10 / 24

10 / 24

Page 10

— Multifamily Properties Quarterly — January 2015

T

he Colorado Real Estate Jour-

nal sat down with real estate

capital veteran Steve Bye

of NorthMarq Capital and

asked him to comment on

the trends in the multifamily lend-

ing arena and his

thoughts about

2015.

CREJ:

How would

you assess the cur-

rent environment

for apartment

financing?

Bye:

To quickly

summarize, bor-

rowers are in the

best of all worlds.

There are no prac-

tical limits on the

availability of capi-

tal from multiple lending sources.

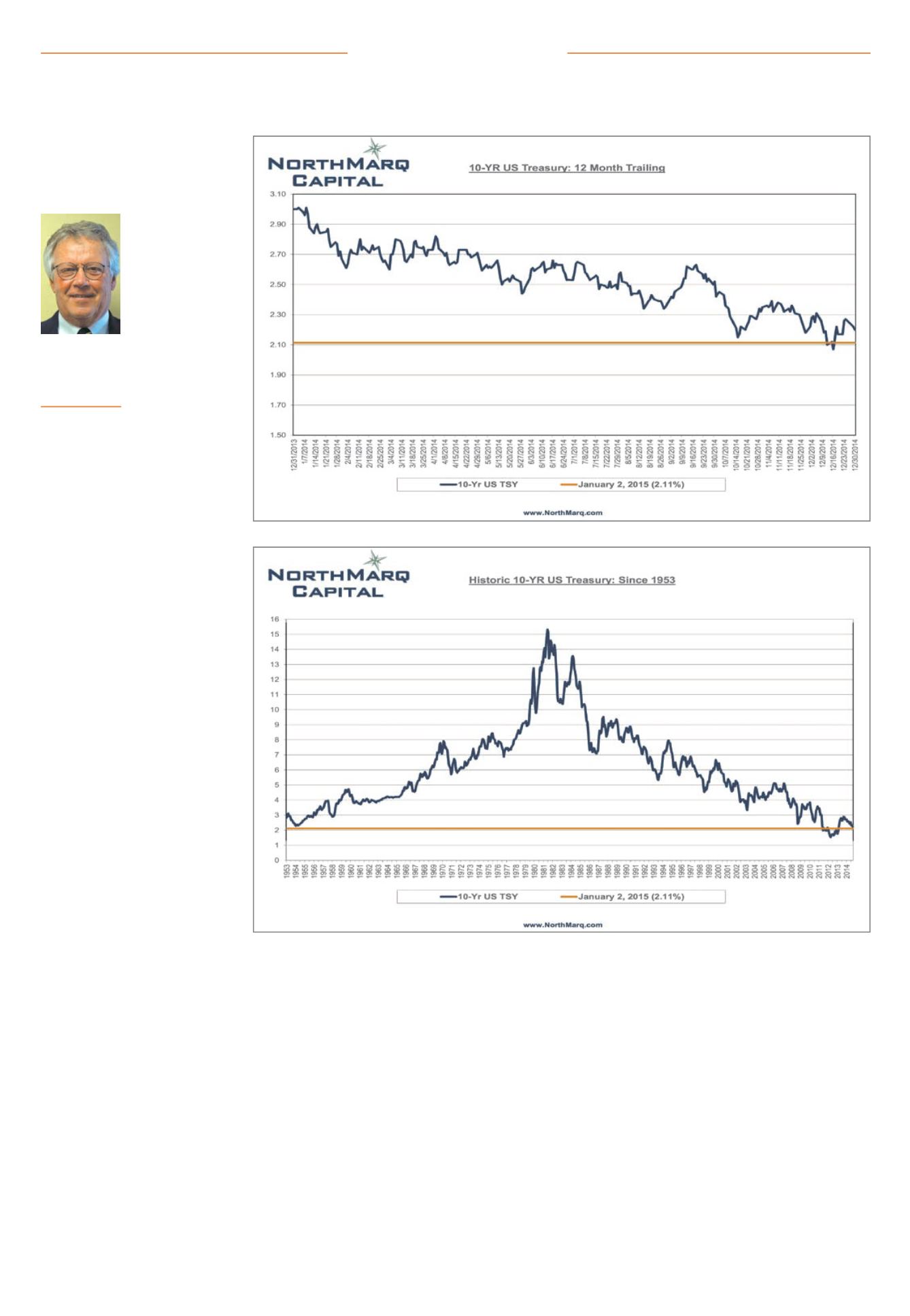

U.S. Treasury or London Interbank

Offered Rate index rates are near

all-time low points and, on top of

that, risk spreads have continued to

compress.

CREJ:

Discuss the type of lenders

who are most active.

Bye:

Most of the apartment loans

that we are arranging are through

the apartment agencies Freddie

Mac and the Fannie Mae Delegated

Underwriting and Servicing platform

through our affiliate, Amerisphere.

However, we have also closed a num-

ber of permanent loans with life

insurance companies. Our Denver

office originated a few commercial

mortgage-backed security apartment

loans in 2014, although these were

the exceptions. We were less active

in 2014 with Federal Housing Admin-

istration originations compared to

2013 and 2012.

CREJ:

Why are the agency lenders so

attractive to borrowers?

Bye:

Many of the agency loans are

focused on financing property acqui-

sitions. Although the agencies have

strict underwriting guidelines, they

are receptive to the lower cap rates

and are comfortable lending up to

80 percent of the purchase price.

In addition, they are more likely to

offer interest-only payments. They

can also provide 30-year amortiza-

tion schedules for older properties.

Another significant attraction is the

ability of the agencies to provide

supplemental loans, executed in a

very streamlined manner. Agency

loans are typically subject to defea-

sance prepayment requirements,

which makes it a cumbersome pro-

cess, although it could result in a

discounted payoff in the event of a

high interest rate environment in the

future.

CREJ:

You mentioned insurance

company lenders. How does that sec-

tor approach apartment lending?

Bye:

First of all, there are at least

three dozen insurance company

lenders, so there is a wide array of

underwriting and risked-based vari-

ables that will distinguish one lender

from the next. From my perspective,

life companies are nimble and can

provide a menu of special features

that a borrower may covet, as well as

the ability to close a loan in as little

as 30 days.

However, regardless of the pur-

chase price or an appraisal, many life

companies use internal underwrit-

ing standards based on minimum

cap rates or debt yield thresholds,

resulting in lower leverage levels.

For example, these disciplines may

result in a loan amount that is 65

percent of an actual purchase price,

even though it may be 75 percent of

their internal value. Life companies

are less likely to offer interest-only

payments or 30-year amortization,

unless the property is newer con-

struction.

CREJ:

Then why would a borrower

pursue a life company lender?

Bye:

They may be able to offer

spreads of 25 to 35 basis points lower

than the agencies, especially when

the loan term is shorter than 10

years. Alternatively, they can provide

fixed-rate terms of up to 25 to 30

years, while the agencies are limited

to a maximum of a 10-year duration.

Life companies can offer flexible

prepayment options, such as fixed

penalties or even par prepayment

over the last few years of the term.

Life companies normally hold their

loans to maturity, and therefore, are

more accessible in order to deal with

issues over the life of the loan. How-

ever, companies offering internal

supplemental loan increases are very

rare, although secondary financing is

often permitted. Funded reserves for

replacements are seldom required, as

opposed to the agencies and CMBS

standards.

CREJ:

You also mentioned commercial

mortgage-backed securities and FHA.

What are those options?

Bye:

CMBS loans would best align

with older properties or those located

in a tertiary location, where higher

leverage and a nonrecourse repay-

ment are important to a borrower.

For example, we recently arranged a

loan on a new apartment project in

Casper,Wyoming, where the agencies

and life companies were too restric-

tive on their underwriting parameters.

We closed CMBS loans on properties

located in cities in Ohio and Michigan,

where the local economies are less

vibrant, as well as in smaller commu-

nities like the oil field areas, where the

economy is less diversified. There are

exceptions to this general rule, as evi-

denced with several agency loans that

our office closed in Midland-Odessa,

Texas, and in Breckenridge, Colorado.

FHA was a more active refinance

option in 2009-2012, when capital

was less abundant. The lengthy time-

frame required to process a Housing

and Urban Development loan creates

challenges for most owners, and cer-

tainly for those operating under an

acquisition deadline. Nonetheless,

the 223(f) program offers a compel-

ling loan-to-value ratio of up to 83

percent and amortization period and

fixed-rate term of 35 years. The pre-

payment structure is somewhat flex-

ible, because the step-down penalty

phases out after nine years. Although

I have not addressed construction

lending, FHA’s 221(d)(4) construction/

permanent 40-year program remains

an attractive vehicle, notwithstand-

ing the long process.

Apartment financing question and answerFinancial Market

Steve Bye

Executive vice

president, senior

managing director,

NorthMarq

Capital, Centennial