14 / 32

14 / 32

Page 14

— Office Properties Quarterly — September 2017

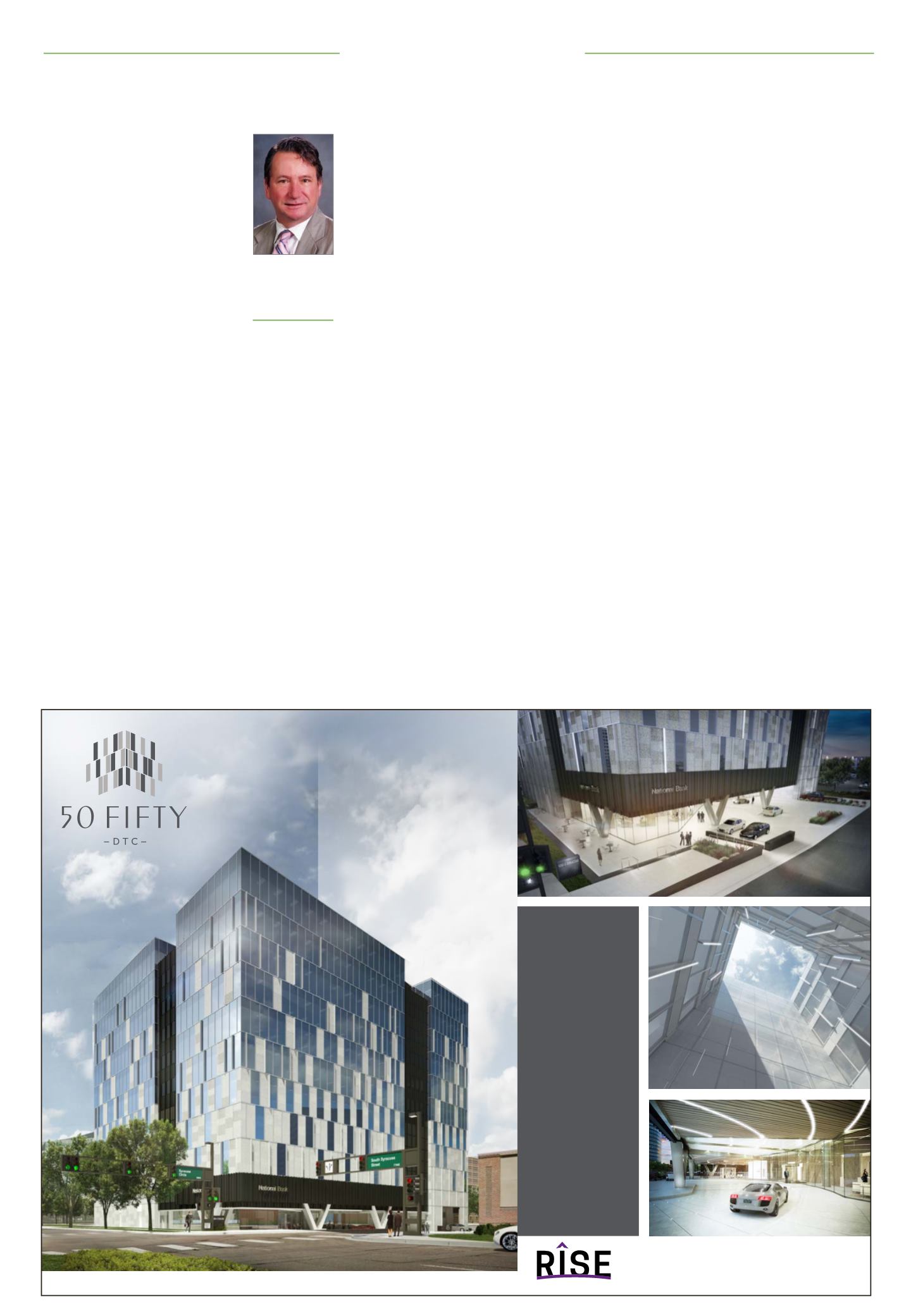

www.crej.comWelcome to 50 FIFTY DTC...

The most elegant and sophisticated

achievement in architecture The DTC

has ever seen.

Make no mistake:

This isn’t just

another office building. It’s a Class

AAA, 12-story office tower like

no other with beautiful lines and

amazing features. A visually stunning

mix of inspired design coupled with

the finest building materials and

technology available.

DETAILS

• Class AAA Office

Tower

• 12 Stories

: 6 stories of

office over 8 stories of

parking

• 185,000 SF

• 30,500 SF

column-free

floor plates

• Mountain views from

every floor!

• 100% covered, secured

parking below building

footprint at

3.5 spaces

per 1,000 SF

• Fitness Center

• Common Conference

Room

• Collaborative Lounge

and Work Space Areas

• Bicycle Storage

• Delivery Summer of

2018

For leasing

information

contact:

BILL WOODWARD

|

720.274.8313

bwoodward@RISEcrea.comRANDY SWEARINGEN

|

303.521.7354

rswearingen@RISEcrea.com5 0 5 0 S OU T H S Y R A CU S E S T R E E T

|

D E NV E R , CO 8 0 2 3 7 |

WWW. 5 0 F I F T Y D T C . COMCommercialRealEstateAdvisors

Investment Market

U

ser-investor office acquisi-

tions are an increasingly

attractive option for a user

who is willing to become a

landlord and is looking to

enjoy the benefits of owning the

building he occupies as well as the

enjoyment of low-subsidized occu-

pancy cost from other tenant’s cash-

flow. As we witness a general increase

in the sophistication of investments

– and in real estate investment world,

in particular – and a new entrepre-

neurial momentum in the economy,

it only makes sense for business

owners to buy user buildings and, by

extension, user buildings with addi-

tional cash flow. There are negative

trade-offs for this strategy and it’s not

for everyone, but we’re seeing unprec-

edented interest in entrepreneurial

business owners diversifying into real

estate investing via the user-investor

office purchase.

Businesses big and small customar-

ily lease their real estate and focus

their capital on the business. The

general thought is to let the landlord

handle the real estate tasks, while the

entrepreneur can focus on her area

of business expertise: growing the

company.

It also is relatively customary for a

business to deploy its capital in the

ownership of the building it solely

occupies and handle real estate tasks

like maintenance and bills them-

selves. These businesspeople now

have two foci: their business as well

as managing and maintaining their

building.

What’s changing is that increas-

ingly business users are deploying

their capital in their business as well

as their building, but offsetting the

building expense

with income from

other tenants. This

dynamic of addi-

tional building ten-

ants requires the

owner to become

landlord in addi-

tion to all the tasks

associated with

investment owner-

ship. As business-

people become

more sophisticated

in investing in real

estate (owning the

buildings they occupy), it only makes

sense that, by extension, these busi-

ness folks would evolve into the

user-investor role – a businessperson

who owns the building she occupies,

with cash flow from other tenants in

a multitenant building. This isn’t a

brand new phenomenon but, I sub-

mit, it now is a more popular invest-

ment vehicle as entrepreneurs get

more sophisticated and more com-

fortable with real estate as a cash-

flowing investment.

As I alluded to above, this user-

investor role isn’t for everyone.

The user-investor must wear three

hats. An entrepreneur running her

core business, a property manager

maintaining the building, and an

asset manager/landlord in charge of

collecting rents, keeping books and

holding tenants’ hands. This presents

an opportunity for said user-investor

to become a jack of all trades and

master of none.

Still, many companies are deploying

this strategy as a diversification tool,

a way to offset occupancy cost and as

a strategy to acquire distressed real

estate at well-below replacement cost

with the utility only the user-investor

can enjoy.

One user-investor strategy is for a

company to build a new building that

is oversized and lease out the excess

space to offset occupancy cost. New

office construction costs are high, so

the excess space would necessitate

strong rental rates to maintain the

replacement value of the building. For

anything but the most high-end (e.g.,

medical) occupancies, it’s difficult for

this strategy to succeed for the user-

investor.

Another more common and more

successful strategy is for a buyer to

buy an unstabilized building with

some vacancy for well-below replace-

ment cost and occupy the vacant

suite.

Our team has sold eight user-inves-

tor office buildings in the last couple

years, and we’ve seen some trends

and benefits for sellers and user-

investors.

For example, a seller may have a

destabilized investment property

that’s 75 percent full and a 4.5 percent

cap on current net-operating income,

and the seller would like to sell it at

a pro-forma 8 percent cap. The pure

investment buyer sees this opportu-

nity and thinks the seller is keeping

upside to himself, and so it sits.

Would a user-investor pay above

what the property is worth to a pure

investor? I submit that it’s of value

for the user-investor to do so, because

he would benefit from the utility of

having space to occupy as well as the

benefit from additional income from

the other tenants to offset the occu-

pancy costs.

The liquidity offered by the user-

investor benefits the seller as well

by making a market for unstabilized

buildings that can’t be filled by value-

add investors alone. This new liquid-

ity also is beneficial for the commer-

cial real estate market as a whole.

These buildings generally sell for

below replacement cost and provide

an opportunity for business owners

to diversify their holdings. Further,

the new owner can monetize her

position by selling and leasing back,

which is a whole other topic.

There are distinct advantages for

the user-investor from a management

perspective as well. The owner is on

site so he can respond quickly to real

estate issues. It’s interesting to note

that of the eight recent user-investor

transactions we’ve been involved

with, none of the buyers hired a

third-party property manager. Some

of these buyers are new to real estate

management. I submit that the prox-

imity of the owner to the building

helps with management challenges,

which is another advantage in lower-

ing costs for the user-investor.

User-investor office acquisitions

are a great opportunity for a user to

become a landlord by owning the

building he occupies, enjoying low

subsidized occupancy cost from other

tenants’ cashflow and deploying the

benefits of investment real estate

ownership. It makes sense for busi-

ness owners to buy user buildings

with additional cash flow at below

replacement costs, and it benefits

sellers and the commercial real

estate market. We welcome this

nascent form of real estate owner-

ship and the new energy these non-

typical real estate buyers bring to

the table.

s

The user-investor office strategy rises in popularityJohn Becker

Senior vice

president, Fuller

Real Estate,

Greenwood Village