18 / 36

18 / 36

Page 18

— Multifamily Properties Quarterly — November 2017

www.crej.comProfessional Management, Better Results

Full Service

Property Management

Providing award winning property management services

for over 30 years along Colorado’s Front Range

GBRents.com GriffisBlessing.com303.771.0800

5600 S. Quebec St, B141

Greenwood Village, CO 80111

719.520.1234

102 N Cascade Ave, Ste 550

Colorado Springs, CO 80903

• New Build

• Lease-Up

• Repositioning

• Rehabilitation

• Due Diligence

Valuation

A

persistent gripe in developer

circles is the constant upward

movement of construction

costs. This has been a sub-

stantial brake on the fast-

moving train of new construction

within the Denver market. Steadily

rising payroll and materials costs have

prevented new deals from penciling,

which has resulted in tightened purse

strings of construction lenders. More

and more proposed projects are being

left without financing, forcing devel-

opers to drop sites they have under

contract for acquisition. Don’t cry for

the down-trodden developer, though,

because there is more to this story

ahead.

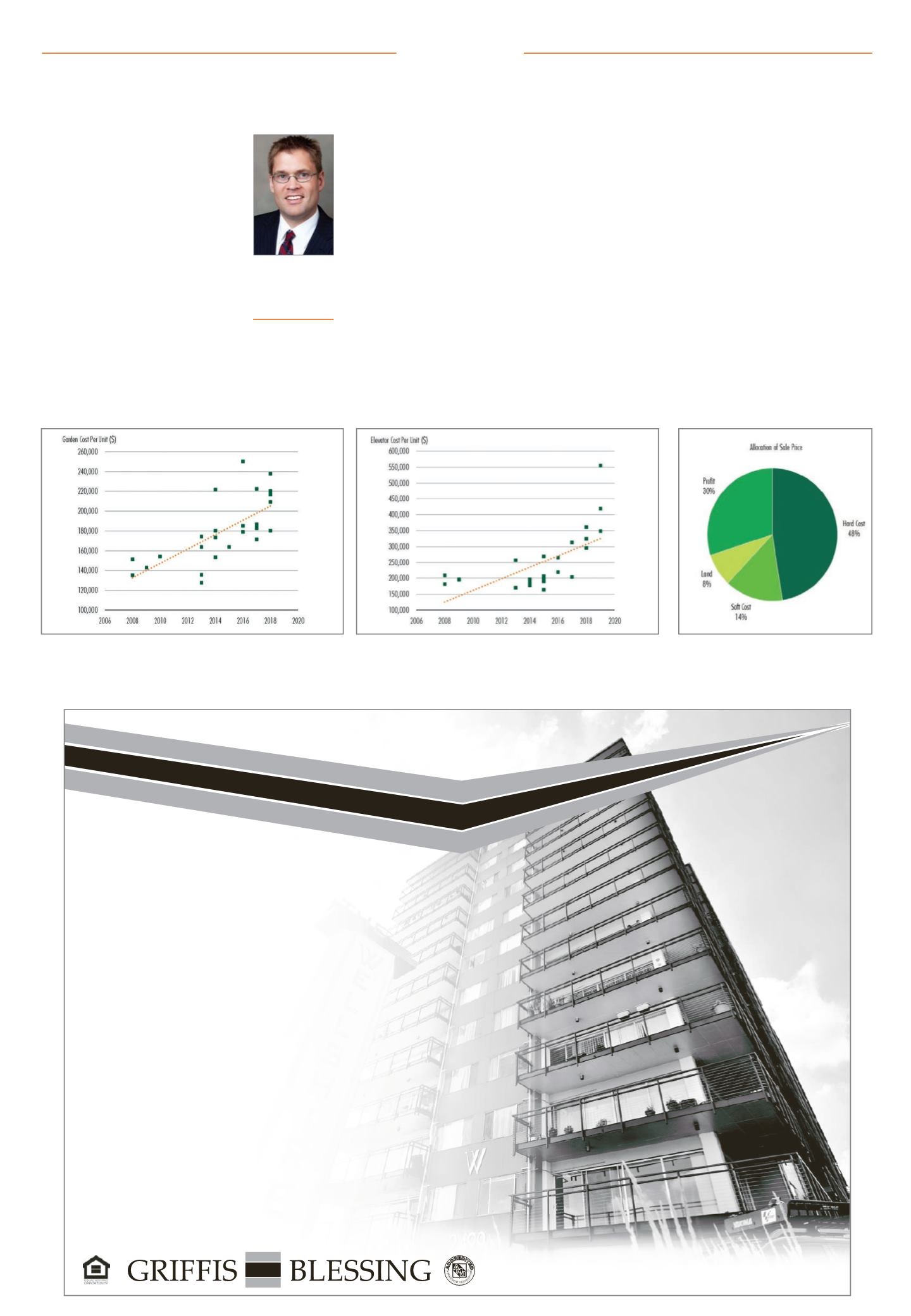

These rising costs have made cash-

ing out of projects a lucrative pros-

pect for builders who brought their

projects to market. As costs have

risen over the past eight years in the

post-2009 doldrums,

we have seen the

per-unit cost metric

change dramati-

cally. The two tables

reflect “all-in” costs

of projects brought

to market over the

past 10 years. This

all-in cost is inclu-

sive of hard and

soft costs, as well

as land acquisition

costs. This cost does

not include a profit

incentive. The data

reflects the trends on over 50 com-

pleted or underway projects in the

Denver metropolitan statistical area.

The dramatic shift shown in the

charts has moved the typical all-in

garden apartment construction costs

from a level of $135,000 to $150,000

per unit at the start of the cycle to

current projects in the $210,000 to

$240,000 per unit range. More dra-

matically, we have seen elevator-style

projects shift in cost from $180,000 to

$210,000 per unit to current projects

under way at costs north of $500,000

per unit. This leap in construction

costs has changed the value per unit

landscape of the market today.

As appraisers, we are armed with

the principle of substitution; we state

that a prudent buyer would pay no

more than construction cost new

today plus a profit incentive. However,

the concept of “cost new today” is

a moving target, steadily advancing

with the market. Next, we ponder the

more elusive topic of how much prof-

it? The answer to this question is hard

to extract. In our discussions with

market participants, we often hear a

range of 15 to 25 percent. But this will

only be borne out in an active market-

ing process, with buyers pitted against

one another to provide the highest

price to the seller.

This leads to a second area of

research: What profit have developers

actually been achieving? As costs have

inflated on the order of 10 percent

per year over the last several years,

we have costs today that are 20 to 30

percent higher than the costs actually

locked in by the developer at the proj-

ect’s origination. Adding this market

movement to “cost new today” sweet-

ens the pot for our developer friend

mentioned earlier.

CBRE researched closed transactions

of new properties in the last several

years where construction costs were

known. This data leads us into the

pie-chart

graphic.Weaggregated the

Construction costs not diminishing profits, for nowMark Lodmill

Director, National

Multifamily

Valuation Group,

CBRE, Denver

CBRE

All-in costs of projects brought to market over the past 10 years. This cost is inclusive of hard and soft costs, as well as land acquisition costs, but

does not include a profit incentive. This data reflects the trends on over 50 completed projects and projects underway in Denver.

Please see Lodmill, Page 34CBRE

The chart shows where the average sale price

on a newly developed asset goes.