4 / 36

4 / 36

Page 4

— Multifamily Properties Quarterly — November 2017

www.crej.comMarket Update

*As of 12/31/2016.

© 2017 PGIM is the primary asset management business of Prudential Financial, Inc. (PFI). PGIM Real Estate Finance is PGIM’s real estate finance business. Prudential, PGIM, their respective logos as well as the Rock symbol are service

marks of PFI and its related entities, registered in many jurisdictions worldwide. PFI of the United States is not affiliated with Prudential plc, a company headquartered in the United Kingdom.

THE FUTURE OF REAL ESTATE

FINANCING IN COLORADO:

PGIM REAL ESTATE FINANCE.

PGIM Real Estate Finance combines one of the industry’s most experienced teams with

extensive lending capabilities and consistent performance in the Colorado market.

We originated over $6 billion* in multifamily loans in 2016 and focused on a

variety of specialized property types including: market rate housing, affordable

housing, student housing, senior housing and health care senior living.

Partner with our experts a

t PGIMREF.com or contact:

Jay Porterfield

(214) 777-4533,

Jay.Porterfield@pgim.com PGIMREF.com/LinkedInR

enting is at historically high

levels, and despite all the

cranes in major metro areas

across the country, includ-

ing Denver, supply is simply

not keeping up with demand.

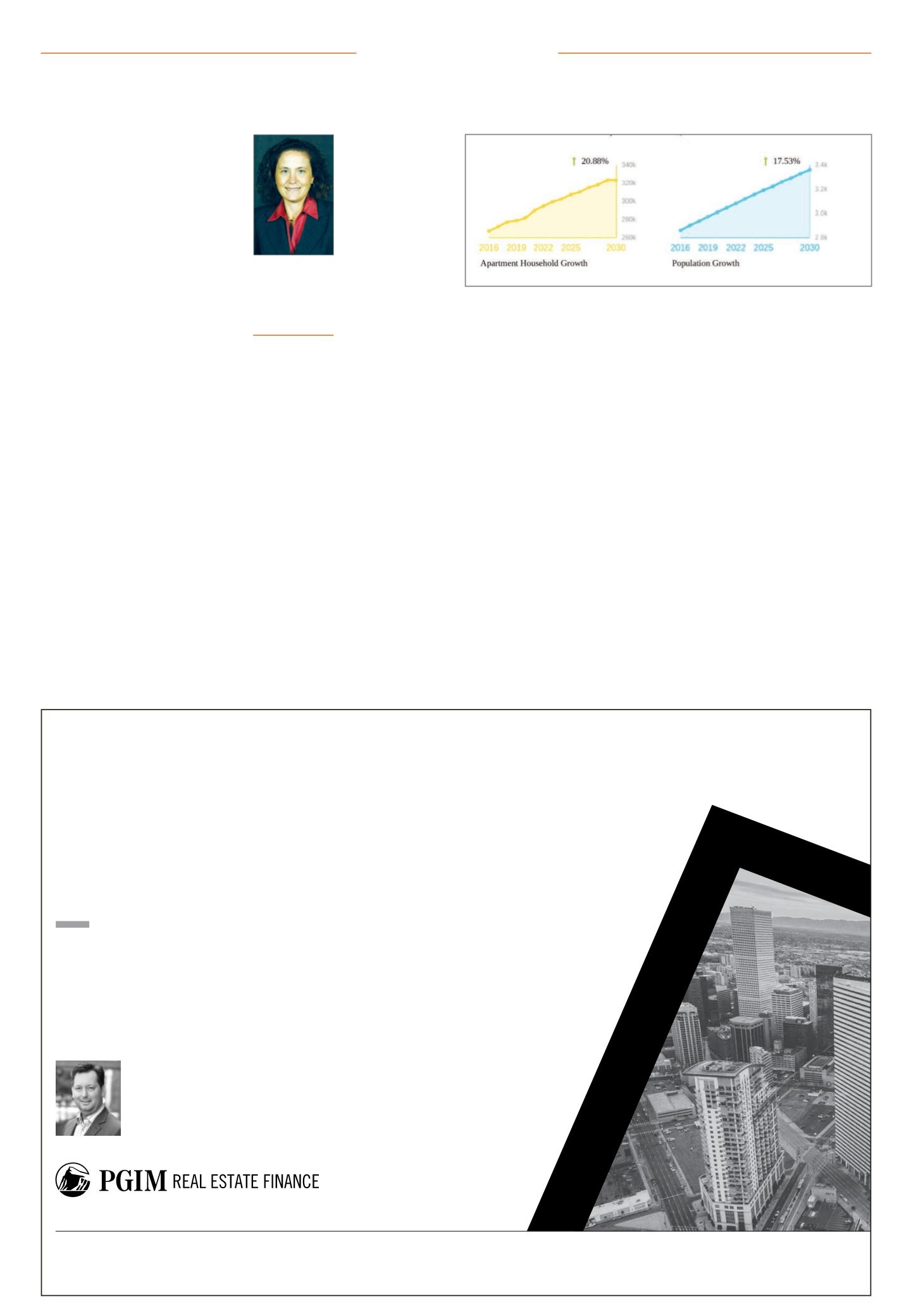

Nationally, the U.S. will need 4.6

million new apartments by 2030,

according to a new study produced

by Hoyt Advisory Services and com-

missioned by the National Multi-

family Housing Council and the

National Apartment Association.

Hitting that number will require

an average of at least 325,000 new

apartment homes every year; yet,

on average, just 244,000 apartments

were delivered from 2012 through

2016. The last time the industry

built more than 325,000 in a single

year was 1989. To add to the chal-

lenge of accommodating 4.6 million

apartment households, as many as

11.7 million existing apartments

could need to be renovated or risk

being lost from the stock.

The research, which examines

rental demand in all 50 states and

in 50 major metro areas, finds that

Colorado will need 100,000 more

apartments by 2030, and 56,000 of

those will be needed in Denver.

•

Surge in demand.

We’re experi-

encing fundamental shifts in our

housing dynamics, as more people

are moving away from buying

houses and choosing apartments

instead. Every year for the past

five years, the U.S. has averaged 1

million new renter households, a

record amount.

There are several factors behind

this surge. Much has been writ-

ten about the millennials, and it’s

true that more

than 75 million

people between

18 and 34 years

old are entering

the housing mar-

ket, primarily as

renters. But rent-

ing is not just for

the younger gen-

erations anymore.

Increasingly, baby

boomers and other

empty nesters are

trading single-

family houses for

the convenience

of rental apartments. In fact, more

than half of the net increase in

renter households over the past

decade came from those aged 45 or

older.

Demographics are driving mean-

ingful lifestyle changes that are

being expressed through our hous-

ing choices. In 1960, 44 percent

of all households in the U.S. were

married couples with children – the

prime drivers of homeownership.

Today, it’s less than one in five (19

percent), and this decline is expect-

ed to continue.

Immigration also is an important

factor. Approximately half (51 per-

cent) of all new population growth

will come from immigration, and

research has shown that immi-

grants have a higher propensity to

rent and typically rent for longer

periods of time.

•

The supply gap.

In a perfect mar-

ket, the private sector would step

up and fill the growing demand. But

anyone who has ever developed an

apartment property knows there is

no such thing as a perfect market.

Land shortages, local regulations,

complicated permitting processes

and more conspire to make it dif-

ficult for developers to deliver the

necessary supply. They also drive up

prices that make delivering apart-

ments at a wide range of prices

nearly impossible.

The NMHC/NAA-commissioned

research also ranked the top 50

metros to identify cities where it’s

hardest to build new apartments

with a Barriers to Apartment Con-

struction Index. Denver ranked in

the top 10, coming in at No. 9.

If Denver is serious about address-

ing its housing shortage, it will need

to take a hard look at the obstacles

that are delaying or increasing the

cost of new apartments.

•

Policies to bridge the gap.

While

the number of new apartments

built each year has been rising, it

hasn’t been enough to meet current

demand and make up for any pos-

sible shortfall at certain price points

in the years following the reces-

sion. This imbalance between high

demand and limited supply options

has driven down affordability and

reduced housing options for rent-

ers. We’ve seen that firsthand in

Denver, where average metro rents

are up $700 per month since 2004.

For many reasons, building apart-

ments has become costlier and

more time-consuming than it needs

to be. Over the past three decades,

not only have hard costs like land

and materials risen sharply, but

regulatory barriers to apartment

construction also have increased

significantly, most notably at the

local level.

These obstacles to development,

such as outdated zoning laws,

unnecessary land use restrictions,

arbitrary permitting requirements,

inflated parking requirements,

CO will need 100K more apartments by 2030Kim Duty

Senior vice

president, public

affairs, National

Multifamily

Housing Council,

Denver

Please see Duty, Page 32National Multifamily Housing Council, National Apartment Association

New research shows that demand for apartments is on the rise. Whether it’s young professionals,

couples, families or empty nesters, Denver will need to add 56,000 new apartment households

by 2030.