27 / 32

27 / 32

December 2016 — Office Properties Quarterly —

Page 27

generously donated by

S U P P O R T YO U R C O L O R A D O S YM P H O N Y !

DECEMBER 31, 2016 8:00 PM

*See all rules and regulations at

coloradosymphony.org/raffle.Raffle License No: 2016-09939 Raffle ticket is not tax deductible. Fundraiser for the Colorado Symphony

Association. Presence not required to win.Winner of all prizes subject to taxes, including federal, state, and local income taxes.

Thank you for your support

at A Night in Vienna

Boettcher Concert Hall • Denver Performing Arts Complex

1000 14th St. No. 15 Denver, CO 80202

Presence not required to win

Market Update

invest more money into the space

because he already is trying to miti-

gate a losing situation, Holm said.

“Finding a user who can use the

space the way it is can be hard,” said

Holm. “If you have a tech firm and

you’re subleasing oil and gas space,

which is all hard offices, that’s a mis-

match – it doesn’t really work.”

Aside from the floor-plan configu-

ration, the type of building itself can

present challenges. The majority of

these spaces are found in traditional

1970s and 1980s vintage buildings

that may not be appealing to every

company, Davidson said.

Tenant improvement allowances

from sublandlords can help get deals

done as can in-building amenities,

said Davidson. And the location is

critical.

If you’re a company subleasing

5,000 to 10,000 sf of open-planned,

brick-and-timber space in Lower

Downtown, your space will probably

be picked up quickly and at rates

north of $30 a sf because options are

extremely limited, Davidson said.

However, if it’s a larger space that’s

office intensive, located in the down-

town core, even at a price of $15 a sf,

that space could sit vacant for a year

or two, Davidson said.

The second common mismatch is

in term requirements – i.e., a sub-

lease space has three to four years

left on the term, but the interested

subleasee only needs it for a year and

a half. Some of these deals get done,

but it’s challenging, Holm said.

With these two hurdles in mind,

the ideal tenant must be a company

that has a short-term need and

can make the existing configura-

tion work, such as a company that

is moving to the market or needs to

expand quickly, said Holm. For these

reasons, it isn’t surprising that much

of the available sublease oil and gas

space hasn’t subleased.

“Some of these sublease spaces,

these bigger blocks, have been sit-

ting for a while,” said Lee. “But that’s

going to change in 2017 for the fol-

lowing reasons: we’ve bottomed on

oil and gas, where the price is right

now; most of the space that’s coming

back to the market has come back in

2015 and 2016 – that doesn’t mean

that there couldn’t be some more iso-

lated situations – but most of the oil

and gas space that’s going to hit the

market has; and I predict that by the

end of 2017, the amount of sublease

space downtown will be cut in half.”

Additionally, relief will be aided by

the fact that 1801 California is now 95

percent leased, which had been the

gorilla of the downtown market for

the last five years because it always

had available space, he said. Many

of the new builds are leasing up, and

demand to be located downtown

and the allure of downtown’s ameni-

ties have never been stronger. This

means that for tech or other growth-

oriented tenants, there will be fewer

options, he said.

“Who are the next tech tenants

that need 30,000, 40,000, 50,000

or 60,000 square feet?” Lee asked.

“Where do they go? I think they go

where there’s value.”They’ll also be

attracted to the flexibility and shorter

lease term options. “The relief will be

coming, for the most part, from val-

ue-oriented tenants who can’t find

growth in new product.”

Holms disagrees about immedi-

ate relief coming in 2017. “I think it

just takes time to work the sublease

space down; you’ve got to go through

the transition,” he said.

He anticipates oil and gas firms

are likely to remain static through

the foreseeable future and wonders

where we are in the overall busi-

ness cycle, which has been enjoying

expansion for about seven years. If

something happens in the economy,

the sublease space could get worse,

not better, he said.

“I’m not saying that’s going to

happen – it’s just a question, and

I’m pretty sure I’m not the only one

thinking about it because of where

we are in the cycle,” he said. The

impact coming from the unpredict-

able political situation also adds to

the unknowns.

“So no, I don’t really see anything

on the horizon that’s going to all of a

sudden fix the sublease situation,” he

said. “It’s just going to have to work

itself out over time and we all have

to cross our fingers that something

doesn’t happen in the economy that

actually makes it worse.”

s

CBRE

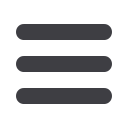

Oil and gas firms make up disproportional share of downtown’s sublease space.