5 / 24

5 / 24

April 2015 — Multifamily Properties Quarterly —

Page 5

I

t seems a little hard to imagine

that we could be reading a head-

line like this in the future about

home prices in Denver. However,

if we look back 20 years, we can

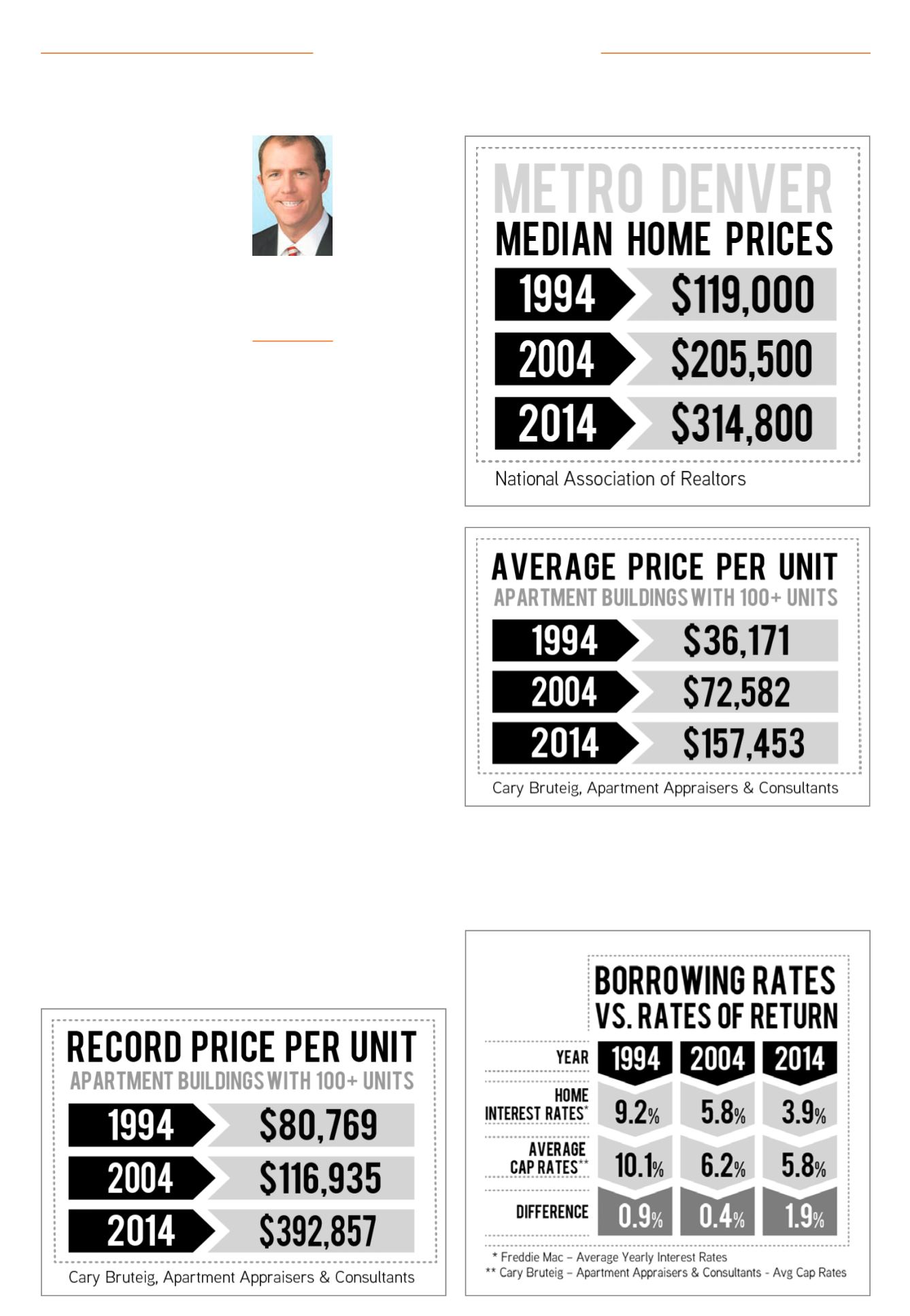

see that median home prices went up

2.65 times from 1994 to 2014. If you

apply this same rate of appreciation to

year-end 2014 median home price, you

could forecast home prices to exceed

$830,000 in 20 years.

As is said, “Past performance is

not an indicator of future outcomes,”

and obviously this methodology is a

bit oversimplified, but it provides an

entertaining way to take a guess at

what the future could hold.

Apartments – A Look Back

When looking at historic average

apartment sales for properties with

100 units or more in those same time

periods, the rate of appreciation is even

more striking with the average price

per unit increasing 4.35 times from

1994 to 2014.

The average price per unit does not

account for the age of the property,

amenities, property upgrades and so

forth.These factors have a bearing on

values, especially if you consider the

record-level pricing achieved by newer

properties with incredible amenities

in core locations. For example, if we

look at record-setting sales in terms

of the highest price per unit each year

for apartments sold with 100 units or

more, we can see the difference – the

record sale price per unit increased by

4.86 times from 1994 to 2014.

If this rate of appreciation were to

occur again over the next 20 years we

could see a record-breaking price per

unit of over $1.9 million! That seems

really hard to envision, but I recall a

conversation with a client back in the

early 2000s. He purchased apartments

in Capitol Hill 10 years prior for $15,000

per unit, and he didn’t think that in his

life they would be worth over $50,000

per unit. This client is still very much

alive today and we have seen proper-

ties similar to his sell for over $125,000

per unit.

Historic Returns

Capitalization rates represent the

rate of return an investor is expect-

ing based on the purchase price. The

percent is derived by dividing net oper-

ating income by the purchase price.

A higher cap rate indicates a higher

rate of return. Further, the greater the

difference between the cap rates and

mortgage rates indicates better invest-

ment returns after debt service. By

looking at the difference between aver-

age cap rates and mortgage interest

rates it would appear that leveraged

buyers have a more

positive spread of

1.9 percent in 2014,

compared with 0.9

percent in 1994.

Recession Proof?

This macro view

of historical values

might belie the

fact that the mar-

ket weathered two

major recessions

in the last 20 years

– first around 2001

with the dot-com

bust, and again

in 2008 with the

financial markets meltdown. It might

also be somewhat misleading to think

that everyone who bought real estate

over the last 20 years made money

(because real estate always goes up in

value, right?). After the fallout from the

recession in 2008 we witnessed several

apartment buildings become lender-

owned from owners who purchased

the properties between 2005-2007.

Interestingly, we recently valued a

property for a lender who foreclosed

during the end of the recession and

has been managing the asset since

that time. At one point the lender was

facing a significant loss. Now, based on

the current restabilized operations, the

property is worth significantly more

than what the previous owner paid for

it in 2007.We tend not to think of real

estate gaining or losing value quickly

but, as recent history shows, it can

happen.

Predictions

We remain very bullish on the near-

term apartment market due the posi-

tive make up of a growing generation

of millennial and empty-nester rent-

ers, lack of for-sale housing options,

strong in-migration to Colorado and a

steadily growing employment market.

However, forecasting what the real

estate market will do in the near

term is always difficult. Will a Euro-

pean debt crisis stymie the market?

Will interest rates increase rapidly?

When will the next “black swan”

event occur? These game-changing

events that tend to send demand

from renters and apartment inves-

tors to the sidelines usually occur

suddenly and without much warn-

ing. Those who can avoid selling into

these markets likely will enjoy the

long-term upside similar to what we

have seen over the last 20 years.

We know that in the current mar-

ket with record-high rents, low bor-

rowing costs and strong investor

demand, it is an excellent time to be

a seller and an owner. Looking into

the past over the long term paints a

pretty good picture of steady overall

apartment appreciation. With our

biased love of Denver and all that

Colorado has to offer, we remain very

positive on this market for the long

term. Here’s to seeing a record price-

per-unit sale in 2034 of $1.9 million!

In the meantime, enjoy these

record rent increases and record prof-

its. And to those waiting to buy in the

next cycle, please let me know when

it will be coming.

s

Median home prices surpass $830,000 in 2034Denver Metro Update

Craig Stack

Vice president,

Colliers

International

Multifamily

Advisory Group,

Denver