7 / 24

7 / 24

February 2015 — Retail Properties Quarterly —

Page 7

I

t has been said that the econ-

omy of Colorado Springs his-

torically trails Denver by 12 to

18 months. When a downturn

hits the economy, Colorado

Springs may not feel the full impact

for up to a year after the Denver

market, and when the economy

begins to recover, Colorado Springs

does not see that recovery for 12

to 18 months. I have never heard

a definitive explanation for this

lag – maybe it is because Colo-

rado Springs’ economy is heavily

influenced by the military (30-plus

percent) and government spending

does not follow the national or state

economies, or maybe the compa-

nies that provide the primary jobs

have different influences than those

in Denver.

In this recovering economy, if

Denver is Colorado Springs’ older

brother and they are in economic

“school” together, Colorado Springs

was held back a grade in 2014.

Recovery of the Colorado Springs

market is well behind the 12- to

18-month lag we have grown to

expect.

Simply driving through each city

provides proof of the longer-than-

normal lag. In Denver there is new

commercial construction in every

quadrant. New homes are being

built in creative new developments,

and young people are attracted to

Denver for careers with established

companies as well as start-ups

and high-tech. In Colorado Springs

commercial construction is almost

nonexistent, new home construc-

tion is stagnant at recession rates

and well-qualified workers are mov-

ing to vibrant markets to the north.

These factors all have an impact

on the retail market in Colorado

Springs.

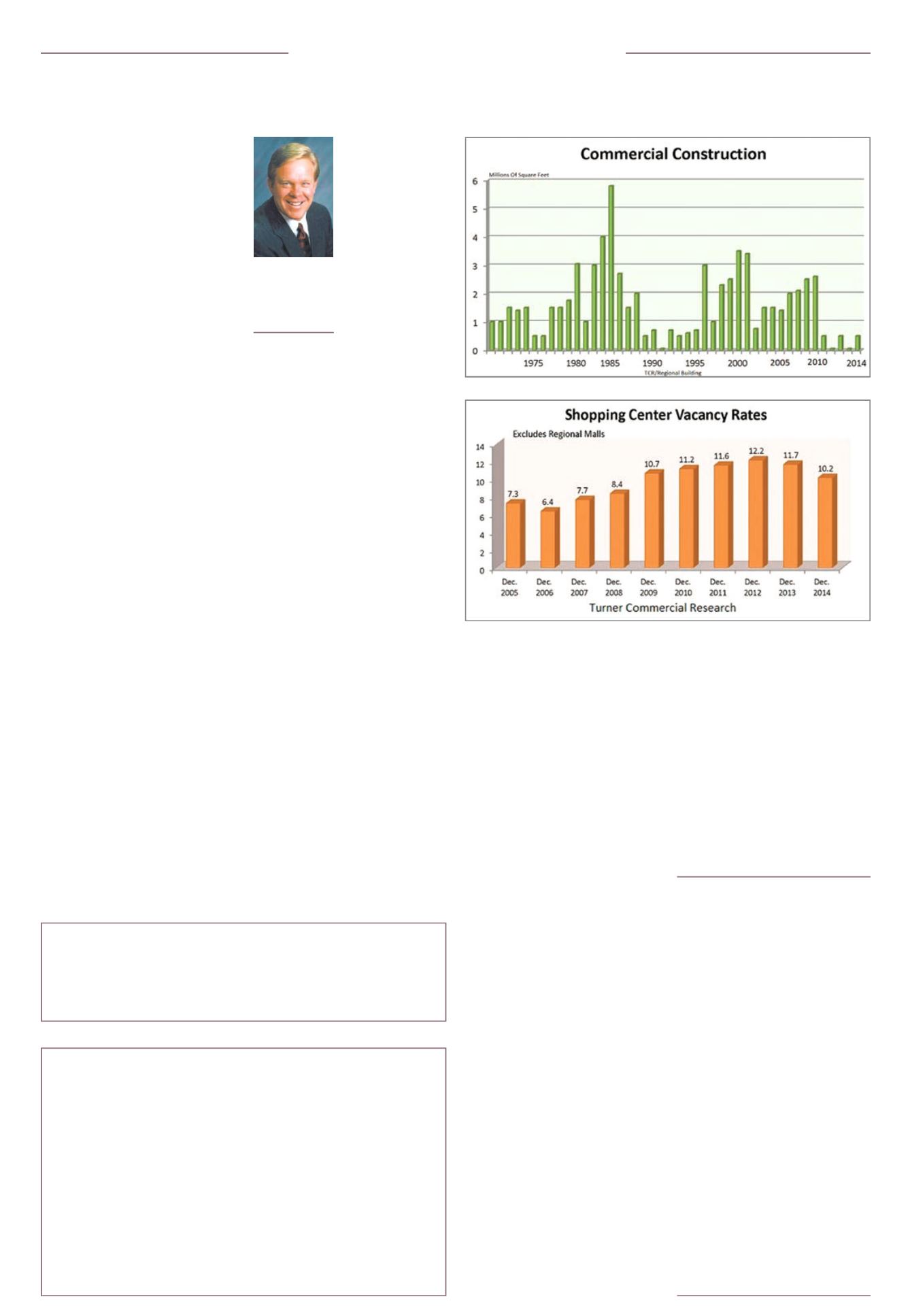

Retail vacancy and absorption.

Tur-

ner Commercial Research reports

that overall retail vacancy rates

reached a historic low in Colorado

Springs in 2006 at 6.4 percent. Rates

rose each year after that, to a high

vacancy rate of 12.2 percent at the

end of 2012. (2014 ended with a 10.2

percent retail vacancy rate.)

Absorption (the change in the

amount of occupied space from one

period to another) was negative in

2011 and 2012, meaning the amount

of leasing activ-

ity could not sur-

pass the increases

in vacant space.

Positive absorption

numbers returned

in 2013 and 2014,

chiseling away

at the vacancy

rates. However, the

vast difference in

commercial con-

struction activity

between Colorado

Springs and Den-

ver is similar to

that of each city’s

largest retail corridors, suggesting

that Colorado Springs may have

greater vacancy issues than the

overall numbers indicate.

Colorado Springs has two main

retail corridors – Academy Boule-

vard and Powers Boulevard. Acad-

emy Boulevard’s retail properties

were built during the 1970s and

1980s, while the retail on Powers

Boulevard was built in the mid-

1990s through today. To get the true

vacancy numbers of what is appar-

ent when driving through the two

main retail corridors, I looked at the

vacancy rates reported in Turner’s

year-end edition on individual

shopping centers on Academy Bou-

levard and Powers Boulevard. The

charts show my nonscientific find-

ings. (The numbers do not include

regional malls.)

From a visual inspection of each

of these retail corridors, the vacan-

cy rates on Academy Boulevard are

in excess of the overall stated retail

vacancy rate of 10.2 percent. How-

ever, it is more surprising to see

high vacancy rates throughout the

Central Academy area as well as for

unanchored centers in the North

Academy area. The other revela-

tion according to these numbers

is that the South Academy retail

area, long considered the stepsister

to all north locations, has much

better occupancy than the Central

Academy area in anchored shop-

ping centers and has equal or better

occupancy in unanchored centers

than any other section of Academy

Boulevard or Powers Boulevard.

In general, the newer anchored

retail centers throughout Colo-

rado Springs, built with a much

lower percentage of small retailer

space, are very well occupied with

strong national retailers. The older

anchored centers, built with equal

portions of anchor space and small-

er tenant spaces, are struggling to

find local or national tenants to fill

their vacancies. Unanchored centers

throughout the city are experienc-

ing high vacancy rates as well.

Retail building sales.

According

to Turner, 57 retail properties were

sold in Colorado Springs in 2014,

the fewest number of transactions

since 2010. Of the 57 sales, 29 were

sold to investors (not owner/users).

The average price per square foot of

all sales was $92.72.

On a national basis, there is great

demand for quality retail properties

from investors. This has driven cap-

italization rates down to unheard of

levels for quality properties (a low

capitalization rate produces a high-

er sales price). While these ultra low

cap rates are now the norm in the

Denver market, Colorado Springs

is still abundant in higher cap rate

opportunities, getting investors

more for their money.

There are bright spots in the Colo-

rado Springs retail market: Univer-

sity Village on North Nevada Avenue

continues to bring in strong nation-

al retailers. Some of the retailers

are new to the market, like Trader

Joe’s and Bass Pro shops, which

opened in 2014 at Northgate Road

on Interstate 25. The development

is expected to announce many new

retailers soon. Walmart Express is

in the process of opening five new

stores in the market, helping to

absorb several big-box vacancies.

The First and Main development

on Powers Boulevard continues to

attract the highest-quality retailers

to the market.

The overall story in the retail

commercial real estate market in

Colorado Springs is one of opportu-

nity. The day is coming for Colorado

Springs to catch up to the frantic

economic pace of its big brother

to the north. There are opportuni-

ties to purchase existing healthy

retail centers and reposition them

in the market. On the other hand,

there are opportunities to purchase

existing struggling retail properties,

raze them and create entirely new

mixed-use developments. Either

way, there are several opportuni-

ties for investors to purchase retail

properties at great prices relative to

other markets. It’s time to seize the

opportunity.

s

Retail lagging but offers opportunity for investorsColorado Springs Update

Jay Carlson

Principal,

managing broker,

Front Range

Commercial,

Colorado Springs

Shopping Centers

Size

Vacant Space

Vacancy Rate

53 (anchored)

12,064,000 sf

713,000 sf

5.9 percent

272 (unanchored)

7,603,000 sf

1,286,000 sf

16.9 percent

325 (total)

19,668,000 sf

2,000,000 sf

10.2 percent

Turner Commercial Research vacancy statistics year-end 2014

Academy Boulevard

Anchored

Unanchored

North Academy

8 percent

23 percent

(Interstate 25 to Union Boulevard)

Central Academy

35 percent

24 percent

(Union Boulevard to Platte Avenue)

South Academy

21 percent

18 percent

(Platte Avenue to Highway 115)

Powers Boulevard

Anchored

Unanchored

Fountain Boulevard

5 percent

18 percent

to Woodmen Road

North of Woodmen Road

5 percent

30 percent

Carlson’s vacancy rate findings for the two main retail corridors

The day is

coming for

Colorado

Springs to

catch up to

the frantic

economic

pace of its big

brother to

the north.