4 / 32

4 / 32

Page 4

— Office Properties Quarterly — April 2015

Market Overview

T

he Denver office market

enjoyed a five-year run of

robust expansion from 2010

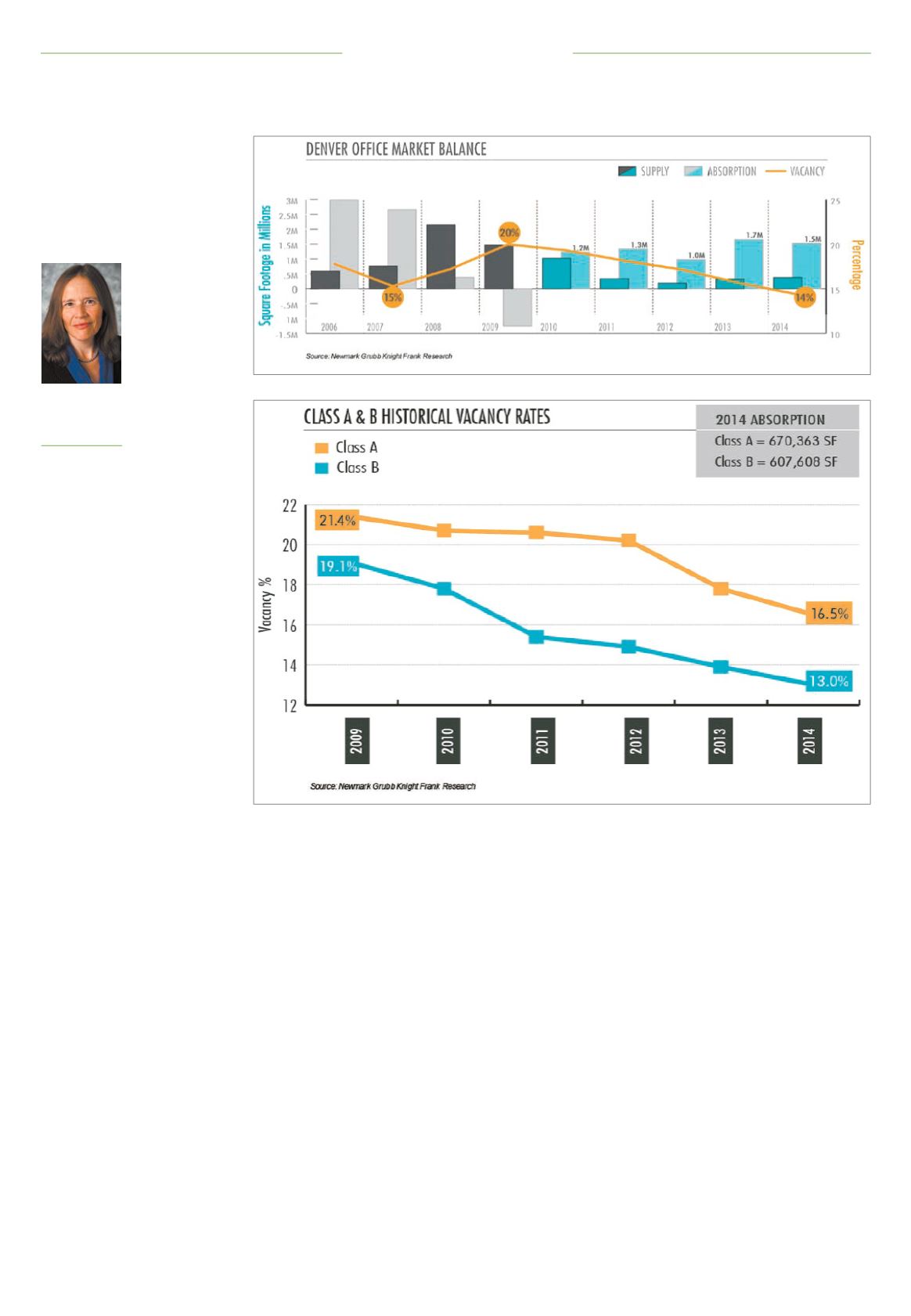

to 2014. Fourth-quarter 2014

vacancy fell to 14.4 percent,

the lowest level since the boom

year of 2000 and a 560-basis-point

decrease from year-end 2009. Quar-

terly absorption stood at 208,682

square feet, bringing the year’s

total to 1.5 mil-

lion sf. From 2010

to 2014, a total of

6.7 million sf were

absorbed.

Submarket high-

lights.

The central

business district

and Northwest

submarkets posted

the strongest

performances

for the year, with

total absorption

of 453,266 sf and

386,255 sf, respec-

tively. Vacancy in the CBD is 12.6

percent, which is down from 13.3

percent in the previous quarter

and down year over year from 13.6

percent. Lower Downtown has the

lowest vacancy rate of the CBD’s

three micromarkets, a drum-tight

7.3 percent.

The NW submarket posted a

strong performance in 2014, driven

by vigorous corporate expansion,

new business lines opened by exist-

ing tenants and tenants new to the

market, culminating in the lowest

vacancy since 2000. Vacancy plum-

meted 481 bps year over year to 14.3

percent.

The southeast suburban submar-

ket ended the year in the red, with

full-year absorption of negative

218,819 sf. This loss, an anomaly,

was due to significant downsiz-

ing by First Data, from 330,000 sf

to 99,000 sf, and the first wave of

migration of Charles Schwab’s 1,900

Denver-based employees to its new

owned campus, which left two

vacant buildings. Although the lat-

ter move was a driver of more than

250,000 sf of negative absorption,

Schwab’s commitment to Denver

promises substantial positive eco-

nomic impact. The financial servic-

es firm plans to add up to 480 high-

paying jobs over the next five years,

and its 47-acre site has the space to

accommodate 4,000 employees.

Class A and B dynamics.

The Den-

ver office market’s Class A and B

office sectors both continued to

improve. As is typical in a recovery

cycle, the Class A sector was the

vanguard as tenants took advantage

of relatively low Class A rates to

upgrade space. After several years

of flight to quality, recovery then

trickled down to the Class B product

due to the widening lease rate delta

and lease up of the desirable Class

A spaces.

Class A vacancy plunged 610 bps

from a cycle high of 19.1 percent

at year-end 2009 to end 2014 at

equilibrium (the point at which

neither landlord nor tenant has

a clear advantage) at 13 percent.

Class B vacancy fell 490 bps during

the same period to 16.5 percent. In

2014, Class A and Class B were neck

and neck in terms of absorption

with both sectors absorbing more

than 600,000 sf.

Rental rates.

Upward pressure on

asking rates continued in the CBD

and NW submarkets. CBD Class

A rates increased 7.9 percent year

over year to $34 per sf, and NW

Class A rates rose 7.5 percent to

$25.54 per sf. These rates represent

historical highs.

Development.

Denver’s strong

economy and market fundamentals

opened a development window: 11

office projects, totaling 2 million sf,

are under construction or renova-

tion. Development is concentrated

in the LoDo micromarket of the

CBD, and the SES and midtown sub-

markets.

Investment.

In 2013, Denver’s office

investment market enjoyed its best

year since 2007 with 11.8 million sf

valued at $2.2 billion trading hands.

In fourth-quarter 2014, sales totaled

5.7 million sf valued at $598.6 mil-

lion, which pushed 2014’s totals

past those of 2013, to 14.3 million sf

valued at $2.3 billion. During 2014,

Denver continued to be a hotbed for

equity placement, with an influx of

new institutional and international

equity to the Denver metro area

driving core pricing.

Of particular note were the sales

of the new Union Station “wing

buildings,” which traded to GLL

Properties, the U.S. subsidiary of

GLL Real Estate Partners Gmbh, for

a record-shattering $600-plus per

sf. Suburban office sales led trans-

action velocity in the latter half of

the year. Spreads between Class A

and Class B rents have become sig-

nificant and will affect investment

patterns in 2015, prompting capital

sources to move down to Class B

product in order to chase yield.

Outlook

Metro Denver has outperformed

the nation in terms of job growth

since February 2010. As of Decem-

ber 2014, job growth increased 3.3

percent year over year, compared

with the U.S. rate of 2.3 percent.

Unemployment stood at 3.9 percent,

almost 2 percentage points lower

than the national rate. Denver’s

record-breaking housing market,

which is ranked sixth in the nation,

is another example of its economic

strength. According to the S&P/

Case-Shiller Home Price Index,

metro Denver home prices rose 7.5

percent year over year in Novem-

ber, the tenth consecutive month in

which prices reached all-time highs.

The future looks bright for Den-

ver’s economy and office market.

The University of Colorado’s Leeds

School of Business forecasts that

Colorado will gain 61,300 jobs in

2015, a level of growth that will

place the state among the top 10 in

the nation for job creation. The pro-

fessional and business services sec-

tor, one of the top office-occupying

industry sectors, is also projected

to grow by a robust 3.3 percent this

year, adding 12,800 jobs.

Denver was ranked fourth among

U.S. markets to watch in 2015 in the

prestigious Emerging Trends in Real

Estate report, which cited its popu-

larity with millennials, concentra-

tion of technology and energy firms,

strong local economy and active

development community.

The stage is set for continued

expansion in 2015. Newmark Grubb

Knight Frank research forecasts this

momentum will continue in 2015

with:

• Positive absorption in most sub-

markets meeting or exceeding 2014

levels;

• Positive absorption returning

to the SES, with space vacated by

Charles Schwab being backfilled;

• Rental rate increases continuing

in the CBD, NW and SES submar-

kets;

• Class A and Class B asking rates

in the CBD, NW and SES continuing

to achieve new highs;

• Strong absorption in the core

CBD, SES and NW submarkets with

continued trickle-down to the mid-

town and southeast submarkets;

• Speculative transit-oriented

development breaking ground in

the SES;

• Increased sales of Class B prod-

uct due to the spread between Class

A and Class B rental rates; and

• Continued job creation and fall-

ing unemployment driving expan-

sion in 2015.

2014 year-end Denver office market overviewLauren Douglas

Research manager,

Newmark Grubb

Knight Frank,

Denver