16 / 36

16 / 36

Page 16

— Multifamily Properties Quarterly — November 2017

www.crej.comMultifamily property management that puts

your building on a more profitable track.

Like the railroad platform that spins train cars in a new direction,

Wheelhouse Apartments™ repositions your property for increased

cash flow and building value.

Property Management

Leasing & Maintenance

Accounting

Construction Management

Asset Management

Marketing & Branding

Strategic Planning

Wheelhouse Apartments

is central Denver’s premier apartment property

management company, helping apartment owners maximize income and

property values through expert property management, innovative marketing

and branding, cost-effective renovations and asset management.

UNIQUE

PROPERTIES

Unique Apartment Group

COLORADO’S PREMIER APARTMENT BROKERS

In partnership with:

Call us for a free initial

consultation: 303.518.7406

Part of the Wheelhouse family of companies: Boutique Apartments

•

Wheelhouse Apartments

•

Wheelhouse Commercial Management

•

Wheelhouse Construction

Wheelhouse Apartments • 574 Santa Fe Drive, #110 • Denver, Colorado 80204

• www.wheelhousemgmt.com•

www.wheelhouseapts.comDenver Highlight

T

wo years ago, the Denver

apartment market was one

of the nation’s strongest.

The market was fuller than

it had been in 15 years, and

rents were growing at a dizzying

pace. A lot of that momentum traced

back to phenomenal growth in the

metro’s young, talent-rich labor

force. Today, educated millennials

will move toward the metro for well-

paid employment opportunities and

a quality of life rivaled by few other

places in the country. While Denver

is still a hot spot for relocations, the

apartment market has cooled off

significantly.

If the market’s fundamentals

remain strong, then why isn’t the

Denver apartment market perform-

ing at the same level as in 2015?

Simply put, developers are bringing

new apartments to the market faster

than renters can fill them.

Developers delivered 5,835 new

apartment units to the metro dur-

ing the first three quarters of 2017,

according to our pipeline figures.

Some 4,990 more are identified for

completion in the fourth quarter,

bringing the year-end total to 10,825

new units – the most this cycle.

Some 9,720 units have been identi-

fied for delivery for all of 2018. That’s

a total of 20,545 new units in two

years.

At the same time, annual job

growth levels in Denver have

declined from 3.5 percent in Sep-

tember 2015 to 1.4 percent in Sep-

tember 2017. That’s an average pace

in the national picture, but a slow-

down is expected in a market where

unemployment is very low. Even

with the slow-

down, apartment

demand remains

high because of a

variety of factors,

including:

• Denver is a

growing tech hub

with a vibrant

arts culture that is

attracting highly

educated millenni-

als to the area.

• Population of

the prime renter

group (ages 20-34)

has increased by

13.3 percent from 2010-2015, accord-

ing to Census Bureau statistics. This

rise has been buoyed by the reloca-

tion of several companies, particu-

larly in the financial services sector,

from higher-cost California locations

to Denver.

• Single-family inventory is tight,

especially in the $100,000-$300,000

price range, which keeps more peo-

ple in apartments.

No matter how strong the apart-

ment demand is, it still is not

enough to keep up with supply,

which is why rent growth has

remained comparatively low com-

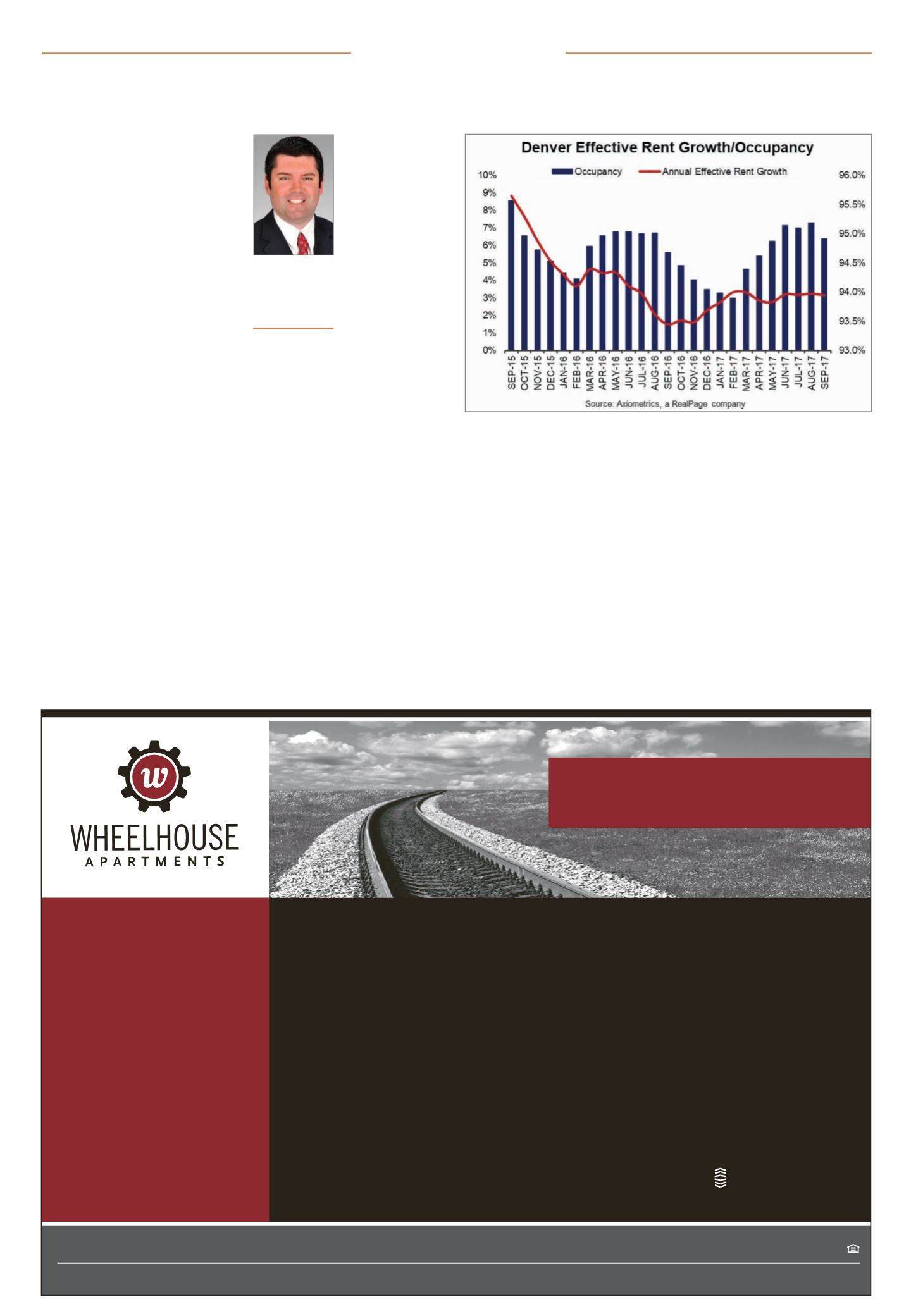

pared to earlier in this cycle. The

Denver average effective rent has

increased $91 since the beginning

of this year to $1,451 in September,

according to our data. Annual effec-

tive rent growth was 3.1 percent,

compared to the cycle low of 1.5

percent last September. Still, that’s

down more than 7 percentage points

since mid-2015.

A large percentage of these new

units are amenity-rich, Class A spac-

es that are marketed to higher-end

renters. And although luxury apart-

ment rent growth spiked in Septem-

ber, it remained the lowest of the

three primary classes in September.

Meanwhile, as rents are rising from

the cyclical low, concessions fell at

existing properties, but increased in

new properties, which are not includ-

ed in the rent-growth calculation.

Existing properties that cut an average

of 0.7 percent off asking rent for con-

cessions in January were only taking

off 0.3 percent in September, signifying

property owners’ confidence in filling

their properties.

Concessions offered in lease-up

properties, however, have increased

this year, from 5.1 percent off asking

rent in January to 5.9 percent off in

September. This increase shows how

owners of new properties are realizing

the competition they face for resi-

dents, especially when effective rent

growth for these newer properties was

-0.7 percent in September.

Digging down into Denver submar-

kets, the urban core, in this instance

the downtown submarket, is taking

the lion’s share of new supply. Some

3,141 new units have been identified

for delivery in the next two quarters,

34.8 percent of the metro total, on

top of the 2,128 units completed in

the first three quarters of 2017. Given

those supply figures, it’s no surprise

that downtown Denver has the low-

est annual effective rent growth in the

metro, -2.7 percent in September.

Denver remains a leader for market strengthJay Denton

Senior vice

president,

Axiometrics, a

RealPage Co.,

Richardson, Texas

Please see Denton, Page 34