8 / 32

8 / 32

Page 8

— Office Properties Quarterly — April 2015

Investment Market

D

enver’s office market and

economy continues to thrive

in 2015. Colorado’s 2014 year-

end unemployment rate was

4 percent. Denver was the

No. 1 city in the nation for millennial

population growth in 2014, and it is

estimated that 22 percent of Denver’s

population is made up of millennials.

Colorado had approximately 1.65

percent population growth in 2014

(fourth in the nation) and is now

ranked the No. 2 city for number of

bachelor degrees per capita. The 2014

year-end job growth was approxi-

mately 60,000 jobs. These dynamics

resulted in Urban Land Institute rank-

ing Denver the No. 4 market for com-

mercial real estate investment in 2015,

and Business Insider Magazine ranks

Denver as the most comprehensive

city for economic growth.

Denver’s office investment market

started rebounding in 2010. Some

of the investors that were willing

to make acquisitions early in the

recovery are now harvesting profits.

Two examples of this are The Triad

at Orchard Station and Offices at The

Promenade.

M&J Wilkow purchasedThe Triad in

2012 for $63 per square foot at 72 per-

cent occupancy. The asset was retrofit-

ted and rebranded by the ownership

over a two-year period. At the time of

purchase, market rents were $16-$17

per sf; today they are $21-$22 per sf

gross. The Triad is back on the market

for sale and will prove to be a case

study on market timing and value

enhancement execution.

There are currently several office

listings that were purchased between

2006 and 2008, and the holding peri-

ods were extended due to the Great

Recession. Denver

weathered the

downturn better

than most mar-

kets. Numerous

office owners were

successful in hold-

ing through the

recession, and they

can now exit with

upper-teen returns.

Occupancies are

nearing 90 percent,

and rents are at lev-

els exceeding past

cycles.

Upside potential

today in Denver is rolling existing

leases to market in an improving

rental market. It’s typical today to see

rents in place at $3-$5 per sf below

current market rents in the primary

suburban markets. Core-plus capital is

aggressively pursuing assets in Denver,

and they target 60 percent roll or more

in the first three years of the holding

period.

Cap rates continue to compress as

new capital pursues Denver office list-

ings. There were 18 office trades above

$15 million in fourth-quarter 2014; 11

of them sold to new investors to Den-

ver. The capital pool spans from New

York to California domestically, and

Canadian capital is the most active

foreign capital. Cap rates continue

to compress as the depth of buyers

increases. The 10-year bond has been

below 2.25 percent since the end of

November. At the time of this article,

the 10-year is at 1.94 percent; it was as

low as 1.67 percent on Feb. 2 (volatile).

This has resulted in interest rates for

long-term debt being plus or minus 4

percent.

Most conduits and

life companies are

offering between

two and 10 years of

interest-only rates,

depending on the

loan to values and

the creditworthiness

of the borrower.

Bank or fund bridge

debt can be in the

mid-3 percent.

Hence, a 6 percent

cap results in a posi-

tive leverage return

of 10 percent during the interest-only

period. Commercial real estate is the

preferred investment vehicle as the

risk and reward can provide higher

returns than alternative investments.

Denver’s most preferred core and

core-plus markets are the infill loca-

tions of Lower Downtown, Cherry

Creek and Boulder. There is about 1.25

million sf of new construction under-

way in LoDo and the west central

business district. LoDo has a vacancy

rate under 4 percent, and leases that

were signed in 2008-2009 can be $7-$8

per sf below market today. Cap rates

can be in the upper-4 percent for tro-

phy assets constructed during the last

cycle to mid-5 percent for redeveloped

historic brick and timber properties.

Prices per sf can range from $300 per

sf for core-plus properties to mid- or

upper-$500 per sf for trophy and core

opportunities in LoDo.

Cherry Creek is transforming from

a dominant retail destination to a

live, work, play environment. Cherry

Creek is becoming a LoDo/millennial

environment that caters to adults with

some of the highest incomes in Den-

ver. Due to the recent zoning change,

there are two office assets, two mul-

tifamily properties and a hotel under

construction. Leasing activity is strong

and rents for new office product are

in the mid-$30s per sf triple net. First

Avenue Plaza (55 Madison and 44

Cook) recently traded for $285 per sf

and under a 5 percent cap rate.

Boulder is in the midst of a transfor-

mation due to a significant amount of

value-add capital being infused into

the market over the past three years.

Unico and Goff Capital Partners both

made significant investments into

portfolios of older assets in Boulder’s

core and eastern markets.With the

repositioning of these properties, Boul-

der became even more attractive to

technology and biotech companies.

Office rents are increasing significant-

ly, and the downtown core of Boulder

can be in excess of $40 per sf triple

net.

Due to the lack of opportunities

in Denver’s CBD and the low yields

of assets in LoDo, investors are fully

engaged in pursing core and core-plus

listings in the southeast suburban

market. Twelve office sales occurred

in the fourth quarter above $15 mil-

lion. Prices ranged from $66 per sf for

a vacant call center facility to $210 per

sf for a core-plus Class A multitenant

building.

Overall, Denver continues to be one

of the most preferred locations in the

nation for office investment capital.

Transaction flow continues to increase

as new domestic and foreign investors

pursue upside in a rising rental rate

environment. The Denver office mar-

ket is experiencing benchmark prices

per sf as lease rates exceed peak levels

of previous cycles, and cap rates con-

tinue to be at historical lows.

s

Office investment market continues to thrivePatrick

Devereaux

Executive vice

president, capital

markets, JLL,

Denver

Jason Schmidt

Executive vice

president, capital

markets, JLL, Denver

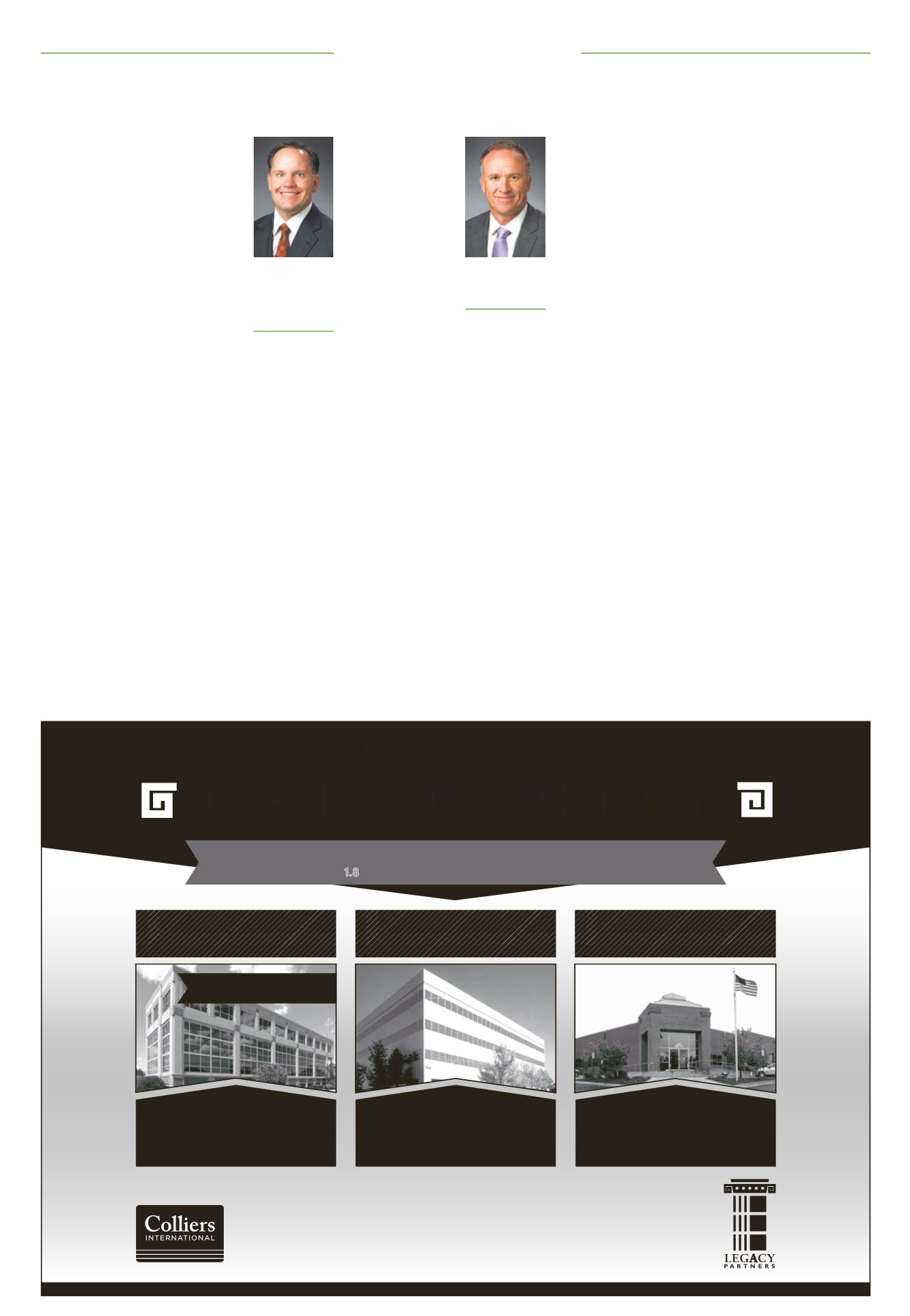

colliers international would like to congratulate

legacy partners

on the

expansion

of their

1.8

m sf

denver area

portfolio

, with these additions:

highland park

9359 E. Nichols Ave.

Englewood, CO 80112

greenwood plaza

5350 S. Roslyn St.

Greenwood Village, CO 80111

400

inverness pky.

Englewood, CO 80112

72,610 SF

100% LEASED

63,488 SF

100% LEASED

111,482 SF

•Outstanding location

•Amazing views

•Upgrades coming soon

The Legacy Continues

EXPANDING

14,235 SF AVAILABLE

$25-$26/SF FULL SERVICE

ROBERT WHITTELSEY

+1 303 283 4581

robert.whittelsey@colliers.comJOHN HUTTO

+1 303 283 4592

john.hutto @colliers.comKATY SHEEHY

+1 303 283 4563

katy.sheehy@colliers.comCOLLIERS INTERNATIONAL I DENVER

·

www.colliers.com/denverFor leasing information on these properties or additional available Legacy properties contact: