35 / 40

35 / 40

August 2017 — Multifamily Properties Quarterly —

Page 35

www.crej.comin the fall than in the spring. Fol-

lowing a dip in occupancy and rents

in the past five years, I have seen a

strong rebound in occupancy and

rental rates immediately after.

While condo development may

begin to ramp up given the recent

construction defect reform legisla-

tion, which was passed in the state,

and the favorable ruling by the Colo-

rado Supreme Court in the Vallagio

case, I don’t expect this to have a

significant impact on the apartment

market for several years, if not much

longer, due to ongoing high insur-

ance costs and a lack of developers,

insurers, contractors and architects/

engineers willing to take the risk on

condo developments as well as the

high cost to develop this product.

Given the strong tenant demand

for apartments, driven by ongo-

ing population and employment

growth and the supply constraints

mentioned, I expect to see deliver-

ies remain relatively staggered and

the apartment market continue to

expand for at least the next two to

three years, barring any unforeseen

black swan event.

V

in addition to employment and popula-

tion trends.There has been a clear shift

in the new construction pipeline over

the past few years, and its impact on

effective rent growth is clear.

We were tracking about 28,500 new

construction units in the planning phase

in 2015.That number slid to just over

12,000 in 2016 and was at 4,500 through

June. Projects under construction or

entering the early phase of lease-up

totaled about 21,000 units in 2015, about

28,000 units in 2016 and just over 30,000

units for 2017.The number of units in

full lease-up with construction com-

pleted has held steady at about 4,900 for

all three years.This all reflects a clear

movement from planning in 2015, to

construction and beginning of delivery

in 2016 and 2017. Looking ahead into

2018, the last remaining units of the

initial planning boom in 2015 will be

entering the market and will put addi-

tional pressure on the top asset tier that

already is showing some signs of rent

growth slowdown.

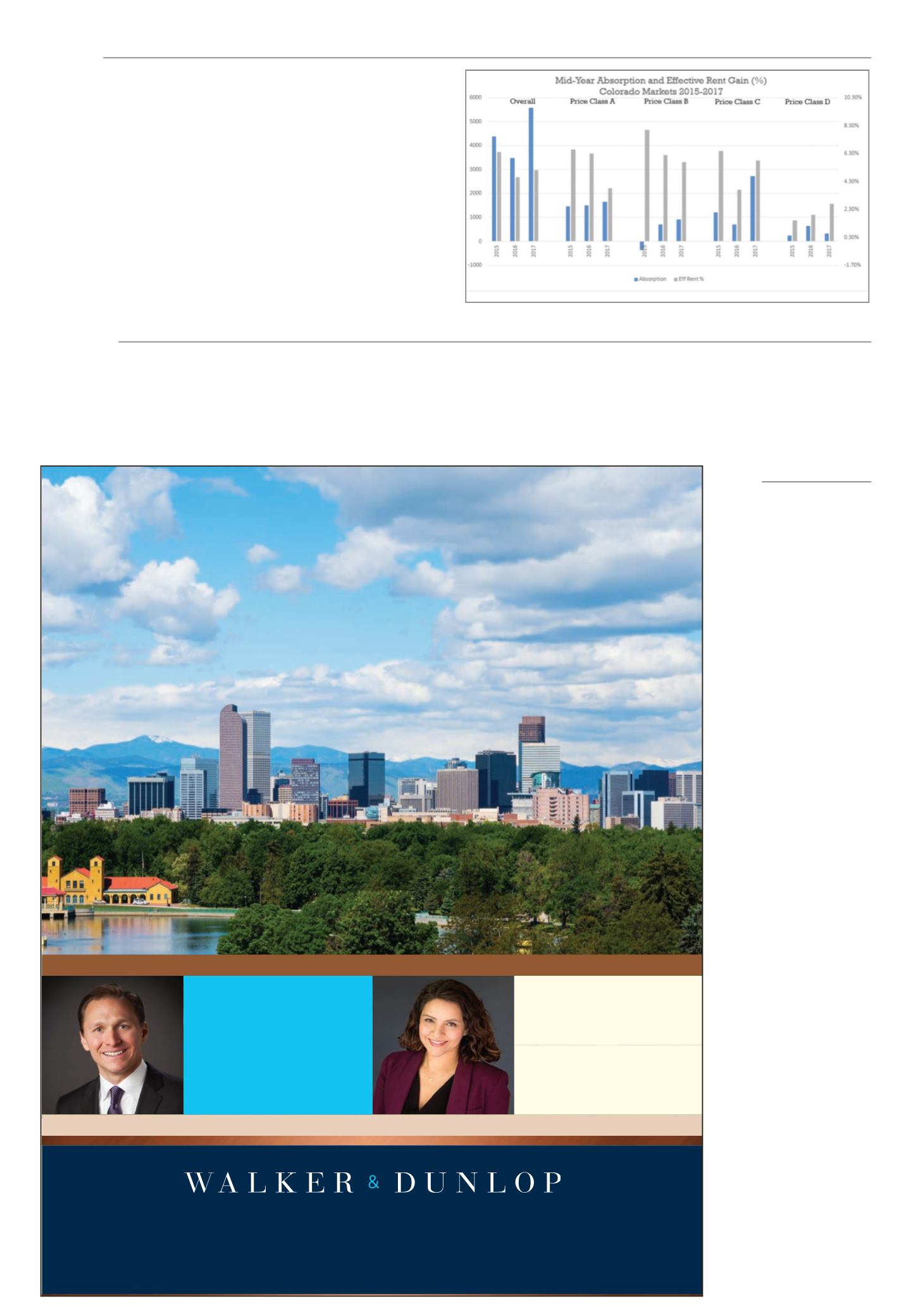

Multifamily overall in Colorado had

superior effective rent growth figures

in 2015 compared to both 2016 and

2017.This held true across all four asset

classes. However, the first half of 2017

saw the highest absorption overall and

across all classes, except D, for this

three-year timeframe. Colorado is a

growing market, and short of a prema-

ture increase in planned new construc-

tion, the outlook for the rest of 2017 and

the first half of 2018 is bright.

V

FANNIE MAE FREDDIE MAC HUD BRIDGE LIFE COMPANY INVESTMENT SALES

WalkerDunlop.comCalifornia loans will be made pursuant to Finance Lenders License #603H310 / BRE Broker #01982999.

IS CERTAINTY OF EXECUTION

AT THE TOP OF YOUR LIST?

TOP FOUR GSE LENDER IN 2016

1

#2 FANNIE MAE DUS

®

LENDER IN 2016

#3 FREDDIE MAC MULTIFAMILY APPROVED SELLER/SERVICER IN 2016

#4 HUD MULTIFAMILY LENDER IN 2016

97% HUD APPROVAL RATE

3

YOUR LOCAL FINANCING EXPERTS

1

MBA 2016 Commercial/Multifamily Annual Origination Rankings

2

Freddie Mac

3

34 HUD approvals out of 35 HUD submissions in FY 2016

ANTHEA MARTIN

Vice President

Real Estate Finance

anmartin@walkerdunlop.comMobile

720.891.6537

RALPH LOWEN

Senior Vice President

Real Estate Finance

rlowen@walkerdunlop.comPhone

720.439.3203

Mobile

303.520.9293

Brooks

Continued from Page 6Hallauer

Continued from Page 10and fully renovating them or

adding significant upgrades.

For example, in Colorado

Springs, there have been

dozens of Class C properties

renovated over the past 36

months, resulting in dramati-

cally increased rent levels and

property values.

Unlike stock in many

other Front Range markets,

value-add opportunities still

are abundant throughout

Aurora and Colorado Springs.

In Aurora, over the past 12

months, 1980s built proper-

ties have averaged around

$168,000 per unit, compared

to 1960s era properties aver-

aging just under $90,000 per

unit. Comparatively, Colorado

Springs’ older Class B and

C categories have seen less

fluctuation in price per unit

and sales volume based on

the decade of construction.

In 2016, apartment build-

ings constructed in the 1960s

and 1970s traded at around

$80,000 per unit, while 1980s

built construction traded at

$108,000, on average. As of

late, there have been sev-

eral sales, and current for-

sale product, at well above

$100,000 per unit for upgrad-

ed or well-located 1970s prod-

uct in both markets, continu-

ing to state the increasing

strength of the markets.

Firm economic growth and

market fundamentals should

continue to propel investment

activity throughout Colorado

Springs and Aurora in 2017

and 2018, with value-add

opportunities remaining more

prevalent in these markets

than most other Front Range

submarkets. Barring substan-

tial interest rate movement,

both multifamily markets

should remain competitive,

with increasing tenant and

investor demand, creating a

further decline in going-in

cap rates. Further, Colorado

Springs and Aurora continue

to attract new out-of-market

buyer pools, boding well for

continued seller confidence

throughout the rest of the

year and into 2018.

V

Price

Continued from Page 8ALN Apartment Data Inc.