup, keep in mind that

landlords aren’t thrilled

about the pros-

pect of dumping loads of money into

building out space, so keep it simple,

unless your investor is ready to come

up with some form of a guarantee.

Find space that can be re-used or

re-purposed and still suit your needs.

Get creative with flexible furniture

that you can take with you along the

way.

8. Most importantly, get into the market

early

and don’t get caught scrambling

at the last minute. It’s a fast-moving

environment with surprises around

every corner.

In short, there are still compelling

reasons for landlords to compete for

tenants. Open your mind, protect your

bottom line and leverage the expertise

of those who do this on a daily basis.

s

Navigating Denver’s central business districtLeasing Market

Matt Davidson

Managing director,

Newmark Grubb

Knight Frank,

Denver

Andrew

Blaustein

Managing director,

Newmark Grubb

Knight Frank,

Denver

Central business district Class A office historical median (full-service) rental rates