4 / 32

4 / 32

Page 4

— Office Properties Quarterly — September 2017

www.crej.comMarket Update

ROBERT WHITTELSEY | KATY SHEEHY

COLLIERS INTERNATIONAL

4643 S. Ulster Street | Suite 1000 | Denver, CO 80237

+1 303 745 5800

| www.colliers.com/denver

IMPRESSIVE FULL BUILDING REMODEL RECENTLY COMPLETED

Suites Available From 3,000 SF to 56,000 SF

6200 S. Syracuse Way | Greenwood Village, CO 80111

CARRARA PLACE

New State-of-the-Art

Fitness Center

New Conference

Center

Updated Café &

Outdoor Areas

Unrivaled Move-In

Ready Suites

Transformed

Multi-Purpose Lobby

Walking Distance to

the Light Rail

OWNED & OPERATED BY:

A

s the current economic

expansion continues, people

start to question where we

are in the business cycle.

The “official” declaration of

U.S. expansions and contractions

comes from the National Bureau of

Economic Research. As of August,

the current economic expansion

has been underway for 98 months,

which currently ranks as the third-

longest expansion since tracking

began in 1854. Where we are in the

business cycle is an important con-

sideration for most companies as

they plan and budget for changing

sales and staffing expectations.

While national business cycles

are tracked using measures such as

gross domestic product, personal

income, industrial production and

employment, these measures may

not be available at the state level or

are released with such a lag as to

not be useful. Therefore, employ-

ment statistics, which are released

on a monthly basis, are closely

watched at the state and local lev-

els as the key indicator of an area’s

economic health.

After ranking fifth for employ-

ment growth in 2015 and 13th in

2016, Colorado ranked 11th for

employment growth as of mid-2017.

Nevada and Utah currently hold the

top spots in the country with a 3.3

percent increase in employment.

Colorado employment growth is

expected to average 2.1 percent in

2017, representing the addition of

about 55,000 jobs.

Six of the seven metropolitan

statistical areas in Colorado posted

increased employment from the

first half of 2016 to the first half

of 2017. The

lone exception

was the Grand

Junction MSA,

where employ-

ment declined

0.4 percent. The

Fort Collins MSA

grew the fastest

in 2015 and 2016,

and that trend

continued into the

first half of 2017

as the region’s

employment base

increased 4.3

percent. The big-

gest shift in posi-

tion was in the Greeley MSA. After

employment decreased by 1.3 per-

cent in 2016, primarily due to the

decline in oil and gas, employment

expanded by 2.6 percent in the first

half of 2017, ranking the Greeley

MSA as the second-fastest growing

MSA in Colorado.

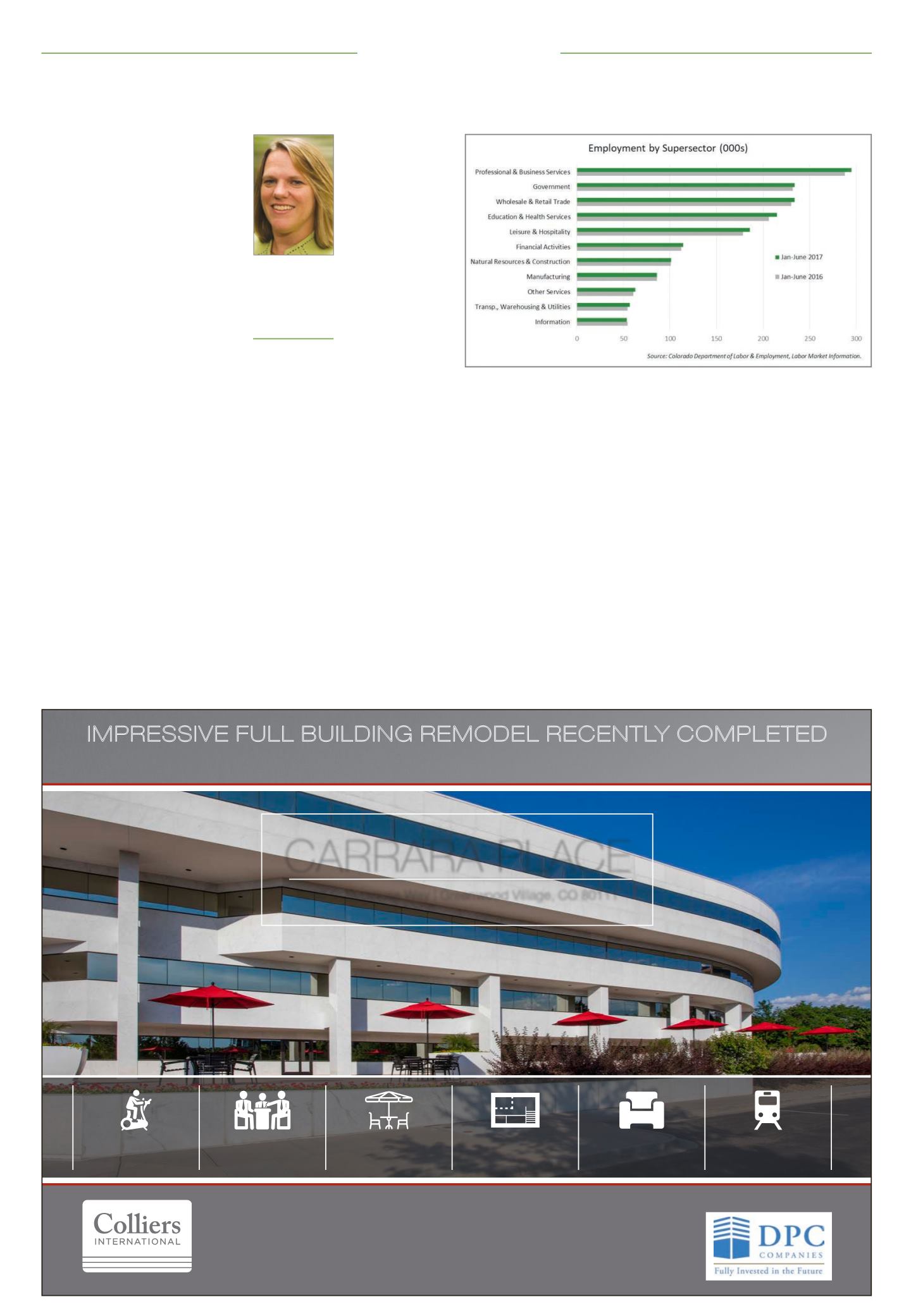

Nearly 1.7 million jobs are located

in metro Denver, defined as the

Denver MSA plus the Boulder MSA.

Dividing the employment base into

11 supersectors reveals that nine

of the categories in metro Denver

increased through the first half of

the year, with the exceptions of the

information and manufacturing

supersectors. The education and

health services supersector report-

ed the largest percentage increase

in employment and added the most

new jobs, averaging a 4.1 percent

increase in employment in the first

six months of the year, or the addi-

tion of 8,500 jobs. The professional

and business services supersector

is the largest of the 11 supersectors

and added 7,200 jobs over the peri-

od. The natural resources supersec-

tor recorded the smallest increase

in employment over the year, rising

0.5 percent with the addition of 500

jobs.

Looking ahead, the Manpower

Employment Outlook Survey

expects that the percentage of com-

panies hiring in the Denver MSA

will increase 3 percentage points

between the second and third quar-

ters, with 30 percent of companies

planning to expand their employ-

ment levels. By comparison, only

about 24 percent of U.S. companies

expect to add workers in the third

quarter.

According to the survey, job pros-

pects are positive in most sectors of

the economy, including transporta-

tion and utilities, wholesale and

retail trade, information, financial

activities, professional and business

services, education and health ser-

vices, leisure and hospitality, other

services, and government. Hiring in

construction and manufacturing is

expected to remain unchanged.

Employment in metro Denver is

forecasted to increase by 2.3 percent

in 2017, representing the addition of

about 37,000 jobs. The employment

growth rate in metro Denver in 2018

is likely to fall slightly as compa-

nies continue to struggle to find the

workers needed as the region posts

an average annual unemployment

rate in the 2.5 to 3 percent range.

• What does this mean for commer-

cial real estate?

A simplistic analysis

of employment by supersector high-

lights expected changes in office,

industrial and retail uses.

Supersectors dominated by office

users include professional and busi-

Employment stats help paint picture of our economyPatricia

Silverstein

President and

chief economist,

Development

Research Partners,

Littleton

Please see ‘Silverstein’ Page 27