6 / 28

6 / 28

Page 6

— Retail Properties Quarterly — November 2017

www.crej.comBIG OPPORTUNITIES ARE AVAILABLE

IN DOWNTOWN SUPERIOR.

Just outside Boulder and a short commute from Denver,

a vibrant, new Downtown Superior is taking shape. This

urban hub offers land for office and mixed-use residential/

retail, plus new office and retail space built to suit. The

area offers competitive economics, easy access to Denver

International Airport, an educated employment pool and

a sought-after location. It will be an energetic, eclectic

mix of retail, shopping, dining, entertainment and living—

walkable, sustainable and surrounded by acres of gorgeous

Colorado open space.

Fully entitled for up to 817,600 square feet of office,

retail and restaurant space; 1,400 residential units;

and 500 hotel rooms.

Visi

t DowntownSuperior.comFRESH OPPORTUNITIES FOR BUSINESS,

RESTAURANTS, RETAIL AND MORE.

That’s a

Superior idea.

R

eal estate investors and 1031

exchange buyers continue to

gravitate toward single-tenant

net lease properties as these

properties typically offer long-

term leases, minimal management

responsibilities and credit tenants.

However, the supply of new construc-

tion single-tenant properties with

long-term leases continues to dimin-

ish.With many consumers abandon-

ing brick-and-mortar retail in favor of

e-commerce, numerous retailers have

significantly reduced or halted their

expansion plans. This has resulted in

a lack of supply of new construction

long-term, single-tenant properties.

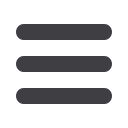

Few retailers are expanding at the

pace of dollar stores. Dollar General is

expected to open 1,000 stores in 2017

while Dollar Tree/Family Dollar plans

to open 650 stores. Needless to say,

dollar stores are expanding at a fero-

cious pace – and for good reason.

In 2016, Dollar General grew its

same-store sales by 0.9 percent,

which represented the 27th consecu-

tive year of same-store sales growth.

Meanwhile, Dollar Tree, which is the

parent company of Family Dollar, saw

its same-store sales grow by 1.8 per-

cent, which accounted for its ninth

consecutive year of same-store sales

growth. Both retailers continue to

grow their same-store sales despite

significant new store expansion,

increasing prevalence of e-commerce

and the Great Recession of the late

2000s. Dollar stores have been careful

to expand rapidly while not cannibal-

izing existing locations. Their busi-

ness model has proven to be largely

e-commerce resistant as a majority

of their consumers are located in sec-

ondary markets that

make e-commerce

cost-prohibitive and

inefficient. Lastly,

dollar stores are

resilient in difficult

economic times as

their products are

convenience goods

offered at an afford-

able cost.

Dollar General and

Family Dollar sell

name-brand prod-

ucts that frequently

are used and replenished, such as

food, snacks, health and beauty aids,

as well as cleaning supplies, family

apparel, housewares and seasonal

items. The products typically range in

price from $1 to $10. The Dollar Tree

business model is slightly different as

it sells snacks, food, candy, health and

beauty products, toys, gifts, party sup-

plies, stationery, craft supplies, teach-

ing supplies, books, seasonal décor,

glassware, dinnerware and cleaning

supplies for $1 per item or less.

Dollar General, Family Dollar and

Dollar Tree offer real estate investors

favorable lease terms. A new construc-

tion property offers an initial lease

term of seven to 15 years with up to 30

years of renewal options and minimal

to no landlord responsibilities.

Helping fuel the rapid growth of the

dollar store sector are the preferred

developers, some of which are build-

ing more than 25 stores per year.

Because the developers have such

large pipelines of properties under

construction, they typically sell a

significant amount of their product

to either allocate capital into future

development or take a profit. Since the

start of 2016, there have been over 510

new-construction dollar stores sold

nationally, according to CoStar. Previ-

ously, institutional buyers and invest-

ment funds acquired large portfolios

of new-construction dollar stores but

have since limited their acquisition of

this sector as they fulfilled their allot-

ment.

Where in the past the developers

could rely on an institutional buyer

or investment fund to acquire the

pipeline of stores, developers now are

selling the new stores in small portfo-

lios or one-off transactions to private

capital buyers. This has resulted in a

significant increase in the supply of

new-construction dollar stores on the

market and capitalization rates that

have risen slightly year over year. Cap

rates for new-construction dollar store

properties typically are between 6 and

7 percent, which is priced at a slight

discount to the single-tenant retail

market as a whole. The discount asso-

ciated with dollar store properties can

be attributed to their location, which

typically is in a secondary market.

Older dollar store properties with

less than 10 years of lease term

remaining also garner significant

investor interest as the properties

typically offer a higher return. These

Why dollar stores are the retailers of the futureMarket Update

Zach Wright

Investment sales

broker, Pinnacle

Real Estate

Advisors, Denver

Dollar stores continue to grow their same-store sales despite significant new store expan-

sion, increasing prevalence of e-commerce and the Great Recession of the late 2000s.

Please see Wright, Page 26