6 / 32

6 / 32

Page 6

— Office Properties Quarterly — January 2015

T

he Front Range office mar-

ket consists of 222.5 million

square feet from Trinidad to

Fort Collins/Greeley with a

respectable overall vacancy

rate of 9.9 percent. Overall Front

Range vacancy rates have ticked

down 120 basis points from a 10.7

percent vacancy

rate at the start of

2014. Consider, too,

the Front Range

has 251 million sf

of retail (with a 5.5

percent vacancy

rate) and 340 mil-

lion sf of industrial

(with a vacancy rate

of 4.7 percent).

The overall 813

million sf of com-

mercial real estate

on the Front Range

is healthy in all sectors with office

product making up 27.4 percent of

the overall commercial product. Con-

struction cranes are the visible sign

the market is healthy and ready for

new product.

Denver’s central business district

market overview includes Lower

Downtown and the Platte Valley. The

overall CBD consists of 34.8 million

sf with a vacancy rate of 10 percent

and average full-service rates of

$31.87 per sf. Vacancy rates have

declined 120 bps from 11.2 percent

at the start of 2014, and lease rates

have increased $1.17 per sf during the

same time period.

The LoDo submarket is the stron-

gest submarket in the state. At 8.6

million sf, the current vacancy rate

is 6 percent. Average lease rates are

$34.58 per sf. Currently four build-

ings are under construction in LoDo:

• 1601 Wewatta, 10 stories –

299,544 rentable sf

• 1401 Lawrence St., 21 stories –

311,015 rentable sf

• The Triangle Building, 1550

Wewatta, 10 stories – 242,807 rent-

able sf

• The Lab, 2420 17th St., four stories

– 78,576 rentable sf

The 2015 CBD outlook is positive.

All roads, rail lines, pedestrian and

bike paths lead to Union Station.

The opening of the train line from

Union Station to Denver International

Airport will be a significant game-

changer for the area. The announce-

ment of Whole Foods at 17th and

Wewatta streets coupled with the

construction of King Soopers at 20th

Street and Chestnut Place further

enhances, stabilizes and affirms the

bullish outlook for downtown Denver.

Other proposed office develop-

ments include:

• Z Block, 1800 Wazee – 235,002

rentable sf

• A Block, 1881 16th St., five stories

– 58,000 rentable sf

• Union Tower West, 1801 Wewatta

St., 12 stories – 100,000 rentable sf

• Chestnut Building, 16 Chestnut

Place, 18 stories – 547,199 rentable sf

• 1144 15th St., 38 stories – 640,429

rentable sf

Oil and gas companies are a sig-

nificant driver of the downtown office

market. With the recent decrease in

the price of oil, it’s conceivable these

proposed developments will remain

just that through 2015.

The southeast suburban office

market runs along Interstate 25 from

Interstate 225 to Lincoln Avenue

and includes the Denver Tech Cen-

ter, Greenwood Plaza, Panorama,

Inverness and Meridian. The market

consists of 45.7 million sf and has a

vacancy rate of 11.8 percent. The SES

market is diverse (telecom, health

care, defense industry, engineering

and financial industries) and active

from small to large tenants. There are

a significant number of large tenants

(i.e., 70,000 sf or larger) currently in

the market that are competing for,

and will ultimately lease, the large

blocks of available space. New con-

struction includes CoBank Center, an

11-story, 276,000-rentable-sf build-

ing scheduled for completion in the

fourth quarter. The SES submarket is

ripe for speculative development, and

potential new office developments

include:

• Village Center DTC, 10 stories –

300,000 rentable sf

• One Belleview Station, 16 stories –

340,000 rentable sf

• Village Center Station II, 9 stories

– 200,174 rentable sf

• The Madden – Palazzo Verdi II, 14

stories – 428,749 rentable sf

Northern Colorado, which con-

sists of Fort Collins and Greeley, has

10.7 million sf of office space with a

vacancy rate of 5.1 percent, down 70

bps from the 5.8 percent vacancy rate

at the start of 2014.

The Northern Colorado economy is

strong and robust with Weld County

adding more than 9,000 nonfarm

jobs in the past two years and Lar-

imer County adding 11,000 jobs

during the same time period. Weld

County experienced a good part of its

growth in the food processing and oil

and gas sectors while Larimer Coun-

ty’s growth is oriented toward health

care, education, professional, sci-

entific and technical industries. The

strong economy will bode well for the

Northern Colorado office market.

Southern Colorado, including Pueb-

lo and Colorado Springs, has 30.9

million sf of office with a vacancy

rate of 11.3 percent. While Pueblo’s

office vacancy has decreased 210

bps from the start of 2014, Colorado

Springs’ vacancy has increased 30

bps. Health care and transporta-

tion are primary growth industries

in Pueblo with health care, finance

and insurance, and technical services

driving the Colorado Springs econo-

my. The 2015 office forecast is mod-

est but there is continued demand for

office space.

The Western Slope has 2.8 million

sf of office space from Durango to

Craig boasting a modest vacancy rate

of 5.3 percent. However, the vacancy

rate has increased 140 bps, from a

3.9 percent vacancy rate at the start

of 2014. Considering the Western

Slope has 22.5 million sf of retail

space (with a 4 percent vacancy rate)

and 4.7 million sf of industrial (with a

6.6 percent vacancy rate), the overall

32 million sf of Western Slope com-

mercial real estate is healthy. Western

Slope office product represents less

than 9 percent of the overall com-

mercial market. With no new mult-

itenant office construction planned,

the coming year’s outlook is positive.

The University of Colorado’s Leeds

School of Business released its report

on the 2015 Colorado business

economy outlook, which predicted

a population “increase of 85,000, or

1.6 percent, for 2014; 89,000, or 1.7

percent, for 2015; and 93,000, or

1.7 percent, for 2016.” By 2015, the

report forecasts Colorado’s population

to reach 5.4 million. The unemploy-

ment rate, currently 5.8 percent, is

predicted to continue to decrease

through the year. With expanding

companies, new jobs and an increase

in population, the 2015 forecast for

the Colorado commercial office sector

looks strong.

s

All signs point up for Colorado’s office marketsLeasing Market

William B. Lucas

Senior vice

president,

principal, Cassidy

Turley, Denver

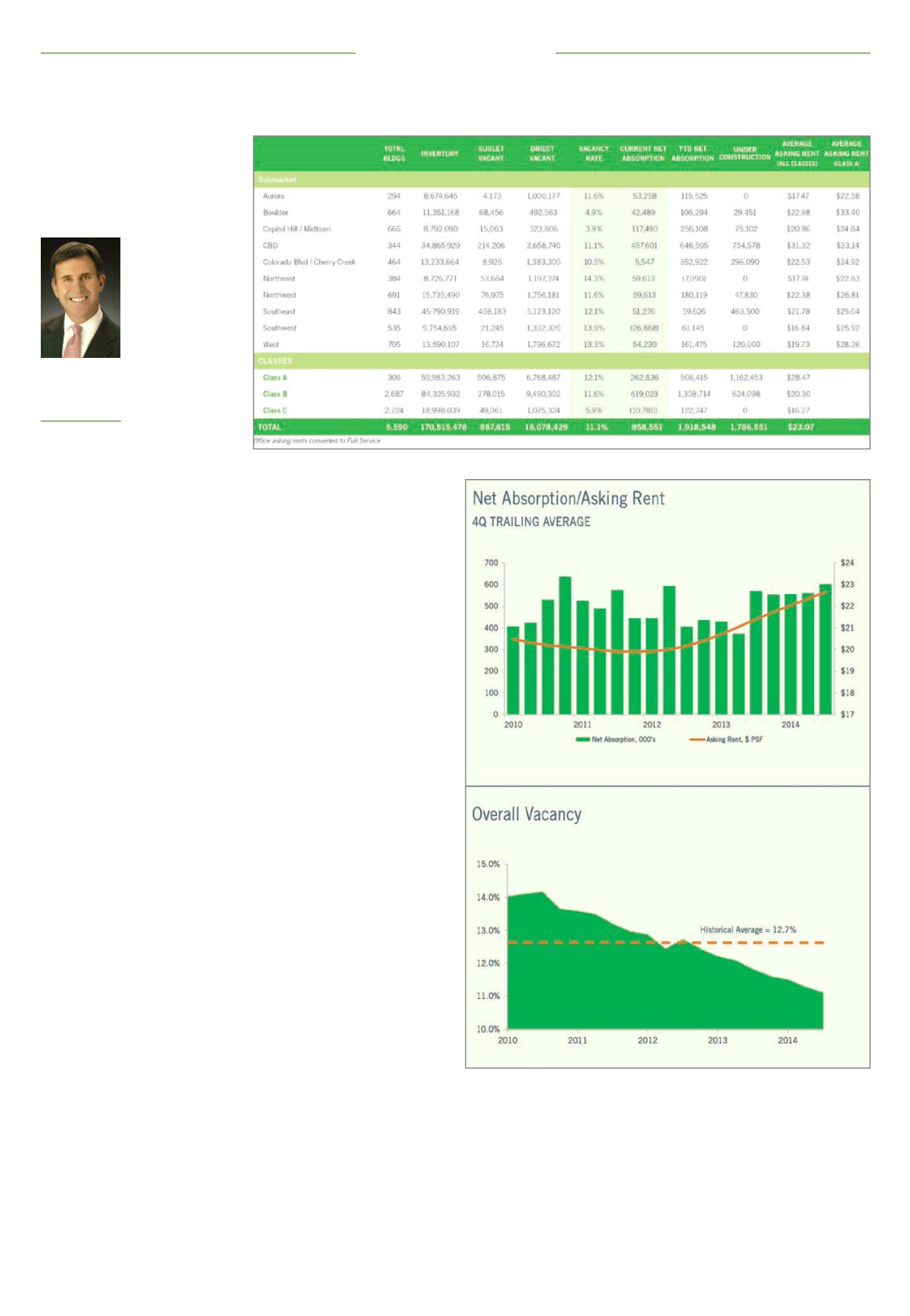

A snapshot look at third-quarter 2014 office properties, by submarket and office class

Denver office market's net absorptions, asking rents and vacancies