8 / 32

8 / 32

Page 8

— Office Properties Quarterly — September 2017

www.crej.comB

oisterous headlines do

not capture the full story

of office availability rates

throughout metro Denver.

To the untrained eye, every

crane in the skyline may appear to

be another office building and not

one of the many residential struc-

tures actually being built. If we are

not overbuilding office space and

1,000 people per month are mov-

ing to Denver, how can pockets of

office availability be as high as 23

percent?

There are undeniable highs and

lows in every submarket across the

city, especially in southeast subur-

ban Denver. Whenever office inves-

tors stumble upon such unfavorable

market data, they immediately look

for trends to explain away high

availability rates. Negative submar-

ket trends in SES point in every

direction from lead tenant mergers,

acquisitions and consolidations,

to urban migration to light-rail

proximity. There is not one evident

culprit for 19 percent availability

in SES, but there is a compelling

dumbbell curve theory to consider.

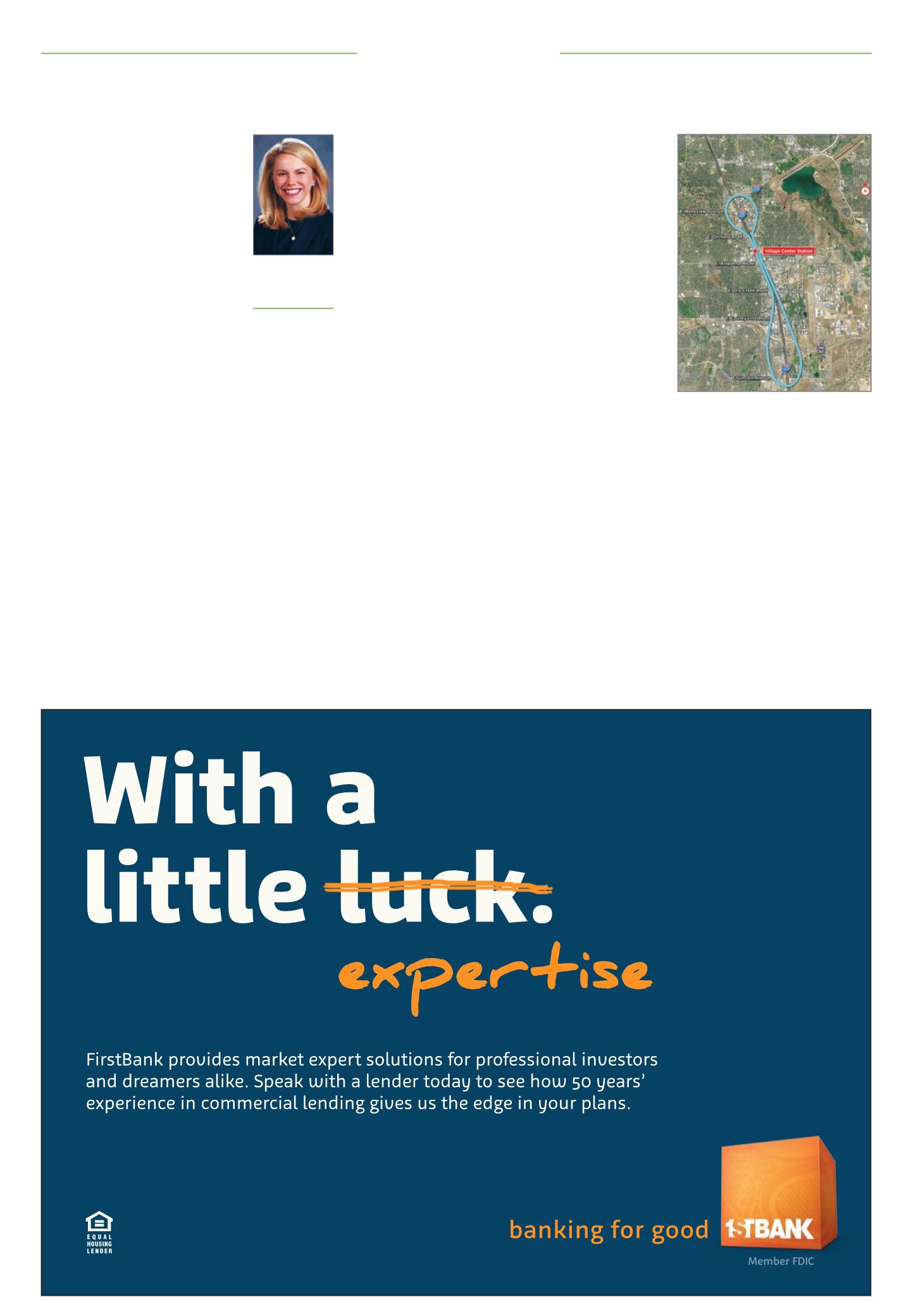

The flat part of the dumbbell

curve is at Village Center Station

(Arapahoe Road and Interstate 25).

This area is an “urb-suburban set-

ting,” which National Real Estate

Investor identifies as “one way to

describe the mash-up of suburban

office locations in walkable settings

with easy access to urban-style

amenities like transit, housing, res-

taurants and retail.”

The office availability rate in

Village Center Station is 14 per-

cent, thanks to companies such as

CoBank, Charter

Communications,

CSG and Fidel-

ity, which have

been attracted to

its urb-suburban

vibe. Suffice it to

say, Village Cen-

ter Station office

buildings also

have fetched the

highest historic

investment sales

prices in SES. For

example, Shea

Properties will sell Charter Plaza

to KBS for approximately $395 per

square foot when construction is

completed in first-quarter 2018.

Furthermore, there are limited sites

for future office development in

Village Center Station, so rents will

continue to rise beyond $30 gross

per sf there, while the rest of the

SES submarket remains stagnant.

North and south of Village Center

Station – the lobes of the dumb-

bell curve – are not urb-suburban

destinations. Instead of embracing

rising rents, these owners are con-

ceding to abated rent, expensive

work letters, rent credits and bonus

commissions. What a difference an

intersection or two can make!

In the North Denver Tech Center

(Belleview Avenue and I-25), where

the average rent is $25 gross per sf,

owners have engaged in an ameni-

ties war to address the preferences

of today’s tenants. Time will tell if

it is enough to add a fitness center,

conferencing facilities, food-truck

spaces, outdoor seating and a con-

cierge to attract new tenants.

Further south in Meridian (Lincoln

Avenue and I-25), corporate cam-

puses of the 1990s – like those of

Teletech, Western Union and Starz

– are coming to market in droves at

a time when pastoral settings must

compete with rousing live-work-

play options.

Few owners have beaten the odds

at a “lobe” location. For instance,

Denver Corporate Centers II and

III have experienced record leas-

ing activity this year in the North

Denver Tech Center. DPC Develop-

ment Co. with Bridge Investment

Group Partners bought these two

buildings for a low basis of $109 per

sf in March 2016. After much col-

laboration between the ownership

partners, property management,

JLL brokers and Gensler architects,

a $3.5 million renovation was

executed with no detail spared.

Instead of just meeting the ameni-

ties war, the joint decisions/design

went above and beyond to include

a group fitness room and a tenant

game lounge. Most importantly,

another $4.5 million was invested

in an aggressive spec suite program,

focused on delivering 4,000- to

6,000-sf turnkey spaces. Ownership

met the market demand by inking

deals at $25 gross per sf, scooping

up virtually every tenant within a

4-mile radius. To enhance urb-sub-

urban appeal, some retail develop-

ment is being added to the site in

2018.

Delivering a good value propo-

sition in a submarket with high

availability creates a magnet effect

– every tenant wants to be in the

building. If the same matrix is

applied in a tight submarket, such

as Village Center Station, owners

will achieve higher rents. Case in

point: Keep an eye out for the com-

ing transformation of Tuscany at

Village Center in 2018 by Crescent

Real Estate Partners and OZ Archi-

tecture.

On a final note, traffic congestion

is beginning to push some tenants

into “lobe” locations in SES. The

inverse of urban migration is lead-

ing to satellite offices in SES. The

next time you are stuck in traffic

on I-25, consider commuting via

the light rail to an urb-suburban

location or settling for an economic

office deal closer to home.

s

The law of urb-suburban office location attractionMarket Update

Whitney Hake

Director, Cushman

& Wakefield,

Denver

Cushman & Wakefield

An aerial of the southeast suburban

dumbbell curve, with the flat part cen-

tered around Village Center Station.