16 / 32

16 / 32

Page 16

— Office Properties Quarterly — March 2017

January jobs report far exceeds expectationsJ

ob growth in January blew

past expectations, with some

analysts attributing the

increase to “animal spirits” – a

term coined by John Maynard

Keynes to describe the willingness

of households and businesses to

spend and invest.

Employers added 227,000 net new

payroll jobs in January, well above

the 2016 average of 187,000 and

beating Bloomberg’s survey of econ-

omists, which forecasted 180,000.

Revisions to November and Decem-

ber data subtracted 39,000 jobs.

Sectors that added jobs last

month included retail trade, adding

45,900; professional and business

services, adding 39,000; construc-

tion, adding 36,000; finance, add-

ing 32,000; and restaurants, adding

29,900. The surge in retail hiring,

which seems at odds with post-

holiday layoffs in department and

clothing stores, may be related to

seasonal adjustment factors. Health

care added 18,300 jobs, trailing its

six-month average. Manufacturing

as well as the mining and logging

sector added 5,000 and 4,000 jobs,

respectively; manufacturers contin-

ued to struggle with exports, while

employment in the mining and

logging sector is stirring thanks to

firming oil prices. The only two big

sectors to shed jobs were govern-

ment, losing 10,000 jobs, with most

of the loss in education; and trans-

portation and warehousing, losing

4,000.

Wages increased by 0.1 percent

last month and by 2.5 percent over

the past 12 months, below recent

trends.

The unemploy-

ment rate ticked

up a notch to 4.8

percent, pushed

higher by a surge

in the labor force

of 584,000. This,

in turn, pushed

up the labor force

participation rate

by 0.2 percentage

points to 62.9 per-

cent. The U-6 rate,

which includes

labor market slack

not picked up in

the unemployment

rate, increased from 9.2 percent to

9.4 percent.

There were three key takeaways

from the January employment

report.

First, the labor market may

already be reacting to the business-

friendly policies proposed by the

Trump administration – corporate

tax cuts, infrastructure spending

and regulatory relief – even though

these policies are still in the for-

mative stages and may not kick in

until late this year or 2018. Small

businesses, in particular, may be

encouraged by the prospect of less

red tape.

Second, wages grew last month

but at a slower pace than in previ-

ous months, suggesting that stron-

ger inflation is not necessarily right

around the corner. This provides

some cover for the Federal Reserve

to push interest rates higher at a

measured pace.

And third, analysts disagree about

how much faster employment can

grow given that unemployment is

low and the labor market is near

full employment. Nevertheless,

there is room for “animal spirits”

to have some impact on hiring and

spending, which will support leas-

ing activity in commercial proper-

ties and postpone the onset of the

next recession.

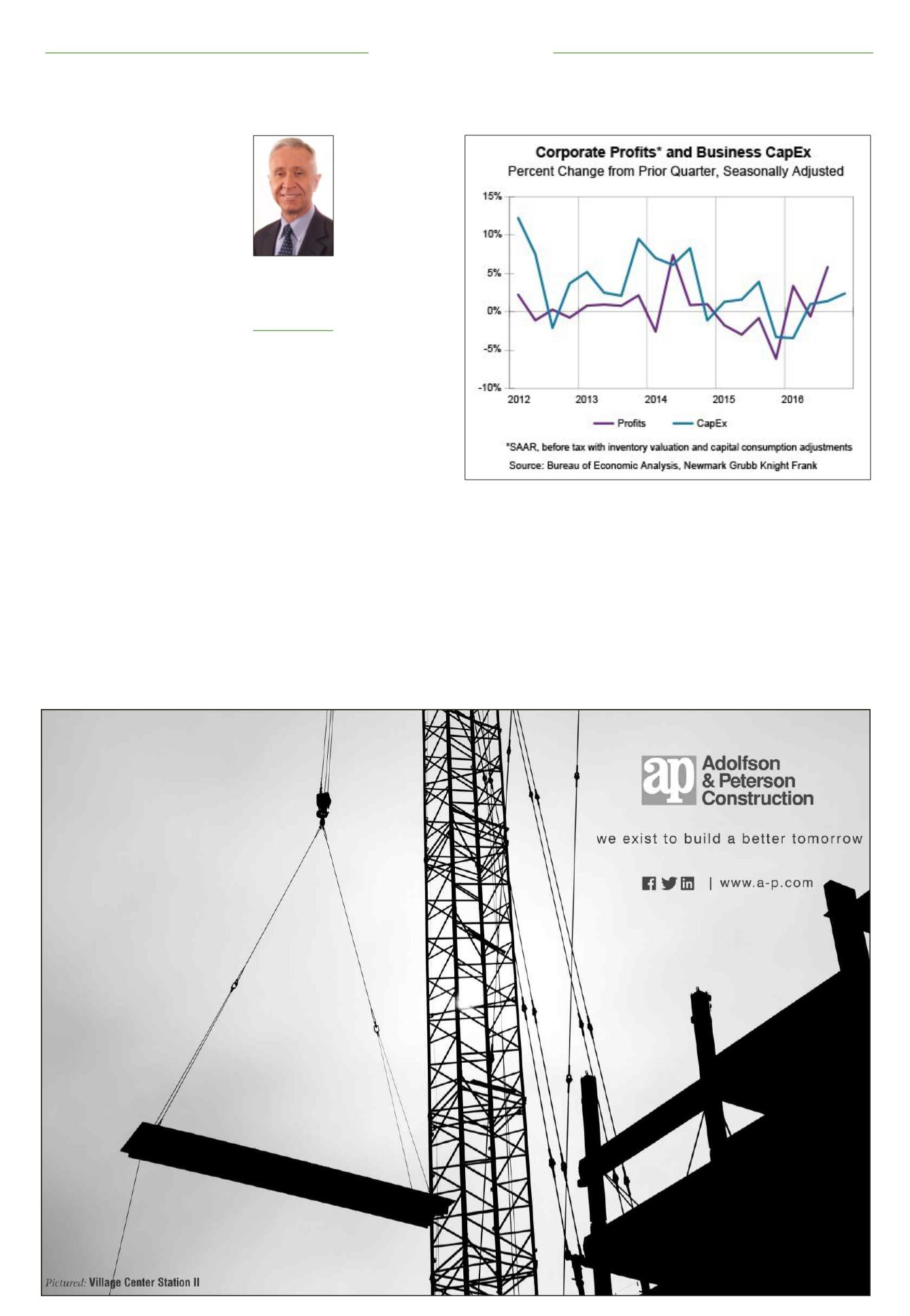

Supply and Demand

Which comes first, demand or

supply? Economic supply-siders

contend that a healthy business

sector is the foundation for a

healthy economy, making it easier

for businesses to offer goods and

services at low prices, and demand

for their products will follow. Yet as

important as businesses are in any

capitalist economy, business capital

spending accounted for 12.4 percent

of the gross domestic product last

year, whereas consumer spend-

ing accounted for 68.7 percent,

based on data from the Bureau of

Economic Analysis. Therefore, a

robust consumer sector will create

Bob Bach

Director of

research-Americas,

Newmark Grubb

Knight Frank,

Chicago

Please see ‘Bach,’ Page 28Market Drivers