4 / 24

4 / 24

Page 4

— Retail Properties Quarterly — February 2015

R

etail is back on the scene in

Denver with plenty of activ-

ity. Last year’s activity was

marked by declining vacan-

cies, increasing rents and

several new national retailers enter-

ing the market. A strong local econ-

omy, population and employment

growth, increasing personal income

and a booming residential market

all contributed to

the retail sector’s

resilience. 2015 will

be another positive

year in the sector,

as the underlying

fundamentals in

the Denver metro

area remain strong.

Notable lease rate

growth is antici-

pated to occur in

the next 12 to 18

months due to

space scarcity in

A-trade areas such

as Cherry Creek, Park Meadows,

downtown and Boulder, along with

moderate construction activity.

Consumer activity was heightened

in the metro area, Colorado and the

U.S. during 2014, with retail sales

increasing by 8.1 percent in the U.S.

through October. Sales at the state

level through May (the latest data

available at the time of this article)

were up 5.5 percent, and in Denver

sales increased by 3.4 percent over

last year. Consumer sentiment is

also vastly improved, being pushed

by cheaper gasoline and rising home

prices in the area. As of December

2014, consumer sentiment in the

region rose 19.4 percent over 2013,

according the Mountain Region’s

consumer confidence index.

Twenty new national retailers

entered the market in 2014, with

more expected in 2015. New retail-

ers are drawn to Denver for several

reasons, including the above-average

personal income levels, steady popu-

lation growth and the region’s solid

residential market. Very few retailers

are leaving the Denver market and

business failures are still at a his-

toric low.

Residential development, includ-

ing a strong multifamily market,

contributes largely to retail health

because it amplifies consumption of

home furnishings, appliances and

accessories. For example, Conn’s

Home Plus, a home furnishings,

electronics and appliance store,

entered the market last year with

six new stores in Colorado’s Front

Range.

The region’s healthy retail mar-

ket benefits from a flourishing

restaurant scene. According to the

National Restaurant Association,

Colorado ranked fifth in the nation

for projected restaurant sales growth

in 2014. While national chain res-

taurants still seek opportunities in

the market, some of the best growth

has been in fast-casual concepts and

chef-driven restaurants. Quick-serve

restaurants posted a strong year in

2014 with several new QSR options

added to the market, such as Protein

Bar and Pizzeria Locale. We expect

this trend to continue in 2015, along

with the expansion of several proven

national sit-down chains, like Del

Frisco’s Grille.

Colorado is also the nation’s lead-

ing craft beer producer, with over

175 breweries and counting. While

the larger breweries typically are

in industrial spaces, many smaller

breweries seek space in key retail

areas.

A very competitive grocery mar-

ket will strengthen further in 2015.

Some short-term vacancies and

shifting are expected in the wake

of the recent merger of Safeway

and Cerberus, Albertsons’ parent

company, but new stores likely will

absorb the extra space. While 2014

saw the entry of Trader Joe’s to the

market, there were also several new

stores opened by Sprouts, Whole

Foods, King Soopers and Walmart

Neighborhood Market following

residential growth patterns. Look-

ing forward, the Union Station area

of downtown will add two large

grocery stores. A King Soopers is

currently under construction and

Whole Foods announced it will build

a 56,000-square-foot store in the

area as well.

Denver’s urban core is now a place

where people go to live, work, stay

and play. Further redevelopment of

obsolete space is expected in urban

and infill areas in the near term as

quality space becomes even scarcer

and in higher demand. The market

also will see mixed-use construc-

tion along transit lines following the

substantial expansion of the region’s

commuter and light-rail network.

For example, the city of Westminster

is in the final stages of approving

plans for the Westminster Center – a

105-acre transit-oriented, mixed-use

development on the site of the old

Westminster Mall, which includes

a significant share of land planned

for retail. Vertical construction may

begin as soon as the third quarter.

Despite encouraging demand

trends, local retailers will face new

issues and ongoing challenges in

2015, ranging from big-box store

consolidations to e-commerce.

E-commerce sales account for an

increasing share of total retail sales

in the U.S., but remain a minor con-

tributor overall. Total e-commerce

sales increased 16.2 percent from

third-quarter 2013 to third-quarter

2014, while total retail sales grew

only 4.2 percent. However, third-

quarter 2014 e-commerce sales

represented only 6.6 percent of total

retail sales in the quarter. Stores

are increasingly incorporating

omnichannel strategies to appeal

to multidimensional shoppers and

this trend is becoming increasingly

present in Denver. For example,

sporting goods store Sierra Trading

Post, which made its Denver debut

in 2014, offers customers an exten-

sive online catalogue and an in-store

pick-up option.

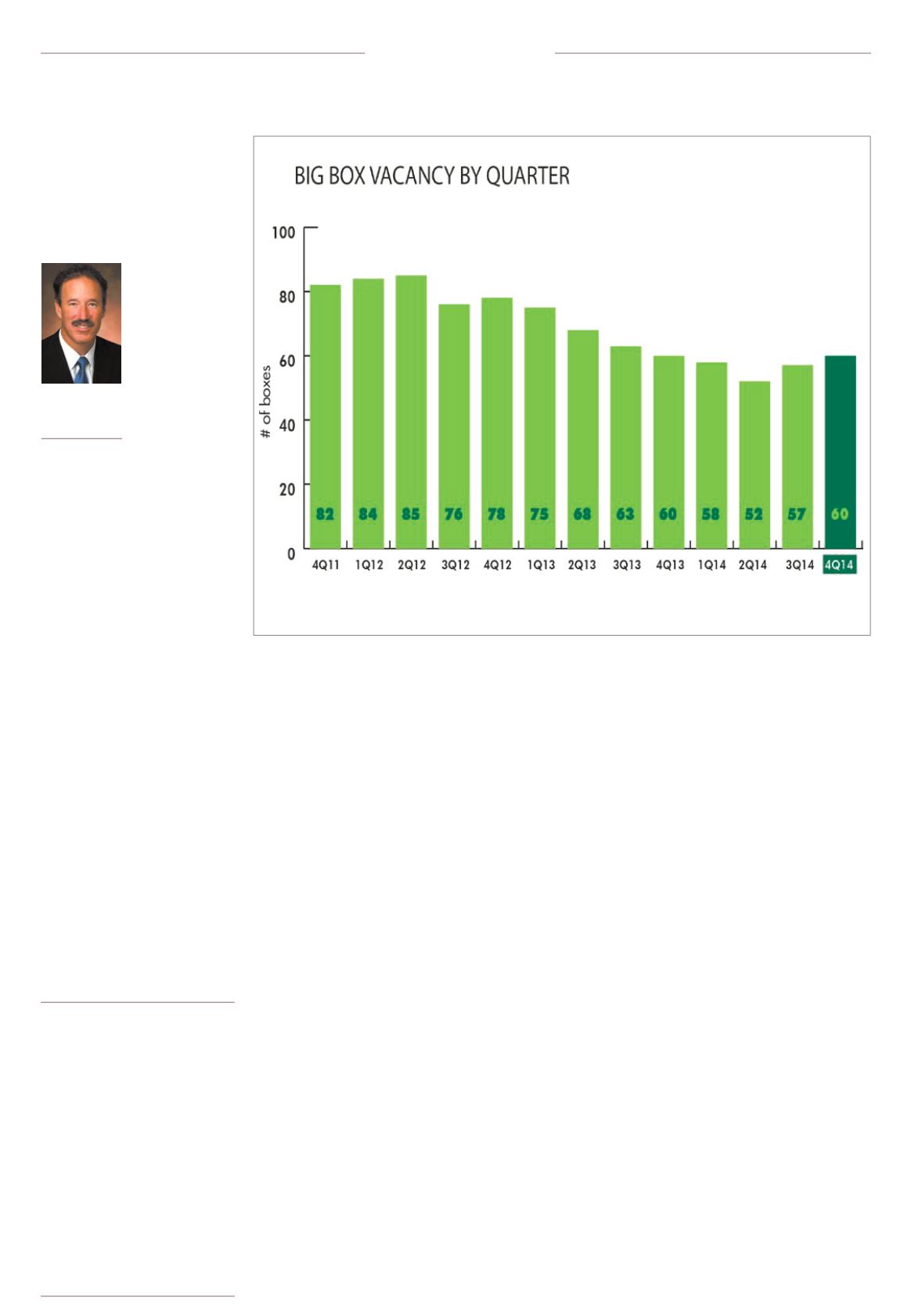

While big-box stores were expand-

ing rapidly in the 1990s and early

2000s, a notable change in consumer

habits led to smaller boxes becom-

ing more desirable. Centers in key

locations have repositioned or split

their boxes to accommodate new

users, thereby sustaining low vacan-

cy rates in the A-trade areas. How-

ever, in secondary trade areas, the

market is readjusting and nontradi-

tional users are finding these left-

over big-box spaces suitable for their

product. Fitness clubs, churches,

self-storage centers and entertain-

ment venues like trampoline parks

signed some of the largest leases

in terms of square footage in 2014.

Nontraditional use of these spaces

will likely increase and the market

will also see redevelopment of obso-

lete big boxes.

Year-end vacancy in the market

stood at 6.5 percent, which was

the lowest level since 2008, when

vacancy bottomed out at 6.4 per-

cent. Availability in the market

reached 10 percent in fourth-quarter

2014, its lowest level in six years.

These figures are reflective of an

overall tightening of the market

around high-quality space, a trend

especially evident in the Colorado

Boulevard/Midtown submarket,

which has the greatest proportion

of high-quality space and the mar-

ket’s lowest vacancy rate at less

than 3 percent. Asking lease rates

are reflective of these conditions,

averaging $24.35 per sf triple net in

fourth-quarter 2014. This submarket

contains premium retail space in the

Cherry Creek North area, which is at

market-setting rates. A few highly

anticipated mixed-use projects are

under construction there.

The overall market experienced

an average lease rate of $15.80 per

sf triple net in the final quarter of

2014, with a 45-cent increase year

over year and the highest rate the

market has seen since 2011. In light

of robust consumerism, as well as

continued broad-based economic

growth, ongoing construction and

overall positive absorption, Denver

retail likely will continue on a path

of restrained expansion through

2015.

s

All signs point to positive vibes for Denver retailRetail Outlook

Jon Weisiger

Senior vice

president, CBRE,

Greenwood Village

Year-end vacancy

in the market stood

at 6.5 percent,

which was the

lowest level

since 2008, when

vacancy bottomed

out at 6.4 percent.