10 / 32

10 / 32

Page 10

— Office Properties Quarterly — April 2015

Leasing Market

S

outheast suburban Denver is

proving to be a dynamic and

highly sustainable submar-

ket for owners and tenants.

Opportunities abound across

more than 40 million rentable square

feet of office space, with abundant

options for tenants and significant

movement among spaces. And it’s

always easy to find a parking spot.

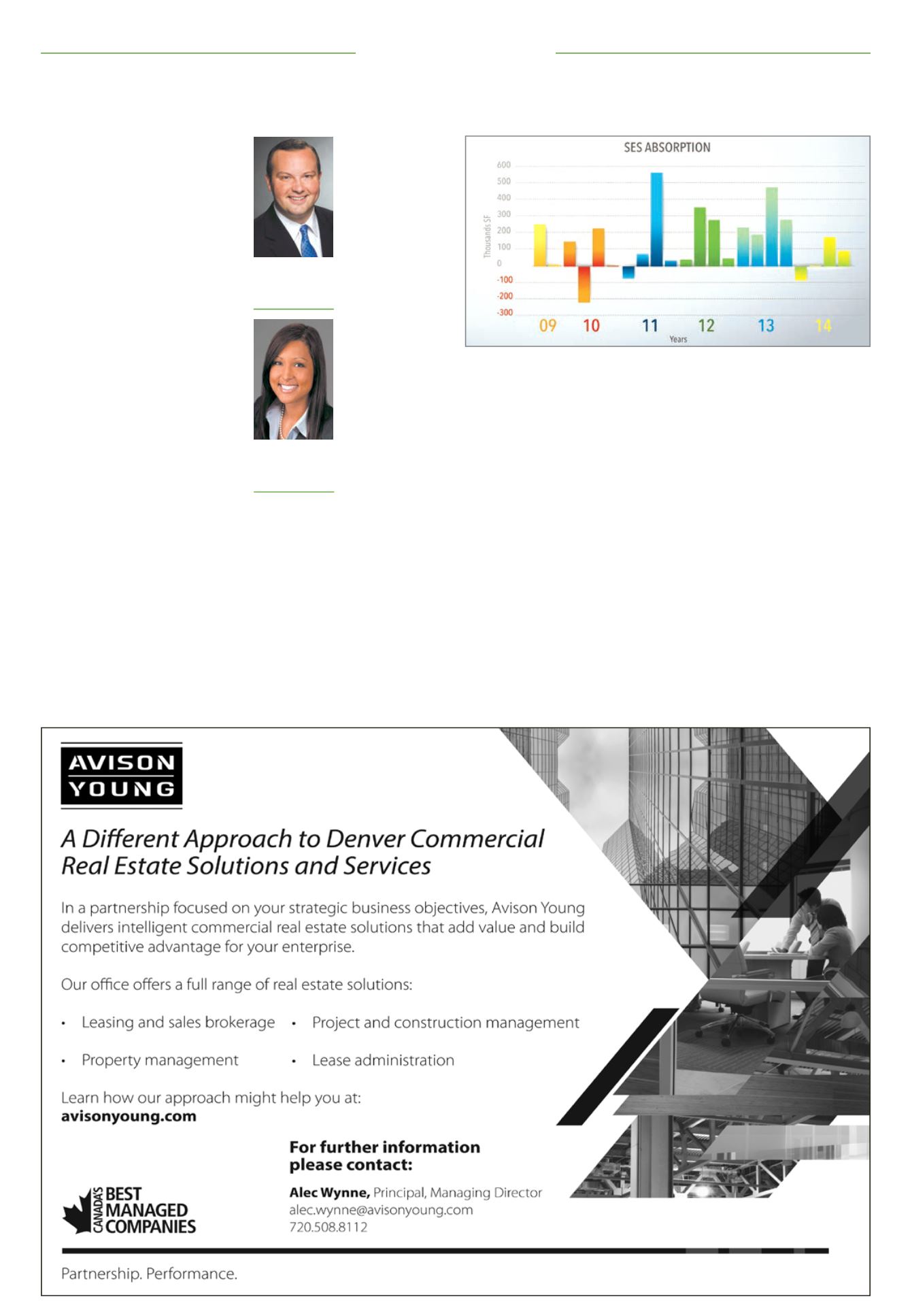

Since recovery from the Great

Recession began in June 2009, 17

of the 22 quarters have seen posi-

tive absorption. In a few cases, ten-

ants have exited the Denver area or

moved to a different submarket, but

what is perceived as a setback for the

landlord community only generates

opportunity for tenants.

Investment activity in SES is fas-

cinating. Transwestern’s Investment

Services Group tracks sales activity,

and watched a compression of capi-

talization rates from 2012 to 2014 of

more than 100 basis points for sta-

bilized Class A product, and over 65

bps for stabilized Class B product. For

this purpose, “stabilized” is defined

as 85 percent occupied or greater. The

practical application of this scenario

for tenants is that the owners’ bases

have risen dramatically, command-

ing higher rent for recently acquired

product.

Class A asking rates climbed an

average of 4.78 percent year over year

since 2010, while Class B asking rates

followed with an average climb of 4.17

percent during the same time period.

Given the customary 50-cents annual

rental bumps, tenants that executed

leases in 2010 will see a disparity of

$2.32 per sf increase (in favor of the

owner) in market asking rates com-

pared with the ending contract rate

for Class A space, and compared with

$1.10 per sf dispar-

ity for Class B space.

Another recent

phenomenon is the

rise in construction

costs since 2012.

Today, $45 per sf is

the new $30, and

$65 per sf is the

new $40. In a build-

out situation, it is

becoming obliga-

tory for owners

to expend greater

amounts of capital,

which either will

affect their margin

or be amortized into

the rental rate. This

rise in construction

cost contributed

to increased rental

rates, and made it

more valuable to

salvage existing

infrastructure when

planning new office

space.

With over 30

large-block tenants

(30,000 rentable sf or greater) current-

ly in the market, representing over 3.4

million rentable sf of space, turnover

is unremitting. This statistic is intrigu-

ing because the large-block tenants in

the market represent approximately

8.5 percent of the overall inventory.

Typical users in the SES submarket

include professional services firms,

communications companies, financial

services firms and engineering firms.

Among the development communi-

ty there is a clear direction for “urban-

ization” of the SES Denver market. For

new developments to be successful,

proximity to light rail and walking-

distance amenities are key. There are

more than 30 proposed office projects

in various development stages across

the SES Denver.

Here is a practical application to

tenants confronting an office-leasing

situation:

Start early.

Time is your friend.

Forward-thinking companies that

want to uncover all opportunities to

drive value from real estate should

approach the market well in advance

of the renewal-option notice date.

Trust your adviser.

Interview multiple

tenant representation specialists to

ensure the right fit for your require-

ments and your business. Cross-

examining multiple groups will give

you access to several perspectives

and ensure you are engaging the best

team to handle your transaction.

Don’t settle for the status quo.

Many

real estate professionals can point to

comps and trends in the market, but

few look for ways to deliver outlier

results that disrupt the norm. Assem-

bling a team of real estate profes-

sionals with diverse skill sets leads to

the best solutions. Every lease is an

opportunity to drive value, not only

economically, but also emotionally

by creating a physical space that will

attract and retain employees.

Understand why.

Building ownership

structures all have different goals

and objectives. Negotiating with a

real estate investment trust, private

owner, institution or foreign entity

presents different challenges that

require insightful audience analysis.

Cover the bases.

Understanding the

basis and financial structure of the

asset in question can pay dividends in

your negotiation strategy. Focusing on

buildings with low amounts of debt

and low bases can add substantial

flexibility to the owner’s abilities.

Recognize the details.

Office leases

are complicated financial instruments

that require acute attention to every

detail. Buildings will trade owners,

but the lease documents will remain

in place, commanding tenants’

outcome.

s

Finding value in vibrant southeast suburban DenverPreston Dunn

Vice president,

Transwestern,

Denver Tech Center

Chaise Schmidt

Associate,

Transwestern,

Denver Tech Center

Southeast suburban absorption rates from 2009 to 2014