6 / 40

6 / 40

Page 6

— Multifamily Properties Quarterly — August 2017

www.crej.comO

verall, the Colorado market

has been strong through the

first half of 2017.The state

has absorbed over 5,500 units

and average effective rent

has increased about 5.1 percent.The

number of units absorbed this year is

higher than in the first half of 2016 and

2015, by about 2,000 units and 1,200

units, respectively. Overall occupancy,

as of the end of June, was at 93 percent,

a slight increase from the 92 percent

average in the previous six months.

For a closer look at the market condi-

tions, it’s helpful to look at the move-

ment in key indicators such as average

effective rent growth, occupancy and

absorption in each asset class.

Class A properties have performed

well when compared to the previous

two years, but there are signs that the

level of new construction is starting

to drag down effective rent growth.

In the first half of 2017, we’ve seen

almost 1,700 Class A units absorbed, an

increase from the 1,500 in the first half

of 2016 and the 1,470 in the first half of

2015.

However, there is some softness in

effective rent growth.While still posi-

tive, average effective rent grew by only

3.8 percent in the first two quarters, a

noticeable drop from the 6.3 percent

increase in 2016 and the 6.6 percent

increase in 2015.This is signaling that

the top of the market is feeling the

influx of new construction units enter-

ing the market at an accelerated pace.

The silver lining is that despite the

slowdown in rent growth, occupancy

is trending in the right direction. As

of the end of June, average occupancy

was 82.8 percent.This is not an ideal

number, to be sure, but it does mark an

improvement from

the 79.6 percent

rate of the previous

period. Overall for

the top tier, average

effective rents are

up, average occu-

pancy is up and

absorption is up.

Class B proper-

ties have seen a

similar dynamic

play out regarding

these three indica-

tors. Absorption is

up compared to the

first half of 2016 and 2015. A little over

900 units have been absorbed in this

asset class in 2017, whereas 2016 saw

about 700 units absorbed and 2015 had

a negative value of nearly 375 units.

The positive trajectory also is pres-

ent for occupancy.With an average

occupancy this year of 92.6 percent,

the previous six month’s average

of 92.2 percent was ever so slightly

edged out. However, just as with Class

A, there has been some erosion in

effective rent growth. The new sup-

ply at the top if the market means

that some of the properties near the

threshold of Class A and Class B have

been bumped into the latter. This has

resulted in increased competition in

this price tier, although the condi-

tions are hardly bleak. In the first half

of 2017, the average effective rent

growth was a robust 5.7 percent. The

previous two years showed immense

price growth, however, and 2017 did

not keep pace. In 2016, the average

effective rent growth was 6.2 percent,

and in 2015 the figure was 8 percent.

Despite the decline in rent gains, there

certainly isn’t reason for concern in

the near term.

Class C also is on solid ground. After

absorbing 1,200 units on the first half

of 2015 and about 700 in 2016, 2017 saw

a huge increase to slightly over 2,700

units.This represents over half of the

total number of units absorbed in the

state through June. Additionally, average

effective rent growth improved from

the 3.7 percent rate of 2016 by a full 2

percent despite falling short of the 2015

6.5 percent growth. Occupancy also rose

1.5 percent from 92.8 to 94.3 percent,

a substantial improvement from 2015

and 2016, which were both under 1

percent through the first six months of

the year.

Class D has not kept pace with the

great start to the year in the other class-

es, but even here, the numbers aren’t

terrible. Absorption decreased by 50

percent from 2016 – but, at a little over

300 units, it is still better than the 2015

number of about 240 units. Additionally,

average effective rent has increased 2.7

percent, which is higher than 2016 and

2015, when both were under 2 percent.

Occupancy has increased by 0.5 per-

cent to 95.5 percent. Absorption in this

class can be shakier than the rest of the

market due to units lost to closure or

demolition.The lack of occupancy loss

and the improvement in effective rent

growth show that the Class D tier is in

good shape.

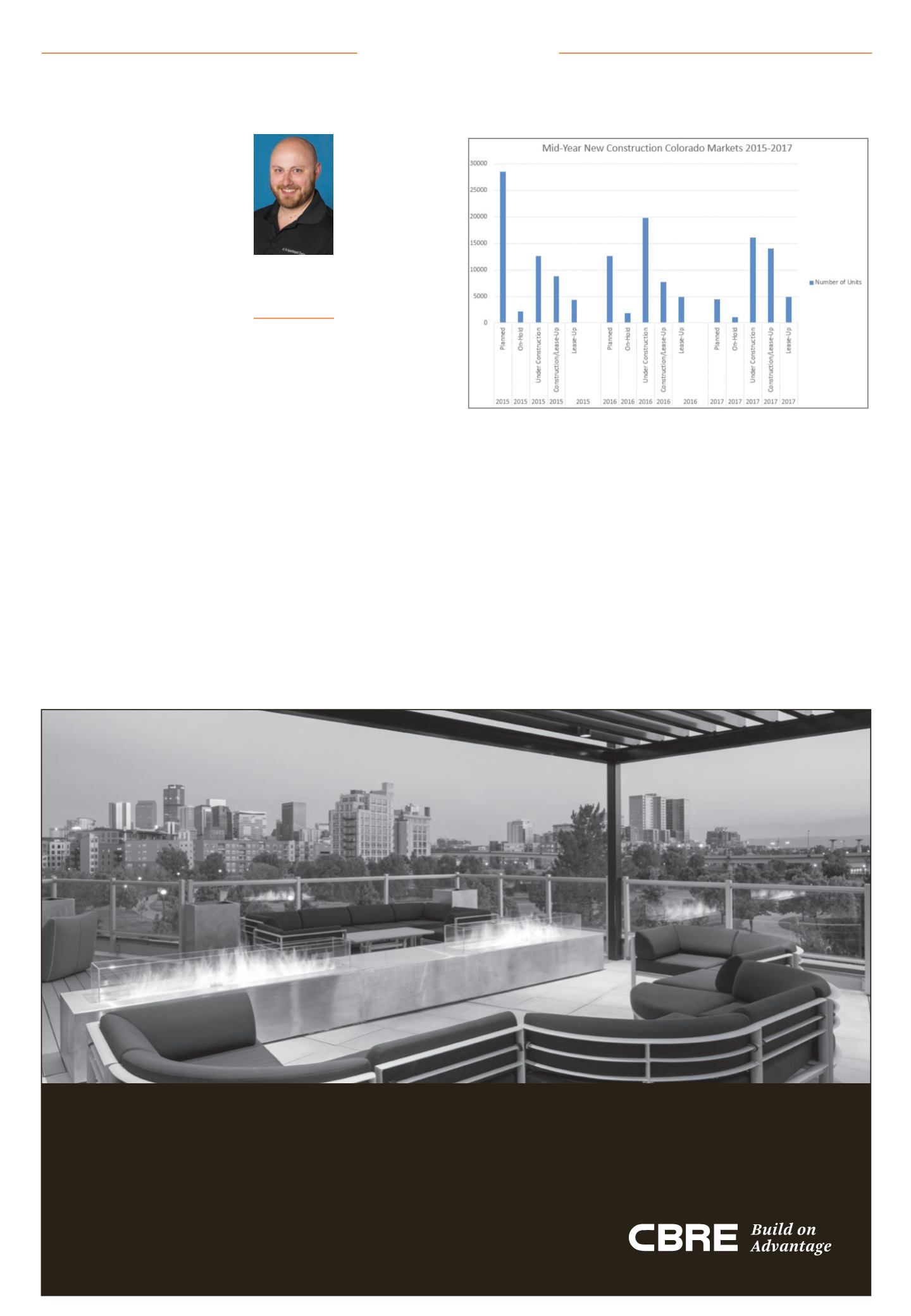

The driver for much of the movement

in these indicators is new construction,

Diving into asset class analysis from 2015-2017CBRE Debt & Structured Finance has closed nearly $1.1 billion in multifamily financing assignments over the last 12 months

in the state of Colorado. Nationally, CBRE Capital Markets is the non-bank industry leader in commercial real estate loan

originations. How can we help you transform your real estate into real advantage?

For more information contact:

Brady O’Donnell, Vice Chairman

303 628 1777

ADVANTAGE

DELIVERED.

Jeff Halsey, Vice President

303 628 1769

Jill Haug, Vice President

303 628 1782

Jordan Brooks

Account manager,

ALN Apartment

Data Inc.,

Carrollton, Texas

ALN Apartment Data Inc.

Please see 'Brooks,' Page 35Market Update