6 / 28

6 / 28

Page 6

— Retail Properties Quarterly — November 2016

W

hile making my daily

5-mile commute from my

house in Lower Highlands

to my office in the Baker

District, there are two

things that I always notice: traffic

and construction. It’s not hard to

spot cranes all over town, and Den-

ver’s population growth is evident

as soon as you get in your car. It’s

no secret that Denver has bounced

back quickly from the Great Reces-

sion, and population growth has

been a huge factor in the recovery.

While Denver’s multifamily market

has been the talk of the town, retail

property investors may be excited at

their prospects when evaluating the

growth in multifamily.

We believe that the multifamily

market may be a good leading indi-

cator for where the retail market is

headed for several reasons, but we’ll

focus on two here. The most impor-

tant is population growth because

retailers need to have customers in

order to pay rent to landlords. Since

a lot of people moving to Denver are

initially renters, we expect the rental

market to be a better indicator for

growth trends than the residential

sales market.

The other factor is multifamily

rental rates because, to a certain

extent, they are a reflection of the

health of the job market since new

residents need to be employed to

pay rent. While Denver’s multifamily

rental growth has been astounding,

it may be slowing down. Retailers

(and retail landlords) should wel-

come that because, absent a mar-

ket correction, retailers and retail

landlords can be the beneficiaries

of a slowing multifamily market.

Consumer confi-

dence is crucial to

the health of the

retail market. If

multifamily renters

believe that rents

will only continue

to go up, they will

be afraid to spend

money since they

will want to save

money to ensure

that they can con-

tinue to live in

Denver.

While Denver’s

job growth has

been strong, wages

have not kept up

with multifamily

rents, which is like-

ly a renter’s largest

expense. Along the

same lines, a con-

sumer’s disposable

income is crucial to

retailers. If a renter

is committed to

living in Denver at

all costs, then they

may forego other

expenditures (e.g.,

dining out, retail purchases) to stay

in Denver. When multifamily rent-

ers can more accurately predict their

expenses, they are more likely to go

out and shop without worrying if

what was disposable today should

have been saved for tomorrow.

Multifamily landlords have the

luxury of being able to quickly adjust

lease rates to the market because

leases usually are 12 months or

fewer and don’t involve complicated

tenant improvement allowances,

leasing commissions, lengthy mar-

keting times and other factors that

are a part of life of a retail landlord.

Retail landlords, on the other hand,

typically sign long-term (sometimes

20-plus years) leases with a lot of

moving parts, which helps to explain

some of the disparity between rental

growth between retail and multi-

family properties. Further, it is much

harder to lease a retail property in

a bad market because retailers may

completely halt their expansion

plans, even if rental rates plummet.

A multifamily developer is much

better equipped to make a deal work

in a bad market than a retail devel-

oper, particularly when rents need

to be at a certain (possibly unat-

tainable) rate for the deal to pencil

and/or satisfy a lender requirement.

Right before the Great Recession, a

Retail rent growth still enjoying long runwayJustin Krieger

Senior adviser,

Pinnacle Real

Estate Advisors,

Denver

Tom Ethington

Senior adviser,

Pinnacle Real

Estate Advisors,

Denver

Market Update

BRIGHTON, COLORADO

UNPRECEDENTEDGROWTH.

UNLIMITEDOPPORTUNITIES.

ACCELERATING

BUSINESS.

brightonedc.orgPinnacle Real Estate Advisors

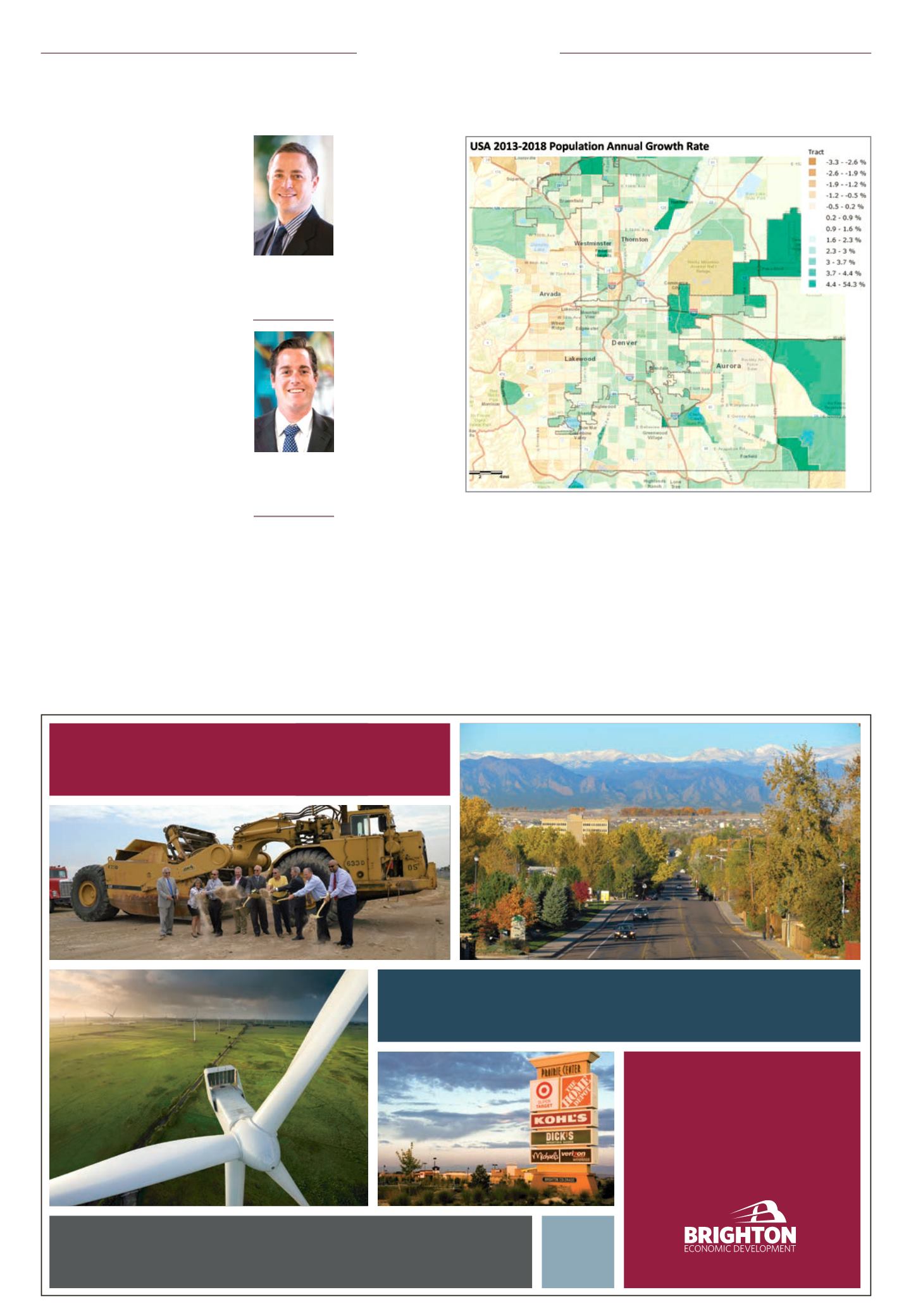

Denver’s population annual growth rate from 2013 to 2018.

Please see ‘Krieger’ Page 23