30 / 32

30 / 32

Page 30

— Office Properties Quarterly — September 2017

www.crej.comcontrols. Improvements like this are

never cheap and can put a significant

dent in discretionary budgets, which

might have otherwise been allocated

for public area design and furniture,

for example.

Again, new building owners don’t

have to contend with any compliance

surprises. Every code requirement

is already accounted for and every

building amenity has already been

designed, approved and constructed

with state-of-the-art methods and

materials.

The good news for those 1980s era

building owners is that occupancy

still boils down to what tenants

want, and tenants still want value. Of

course, it is the millennials who drive

the market and ultimately define

what value is.

“Those employees dictate not only

tenant design, but building retrofits

as well,” Revious said. “Tenant spaces

are going to continue to evolve, and

owners of older product are respond-

ing by bringing the sizzle, the cool.

That’s the necessity of the market.”

In fact, push back on the open-plan

office is fueling some of that sizzle.

C-suite players have been increas-

ingly vocal about the disruptive

nature of the open office, but many

employees who once may have laud-

ed the wide-open egalitarian work

style now are starving for privacy

wherever they can find it.

In a piece about office design strat-

egies published last month in Fast

Company’s Co. Design digital maga-

zine, one quoted architect put it this

way: “When [I] asked where a young

client goes for privacy, the response

was ‘Starbucks,’ which is not unique.”

The “not unique” part of that state-

ment is what speaks volumes. Com-

panies that are slow to address these

pervasive facility issues are paying a

price in lost employee productivity

and morale. On the other hand, 1980s

building landlords and their savvy

property managers are profiting from

these tenant-based design deficien-

cies by upgrading and repurposing

building common areas.

Both open and enclosed private

breakout spaces in or near lobbies, for

example, can offer building tenants a

privacy amenity that may have been

lacking or absent in their own offices.

Even fussy millennials may opt out of

Starbucks if given the option to stay

in their own office building and com-

plete the tasks that they previously

may have deemed impossible.

Of course, no two buildings are

alike, and property managers must

sell the individual benefits of those

renovations aggressively and consis-

tently. And intangibles do matter.

“It’s not always about the numbers,”

Kaboth maintains of the metro area’s

aging office inventory. “You can take

these ’80s buildings and create a

similar environment to new product

with the right renovations at the right

time. The bones are there. And every

building has its own personality.”

s

Brunner

Continued from Page 20ing, there are challenges to a robust

economy. For both landlords and ten-

ants, construction costs for tenant

improvements have raised dramati-

cally.This is partially due to a shortage

of construction labor, which has led to

fewer and higher bids across the board.

In a down market, landlords typically

had to provide turnkey tenant improve-

ment packages to compete for tenants.

Landlords are more bullish and tenants,

in turn, often contribute to their own

improvements. Alternatively, tenants

are signing longer-term leases with

higher tenant improvement allowances

or amortizing the cost of the improve-

ments into the lease rates.

There are challenges on the sales

side for office product as well.Valuing

properties can be challenging, primarily

with regard to properties sold to owner

occupants. As demand for owner-occu-

pied office properties has increased,

property values have gone up.The gap

between buyers and sellers seems to

be widening, and I have experienced

several instances where appraisals have

come in low because the pricing con-

tinues to rise, in some cases faster than

the market can keep up. It is important

to work with an experienced real estate

professional who can convey to the

seller and buyer the true value of the

property.

Is change on the horizon?The answer

is yes, but probably not dramatic change

thanks to our diverse economy. Rent

growth has slowed down to approxi-

mately half of what it was last year.The

supply is beginning to catch up with the

demand.The office market will contin-

ue to be a vibrant market but perhaps

at a slower pace than we have seen

over the last few years. Now is the time

to plan, prepare and execute to get the

most out of a strong office market.

s

Shaw

Continued from Page 21Denver Office of Economic Development

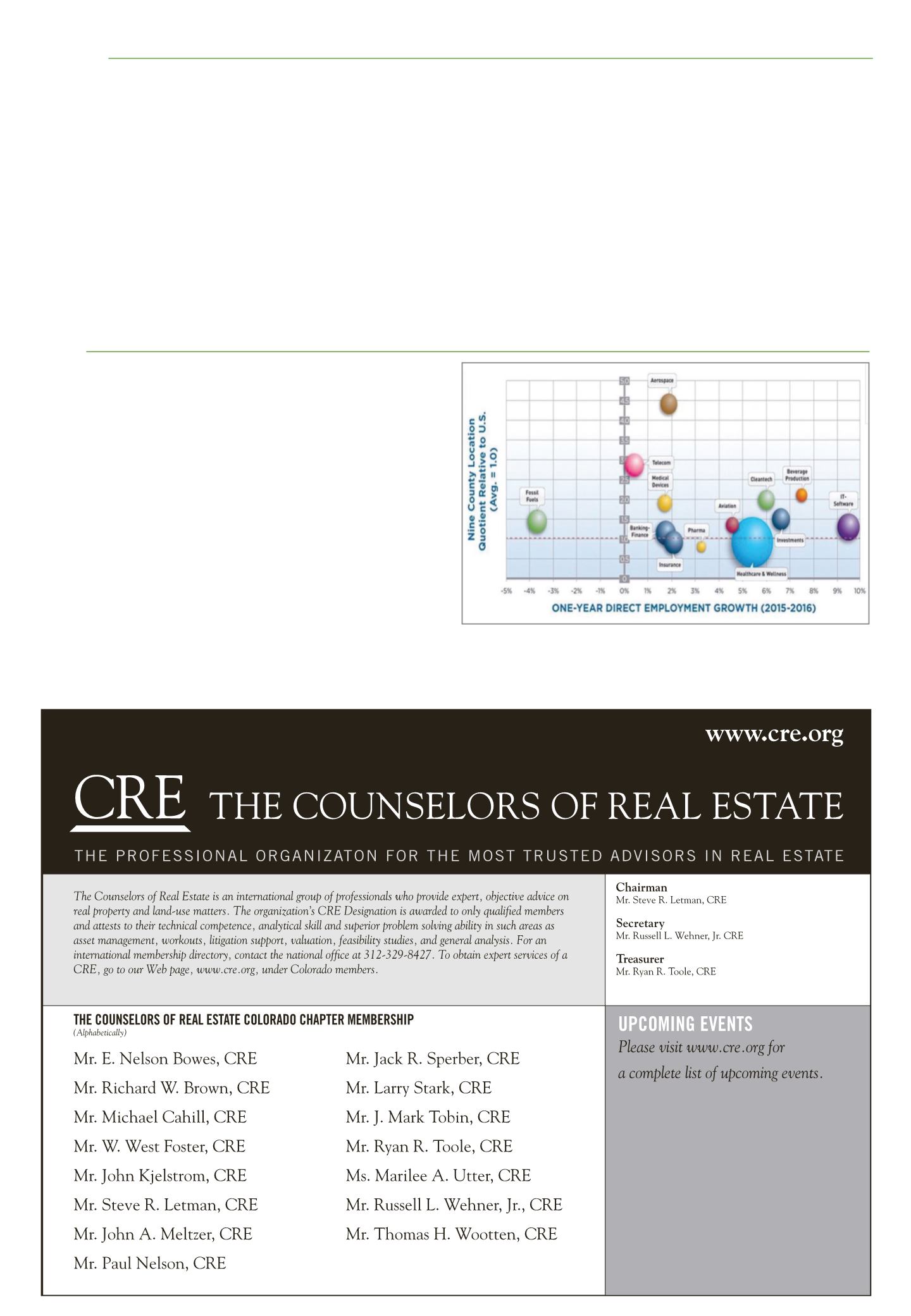

Denver metro industry growth: Increased professional and industrial diversification has allowed

the office market to withstand market challenges.