26 / 32

26 / 32

Page 26

— Office Properties Quarterly — December 2016

Market Update

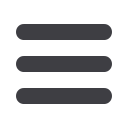

1.4 million and 1 million available

in these markets, respectively, that’s

the equivalent of 2.6 percent and 1.5

percent of the total respective space.

“So it’s material, but it’s not earth

shaking,” he said.

Another important key to under-

standing the current sublease market

is identifying the main industry – oil

and gas companies – subleasing space

downtown. Unlike the previous oil

bust of the 1980s, downtown Denver

now enjoys a diversified business

market, with oil and gas accounting

for about 20 percent of downtown

office market tenants. However, due

to the drop in oil prices, these tenants

now make up about 60 percent of the

available sublease space in the down-

town market, totaling almost 900,000

sf of available space, said Holm.

Further, of that sublease space, oil

and gas firms make up four of the top

five largest blocks of available space,

which equals 52 percent of the entire

sublease space available, said David-

son.

Of these four major sublease spaces

– two are 100,000 sf, one is 230,000 sf

and the last is 50,000 sf – all but one

have four to five years remaining on

their leases.

“The largest sublessors downtown,

representing 60 percent of the oil

and gas sublease space, are all credit

users, so these are not people who are

going to default,” Holm said. “They’re

going to continue to pay the rent and

landlords will continue to collect, and

while those companies may sublease

their space at a discount, the over-

all impact on the market is muted

because they’re not a risk of default.”

The SES market’s sublease space

is spread across industries, which

appear to result from a combination

of factors without anything in particu-

lar leading the way, Holm said.

Potential Relief

There has been some activity

backfilling this sublease space by a

few oil and gas firms that are taking

advantage of the current market and

expanding. Law firms and profes-

sional services also are a natural fit

for the space configuration, but it’s

hard to point to one specific industry

that is gobbling up the spaces.

Thanks to Denver’s diverse econo-

my, there’s a variety of potential ten-

ants, ranging from tech to health care

to finance and advertising to food

services, that could be interested,

said Lee.

“This is the best-valued space in

downtown, because you’re going to

be in the $45- to $50-per-sf range on

space in Central Platte Valley or LoDo

for new construction,” Lee said. “This

space can come in at 50 to 60 percent

of that cost, so it’s really where the

value is. The question is, is the fit

appropriate?”

There are two major challenges

when filling sublease space: configu-

ration mismatches and timeline mis-

matches.

A user must be willing to use the

space in its existing configuration.

The sublessor does not want to

Continued from Page 1