6 / 28

6 / 28

Page 6

— Retail Properties Quarterly — May 2017

www.crej.comMarket Update

I

s the internet killing retail as

an investment product type?

If you have been following the

recent store closure announce-

ments, one might be inclined

to believe that was the case. Macy’s,

J.C. Penney, Abercrombie & Fitch,

Gander Mountain, Sears/Kmart and

Whole Foods are among a number

of retailers closing stores across

the country. Others such as Sports

Authority, The Limited, HH Gregg

and American Apparel have filed

bankruptcy and either went out of

business completely or are moving

to an online presence only. However,

this frequently discussed narrative

overlooks the fact that while some

retailers have faced difficulties, due

to a constrained supply of new retail

construction, shopping center fun-

damentals are strong and improving.

The Denver metro area has seen

its fair share of store closures, yet in

total vacancies continue to decline.

Rents continue to increase. There

is no shortage of demand for well-

located, appropriately priced retail

shopping centers. In fact, investor

demand for retail centers far outpac-

es supply. These trends are seen on a

national level as well.

The internet clearly is having a

negative impact on certain types of

retailers, and it is forcing landlords

to revise their tenant line-ups to

favor food service, health and value-

oriented retailers, but its cumulative

impact has not changed the appeal

and viability of shopping centers as

an investment.

Since peaking in fourth-quarter

2009, the Denver metro area retail

vacancy rate has fallen every year

and is projected to

hit 4.8 percent in

2017. This is despite

the area absorbing

a number of clo-

sures during this

period from retail-

ers such as Safe-

way/Albertsons,

Sports Authority,

Office Depot/Office

Max and Golf

Smith, to name a

few.

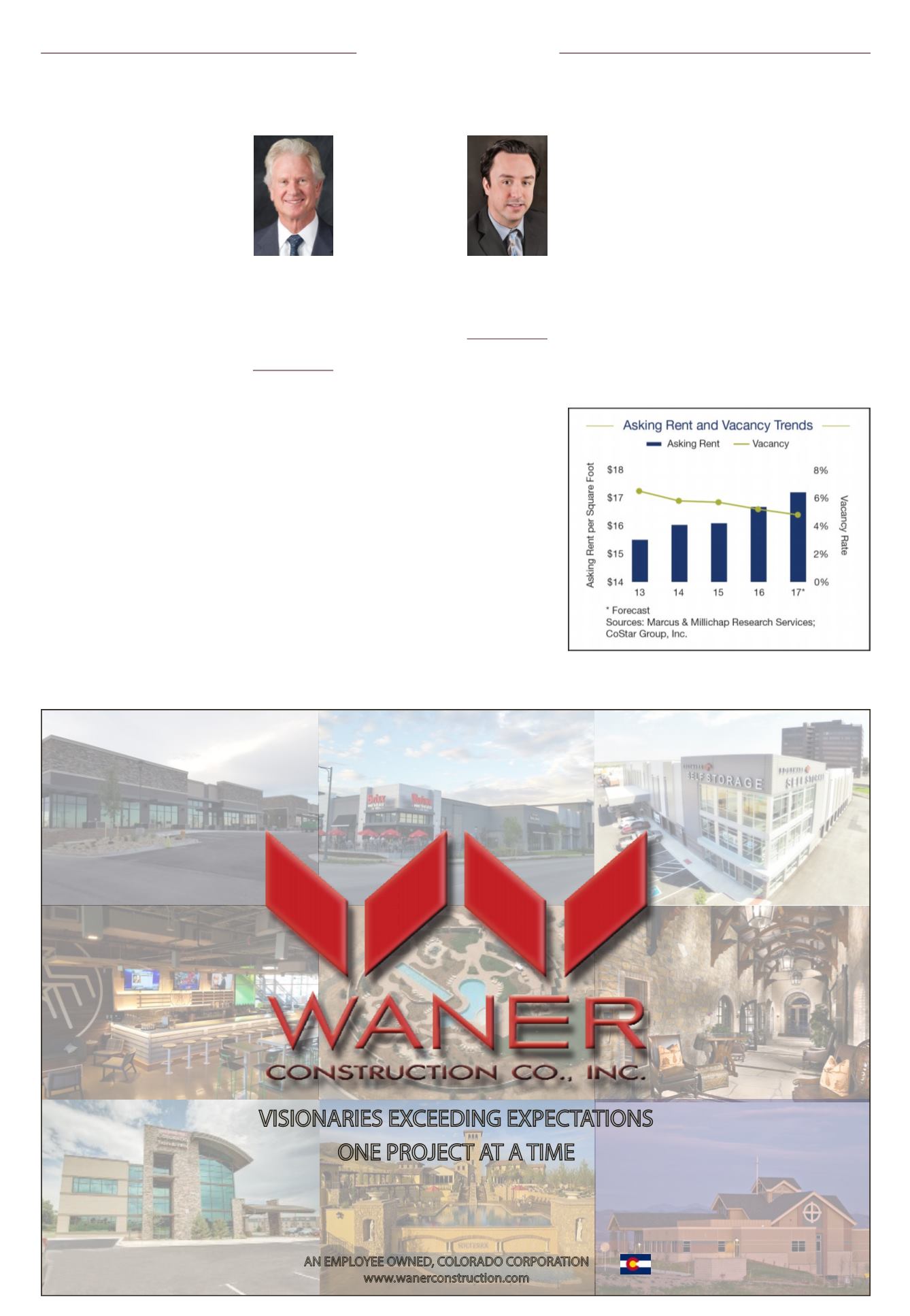

As the vacancy

rate has decreased,

rents have been

increasing. Retail

rents grew by 3.6

percent in 2016

and are projected to increase by 3.1

percent to $17.19 per square foot

in 2017. The driving factor at work

here is that while population and

consumer demand have increased,

the supply of new retail construction

has remained relatively constrained.

Since the recession, deliveries of new

retail construction have been less

than one-third of what they averaged

prior to the recession. This has put a

significant premium on viable retail

shopping centers for tenants and

investors.

Well-located shopping centers in

the Denver metro area continue to

be highly sought after and are trad-

ing at more aggressive values relative

to income than they were prior to

the recession. Assuming a property

is properly priced, numerous offers

can be generated in relatively short

periods of time. Newly constructed

small strip retail centers, often fea-

turing restaurants

and food-service-

related retailers,

are highly coveted

by 1031 exchange

buyers looking for

passive income.

Most likely we

have seen the

peak of this cycle

with respect to

capitalization rate

compression; how-

ever, this is largely

a product of the

changing interest

rate environment.

The 10-year Trea-

sury has increased 60 basis points

since the election (at the time of this

writing), and the federal funds rate

is projected to

see an additional

six increases

over the next 18

months. Assum-

ing the Fed con-

tinues increasing

interest rates,

there is a strong

possibility that

the 10-year Trea-

sury reaches 3

percent by the

end of 2017 for

the first time

since December

2013. As interest

rates rise, buy-

ers will require

higher capital-

ization rates to

achieve their

targeted returns.

It’s important to point out that

capitalization rates have decreased

every year, on a year-over-year basis,

since 2010 – the same period of time

that has seen exponential growth in

internet retail sales.

Strong and stable job creation in

the Denver metro area continues

in 2017 and is expected to create

another 41,500 jobs by the end of

the year. This is in spite of the fact

that the unemployment rate in Colo-

rado is at 2.9 percent, its lowest level

since 2001. Continued job creation,

combined with a low unemployment

rate, has led to several consecutive

years of wage growth. Incomes in

Denver have seen an increase of

nearly 25 percent since 2010, accord-

Retail fundamentals are solid, despite closuresVISIONARIES EXCEEDING EXPECTATIONS

ONE PROJECT AT A TIME

AN EMPLOYEE OWNED, COLORADO CORPORATION

www.wanerconstruction.comGarrette

Matlock

Senior vice

president of

investments and

senior director,

Marcus &

Millichap, National

Retail Group,

Denver

Ryan Bowlby

Senior broker

and associate

director, Marcus &

Millichap, National

Retail Group,

Denver

Please see 'Matlock,' Page 25Marcus & Millichap

Denver’s asking rent and vacancy trends from 2013 to 2017