27 / 28

27 / 28

May 2017 — Retail Properties Quarterly —

Page 27

www.crej.comSRS Real Estate Partners

Tony Pierangeli • Jim Hoffman

Joe Beck • Brian Hollenback • Austin Tillack

Tami Lord • Molly Bayer

SullivanHayes Brokerage –

Boulder

Michael DePalma • Sean Kulzer

David Dobek

SullivanHayes Brokerage –

Denver

Tom Castle • Chris Cook

Courtney Dahlberg Key • Mark Ernster

Mike Kendall • Emily Klimas

John Liprando • Grant Maves

Brian Shorter • Christopher Anton

Josh Burger • Bryan Slaughter

Mark Williford

Tebo Development Company

Stephen Tebo • George Levin

The Zall Company

Stacey Glenn • Stuart Zall

Trevey Land and Commercial

Mitch Trevey • Nick Nickerson • Jason Thomas

Unique Properties Inc.

Marc S. Lippitt • Scott L. Shwayder

Tim Finholm • Brad Gilpin • Phil Yeddis

Gannon Roth • Allen Freedberg

Samuel Leger

Valentiner & Associates

Sheri Valentiner

W.W. Reynolds Companies, Inc.

Chad Henry • Nate Litsey

Marty McElwain

WalderaScott Real Estate

Partners

Kimberly Waldera • Noah Waldera

Scott Nannemann • Paul Klink

Western Centers Inc.

Brian Pesch • Corey R. Wagner • Bill Singer:

Western Investor Network

Tony Hemminger • John Jumonville

Matt Ritter

WestStar Commercial

Tim Hakes • Kevin Hayutin

Michael Hayutin • Stephanie Keyes

Retail Broker Directory

RETAIL BROKER DIRECTORY

If your firm would like to participate in this directory, please contact Lori Golightly at

lgolightly@crej.com or 303-623-1148 ext. 102

over Target pharmacies. Target bene-

fits from CVS customers coming into

the store and CVS is able to expand

exponentially without the overhead

of opening new storefronts.

In 2017, Walgreens and FedEx

announced a partnership that will

put FedEx drop-off/pick-up centers

in Walgreens stores. More of these

types of retail partnerships should

be expected as retailers continue to

look for ways to streamline expens-

es.

•

Uniqueness matters.

Small stores

with unique products not at major

superstores are in demand. This can

be seen in online retailers opening

small storefronts as distribution

channels and in international retail-

ers finding the value of entering

the U.S. It is a tenant’s market, so

the new-to-market retailer offering

a unique product is a real catch for

property owners; therefore, the new-

to-market retailer often can negoti-

ate better rents and have the oppor-

tunity to expose its international

brand in a new market.

With an eye on these retail trends,

the city of Thornton is proving to

be on the forefront with these new

projects announced along the north

Interstate 25 corridor:

•Denver Premium Outlets, break-

ing ground in May, addresses the

savvy shopping mentality.

•The Summit and Topgolf,

approved to begin construction in

2017, are experiential/entertainment

concepts.

•ViewHouse Eatery and Bar,

approved for construction in 2017,

addresses the “eatertainment”

requirements for modern day res-

taurants.

Realistically, brick-and-mortar

stores aren’t going anywhere. There

is still an appeal for the sensory

experience of shopping – smelling,

touching, hearing and trying on.

However, the industry is evolving,

with online shopping no longer just

a support sales tool. Today, the brick-

and-mortar store may support the

online store. While both remain nec-

essary, the evolution leads to a con-

traction in the number of physical

storefronts with larger radius rings

between repeat stores.

Looking to the future, retail must

remain nimble to retain the capacity

to anticipate and respond to future

trends and support creative/sustain-

able retail development to ensure

the economic vitality of our commu-

nities.

s

Jacoby

Continued from Page 12has home delivery and grocery pick

up, and it recently started Live Nat-

urally, a new natural and organics

delivery service that carries in-store

brands including many that can

only be purchased online. Walmart

has in-store pick-up options and

is testing a home delivery concept

using Uber and Lyft for same-day

delivery. Whole Foods and Natural

Grocers have partnered with Insta-

cart to provide home delivery. And,

of course, Amazon is already mak-

ing inroads into traditional grocery

territory with its Prime Pantry divi-

sion. The company also is rumored

to be scouting out Denver locations

for its brick-and-mortar Amazon Go

concept.

The grocery business is alive

and well in Colorado even as new

methods of delivery, consolida-

tions and closures prune the cur-

rent store base. These trends bode

well for the market leaders who

innovate and adapt to changing

consumer habits that have caused

such pain in the traditional depart-

ment store sector.

The good news for those of us

who own grocery-anchored cen-

ters is that we may finally see a

leveling off of new grocery store

openings, which, while it may not

bode well for our development busi-

nesses, should strengthen sales at

the existing stores in our portfo-

lios. This would be a nice outcome

after years of worrying about ever-

increasing new competition dimin-

ishing the sales and values of our

current centers.

s

Ginsborg

Continued from Page 21PNC

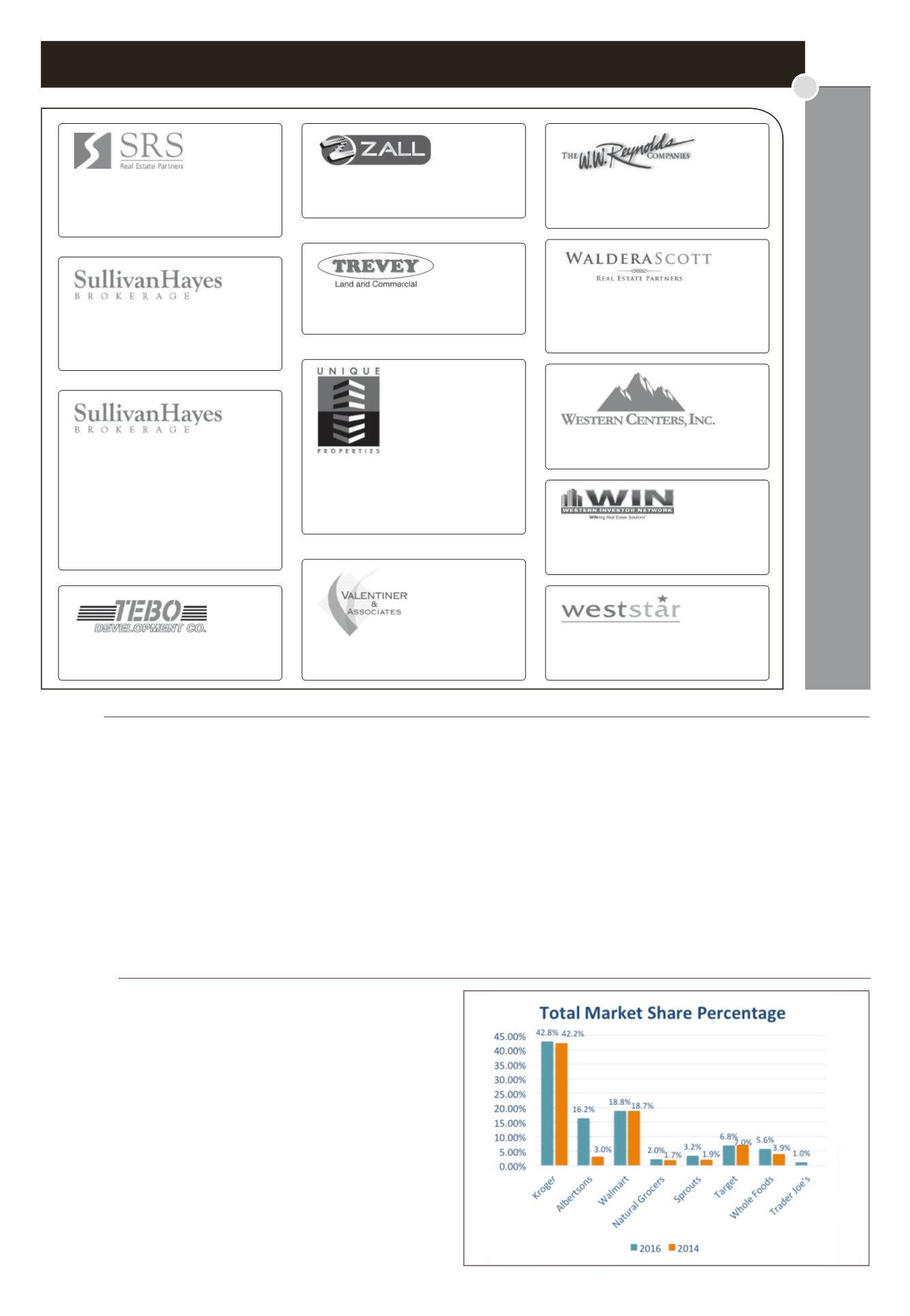

The total market share percentage of major grocers in Denver.