Page 24 —

COLORADO REAL ESTATE JOURNAL

— June 15-July 5, 2016

Finance

by John Rebchook

Lakewood-based FirstBank

made a near record $722.6 mil-

lion in business loans in the first

quarter.

The loans by FirstBank, one

of the nation’s largest privately

held banks and the second larg-

est in Colorado, included con-

struction, land development and

real estate.

Indeed, most of the loans it

made involved real estate.

FirstBank also provided financ-

ing for equipment and for cli-

ents needing U.S. Small Business

Administration loans in the first

quarter.

But business lending only

accounted for about $51 million

of the total.

“The balance was for commer-

cial real estate, with roughly 50

percent for construction lending

and 50 percent for other types

of

loans,”

i n c l u d i n g

bridge loans

and refinanc-

es, according

to Ron Tilton,

president of

F i r s t B a n k -

Denver.

While First-

Bank also has

operations in

California and Arizona, Tilton

estimated 80 percent of the loans

were in Colorado.

It was an active quarter for

FirstBank.

“It was right in line with what

we did in the first quarter of 2015,

which was our biggest first quar-

ter,” in terms of lending, Tilton said.

“We are on the same pace as

in 2015.”

The two main asset classes

FirstBank made loans on were

multifamily and office. Loans

included the well-received

MOTO apartment building and

a 240-unit housing community

planned in Silverthorne.

“We also do some mixed-use,”

Tilton said. “A good example

would be a hotel with retail on

the ground floor.”

FirstBank also made retail

loans.

“We would like to do more

industrial, but we just haven’t

had that many opportunities,”

Tilton said.

FirstBank continues to make

a lot of multifamily loans, but

at the same time, it is worried

themarket is becoming overbuilt,

especially for high-end commu-

nities in and near downtown.

“My answer may sound con-

fusing, as we continue to make

multifamily loans, but we are

concerned about all of the inven-

tory coming on line,” he said.

He follows Cary Bruteig’s

analysis of the apartment market

very closely, for example. Bru-

teig, the owner of Apartment

Appraisers & Consultants, pub-

lishes Apartment Insights, a mul-

tifamily database that includes

sales, occupancy levels and rental

rates.

Because of fears of overbuild-

ing, FirstBank has tightened its

lending standards.

It’s not alone in doing so.

“My sense is that most lend-

ers are tightening their lending

standards when it comes to mul-

tifamily lending,” Tilton said.

That means that FirstBank

requires more equity in deals.

“It varies with the loan size,

but I would say that with a small

deal, we will require a minimum

of 25 percent equity and with the

larger deals we want 40 percent

to 45 percent down,” Tilton said.

As far as a “sweet spot” for

lending, “we are a little bifur-

cated,” Tilton said. “We will do

a lot of $15 million to $20 million

deals and then we might make

a very large new construction

deal, like you see in Five Points

or downtown or along light-rail

stops,” he said.

They also will provide financ-

ing for small investment groups

or one or two families that are

buying apartment communities

built in the 1970s and 1980s.

“We will do a lot of $1 million

to $2 million loans,” for those

types of buyers.

“Those deals might be for two

local families or real estate part-

ners looking to buy a small prop-

erty in Capitol Hill, for example,”

he said.

One reason FirstBank hasn’t

stopped making apartment loans

is because of the growth of Den-

ver’s increasingly diversified

economy.

“There is a lot of discussion

in our industry about overbuild-

ing in downtown or along light

rail and in TOD (transit-oriented

development) projects, but you

can argue both sides,” Tilton said.

“These are the places where the

demand is occurring,” he said.

“So we are not shying away

from lending in downtown or

TOD or RiverNorth, just because

there are a lot of projects moving

forward,” he said.

Also, FirstBank puts a lot of

stock in the track record of the

developers it deals with.

“It’s interesting, because in the

vast majority of the cases, we

have been doing business with

the people for a long time,” Tilton

said.

“But, in their next deal, they

might be bringing on a new

investment group or investment

partners, whom we have never

met before. Denver is a big city

with a lot going on, but it also is

a tight-knit community and a lot

of people want to be here,” Tilton

said.

Other News

n

Leon McBroom

and

Eric

Tupler

of the

Holliday Fenoglio

Fowler

team in Denver, recently

arranged a $14.46million loan for

an industrial property in RiNo,

which will be converted into

“creative” office space.

McBroom, an associate direc-

tor at HFF, and Tupler, a senior

managing director, arranged

the bridge and construction

financing for 2323 Delgany, an

83,133-square-foot, 100 percent-

leased industrial warehouse.

They worked exclusively on

behalf of the borrower, a joint

venture between Denver-based

EverWest Real Estate Partners

and

WHI Real Estate Partners

LP

of Chicago.

McBroom and Tupler secured

the fixed-to-floating-rate loan

through

First National Denver.

First National Denver is a divi-

sion of the First National Bank of

Santa Fe.

The initial fixed-rate loan fund-

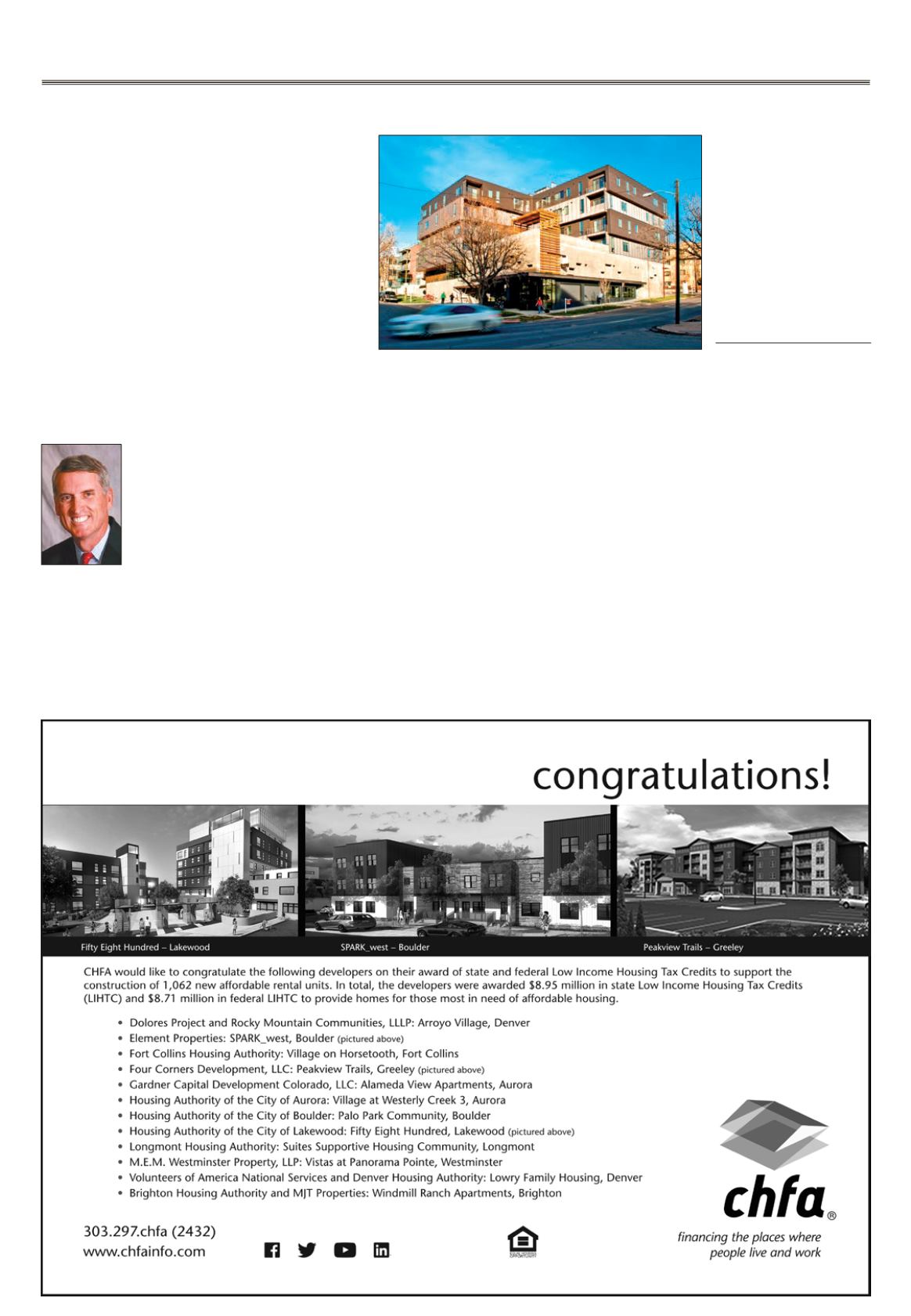

FirstBank made a loan on the MOTO apartment community at 820

Sherman St. in Denver. MOTO stands for Middle of Town.

Ron Tilton