10 / 28

10 / 28

Page 10

— Retail Properties Quarterly — May 2017

www.crej.comRetail Trends

R

etail is dead. Long live

retail!”While headlines

about the retail indus-

try are screaming, this

exclamation represents

a turn of phrase first used to com-

municate the continuity of royal

power. One king, declared dead, is

followed by the next in line bound to

rule and transform the country. And

few things have transformed more

aggressively in the last decade than

the retail industry and its indel-

ible connection to commercial real

estate.

Upon announcing the closure of

100 Macy’s stores last August, for-

mer CEO Terry Lundgren provided

some eye-opening statistics about

America’s retail conundrum: we

are vastly overstored. Per capita in

the U.S., developers have built 7.3

square feet of retail space (versus

1.7 sf in France and 1.3 sf in the

U.K.). And, since 1995, the number

of shopping centers in the U.S. has

grown by more than 23 percent

(and gross leasable area by almost

30 percent), while the population

has grown by less than 14 percent,

according to retail analyst Robin

Lewis.

We are seeing the results. For the

first quarter, Quantum Real Estate

Advisors Inc. reported declining

lease rates at malls (from $20.32 per

sf in 2016 to $19.85 per sf), while

rates increased in neighborhood

environments (up to $15.63 per sf).

While no single retail category

has been immune

to the all-powerful

growth of online

retailing, malls are

disproportionately

affected because

mainstays such as

apparel, footwear

and accessories

comprise the top

sellers online.

Independent retail

analyst Jan Rogers

Kniffen projects

that 50 percent of

all retail not tied to

bars and restaurants will go online

by 2030.

So far this year, we have already

seen nine major retail bankruptcies,

which is as many bankruptcies as

all of 2016 combined. Contributing

factors are numerous and include

increased consumer spending on

experiences, rather than buying

things. Travel and hotel occupancy

is up, and in 2016, for the first time

ever, Americans spent more money

in restaurants and bars than at gro-

cery stores.

•

Urban center investments.

Also

for the first time since the 1920s,

growth in U.S. cities is outpacing

growth outside of them. As millen-

nials and empty nesters increas-

ingly move into urban centers, more

retail investors are looking at street

retail, and those with a portfolio

of these assets are adding to them

with enthusiasm. Even smaller

markets such as Columbus, Ohio,

and Savannah, Georgia, are at the

magnified end of leading investors’

telescopes.

•

Street retail convenience and

magic.

For millennials and others,

street retail convenience frequently

wins out versus destination shop-

ping. Driving to, parking at and

navigating the mall environment is

not as appealing as a quick car ride

or – better – walking a few blocks

to meet daily needs. Some retailers

are leaving malls with urgency to

capture better neighborhood foot

traffic. A preferred local developer

for one of the nation’s largest cel-

lular providers said that he’s been

instructed to relocate 36 of 38 stores

from malls to street retail region-

ally.

At its best, street retail evolves as

community gathering points and

thoroughfares with daily-use retail-

ers like banks and coffee spots lay-

ered over with restaurants, bars and

grocers. A set of favorable specifica-

tions precedes development and

are highly valued in urban cores or

corridors:

•One-mile population range of

20,000 to 30,000 people, or 500,000

people within 5 miles;

•Annual income of more than

$50,000;

•Pedestrian friendly, broad side-

walks and detached lawns;

•Mature trees and landscaping or

the ability to add these elements;

and

•Proximity to public transporta-

tion.

A long view, swift calculations

and gut instinct combine to create

street retail magic. Transformations

are impactful and profitable when

the right tenants match consumer

demand. The ability to recognize

early site potential can be the key

to affordable transactions that bank

land for the future. Neighbors wel-

come progress on underutilized

parcels.

By contrast, there may be signifi-

cant costs associated with remnant

parcels in near-mature or mature

neighborhoods. This land generally

is smaller with a higher barrier to

entry and requires a creative blue-

print for structures and foot traf-

fic. Because retail follows rooftops,

residents are more engaged in the

development process. Still, even in

these more challenging scenarios, it

can be worth the investment to find

a home for retail tenants in these

communities.

Street retail in Denver has helped

enhance neighborhoods, including

North Denver (Lower Highlands,

Highlands, Sunnyside and Berk-

ley), River North, Baker, and the

East Colfax/17th Avenue and Colo-

rado Boulevard corridor. It’s not by

chance that the ultra-hip bakery

Voodoo Doughnuts opened its first-

ever location outside of Oregon

in Denver at Colfax and Hum-

Amid market challenges, street retail thrivesJay Landt

+1 303 283 4569

jay.landt@colliers.comLisa Vela

+1 303 283 4575

lisa.vela@colliers.comJason F. Kinsey

+1 303 283 4598

jason.kinsey@colliers.comBrady Kinsey

+1 720 833 4618

brady.kinsey@colliers.com4643 South Ulster Street

|

Suite 1000

|

Denver, CO 80237

+1 303 745 5800

|

+1 303 745 5888

fax

www.colliers.com/denverThis document has been prepared by Colliers International Denver for advertising purposes only. The

information contained herein has been obtained from sources we deem reliable. While we have no

reason to doubt its accuracy, no warranty or representation is made of the foregoing information.

Terms of sale or lease and availability are subject to change or withdrawal without notice.

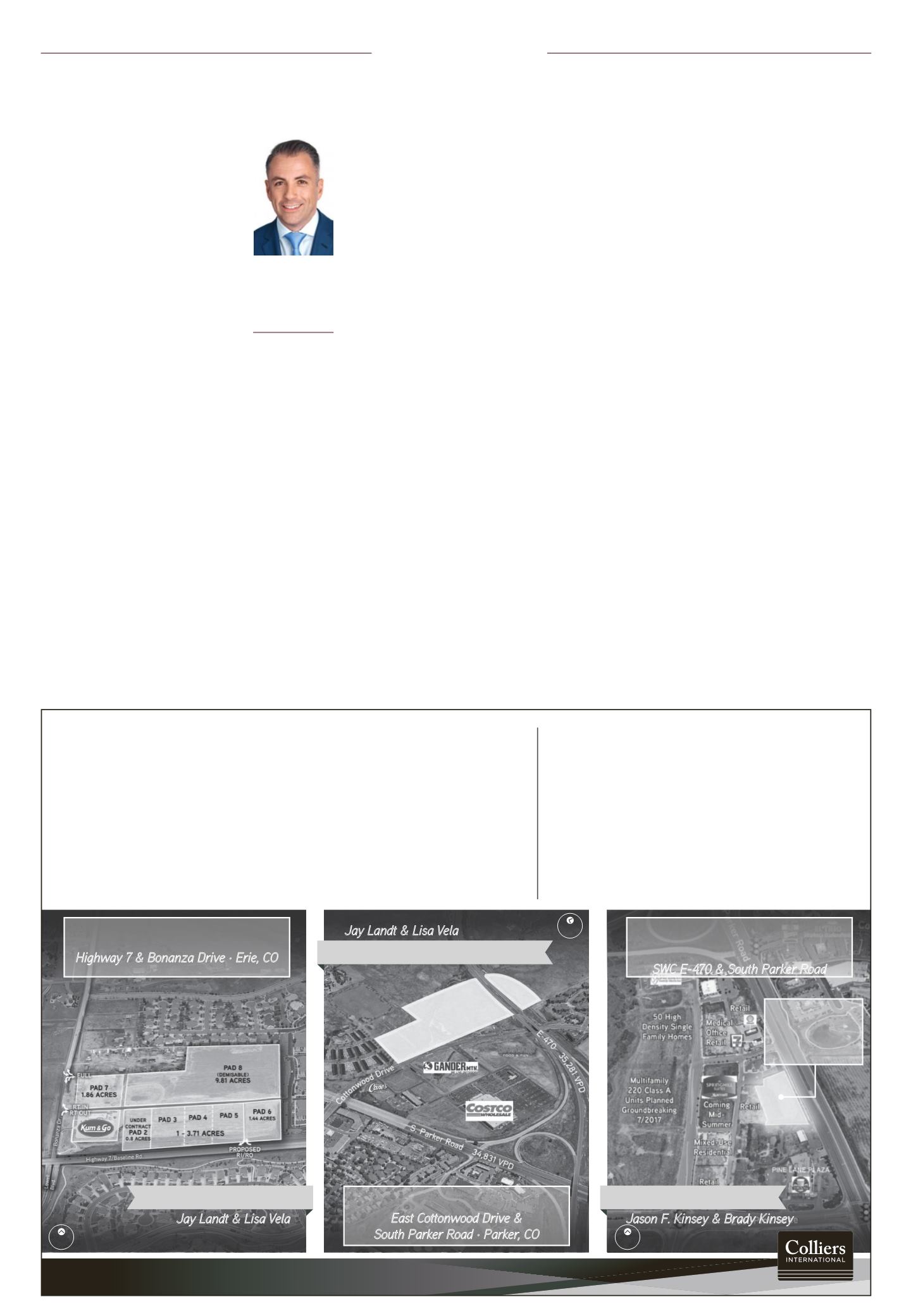

LAND FOR SALE

FOR LEASE

WESTCREEK

DEVELOPMENT

SWC E-470 & South Parker Road

VANTAGE POINT

East Cottonwood Drive &

South Parker Road · Parker, CO

VISTA RIDGE COMMONS

Highway 7 & Bonanza Drive · Erie, CO

c o l l i e r s i n t e r n a t i o n a l

Colliers International Denver Retail Team is pleased to present

these land offerings. Contact us for more information!

FOR SALE

FOR LEASE

FOR SALE OR GROUND LEASE

28.4 ACRES

1,200–

2,450 SF

AVAILABLE

ORTH

NORTH

ORTH

NORTH

ORTH

NORTH

ORTH

NORTH

NORTH

NORTH

NORTH

NORTH

NORTH

NORTH

NORTH

NORTH

NORTH

NORTH

NORTH

NORTH

NORTH

NORTH

NORTH

NORTH

&

Jason F. Kinsey & Brady Kinsey

Jay Landt & Lisa Vela

Jay Landt & Lisa Vela

Jimmy Balafas

Co-founder/

managing

principal, The

Kentro Group,

Denver

“

Please see 'Balafas,' Page 25