4 / 28

4 / 28

Page 4

— Retail Properties Quarterly — November 2017

www.crej.comMarket Update

D

enver’s roaring economy con-

tinues to attract businesses

and new residents, sustaining

demand for goods, services

and retail real estate. Ongo-

ing job growth well above the national

average has supported the unemploy-

ment rate contracting to 2.2 percent by

the end of the second quarter, one of

the lowest rates in the nation. By the

end of the year, the metro’s labor force

is expected to expand by 2.4 percent. In

addition, a rise in high-paying positions

has supported rising median house-

hold incomes, which is $17,100 more in

Denver than the national median and

translates to higher spending power.

These positive economic trends have

created robust demand for retail goods

and services at a

time when market-

wide concern over

the state of retail as

a product type has

been prevalent.

The largest retail

developments are

occurring in the out-

skirts of Denver in

suburban communi-

ties such as Castle

Rock andThornton.

Alberta Develop-

ment continues to deliver new retail

square footage as part of the planned

1-million-sf Promenade at Castle Rock.

A 139,000-sf Sam’s Club and a 125,000-

sf King Soopers opened earlier this

year, joining Ulta

Beauty and several

smaller-scale retail-

ers. On the northern

end of the Denver

metro area, Simon

broke ground on the

Denver Premium

Outlets, which will

contain 80 outlet

stores totaling more

than 330,000 sf.

While the larger

retail developments

mostly are occurring

in the outlying suburban communities,

in the urban core, older neighborhoods

are being redeveloped with mixed-use

apartment and office buildings that

also include retail components.The

most notable is the 9th and Colorado

Project, which is being developed by

Continuum and will include between

235,000 and 300,000 sf of retail space

once the project is fully completed.

In the first half of the year, 284,000 sf

of new space was delivered, with the

bulk of the activity occurring in the

northwest submarket. By the end of

2017, builders are slated to complete a

total of 750,000 sf of new retail space.

While this is an increase of 110,000 sf

from last year, it’s important to note

that the pace of development still is far

below the long-term average prior to

the recession. Developers’ restrained

and cautious approach to new retail

projects since the recession has kept

the market in balance and tenant and

investor demand for premium retail

product at very high levels.

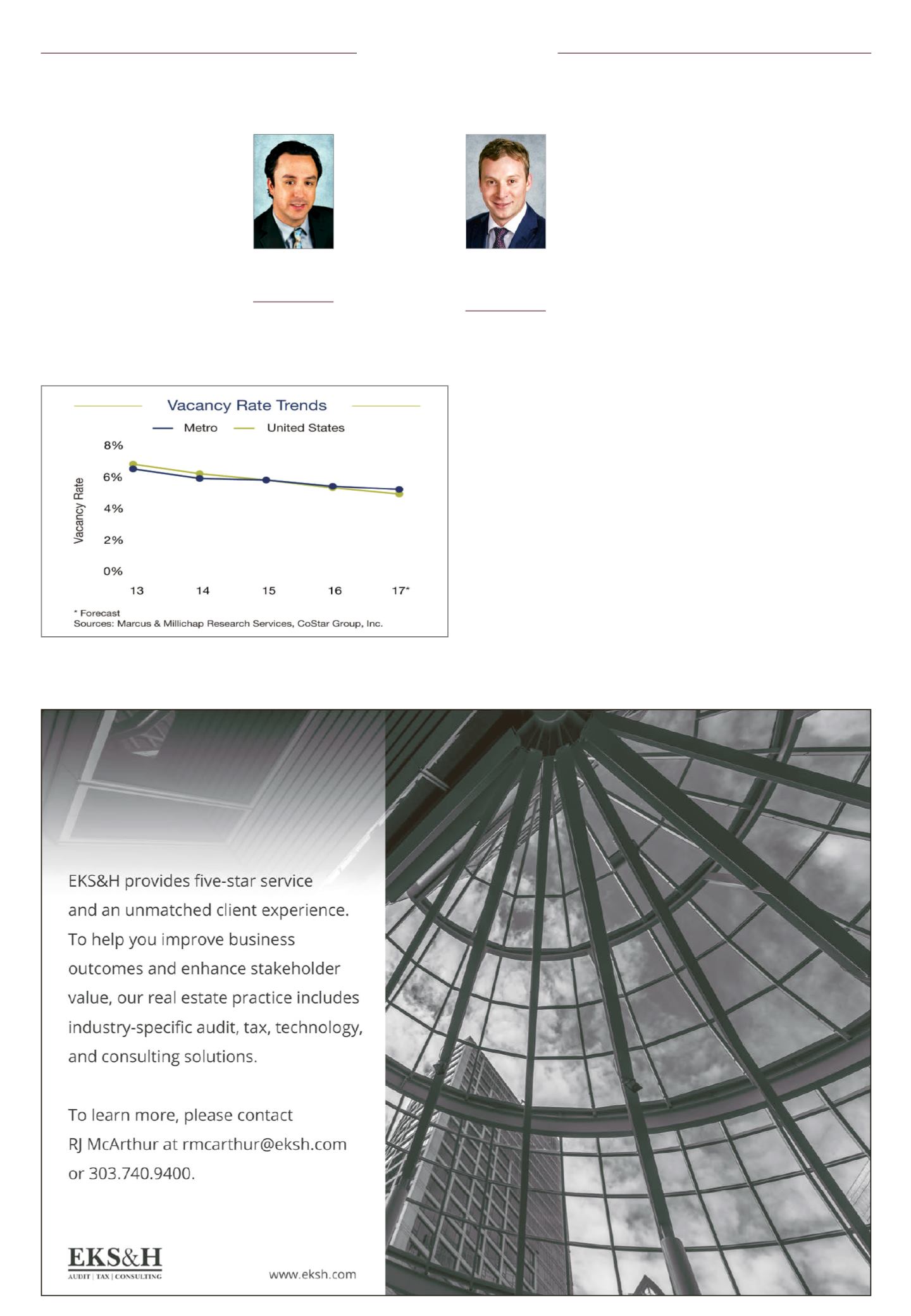

Despite the increased deliveries this

year and a changing retail landscape,

strong retail demand will compress

vacancies in the Denver area.While

the third quarter saw a slight increase

in the vacancy rate due to new prod-

uct coming on line, the full-year 2017

absorption levels will once again out-

pace new inventory, resulting in the

vacancy rate dropping 20 basis points

and building on last year’s 40-basis-

point drop. And, as retail vacancies fall,

rents will continue to rise.

Overall, demand for retail space

is driving rent growth in Denver. As

of June 30, the average asking rent

increased to $17.47 per sf and is

expected to climb 4.8 percent to $17.60

per sf by the end of 2017, the larg-

est percentage increase in nine years

and surpassing the prerecession high.

While new retail construction routinely

commands $30 to $40 per sf for well-

located shop space premises.

Denver’s positive retail real estate

performance and the area’s favorable

long-term growth outlook continues to

attract investors. Single-tenant restau-

rants and fast-food stores remain the

prime choice of many buyers, driving

yields into the 5 percent range. Many

investors who have been priced out of

this market were able to achieve more

attractive yields – in the low 6 percent

range – in recently constructed mul-

titenant strip centers with long-term

leases and attractive tenant mixes. One

such asset we recently sold in Staple-

ton was leased to eight tenants, seven

of which had signed 10-year leases

with absolutely no landlord responsi-

bility to cover any property expenses.

These types of multitenant assets are

uniquely positioned to appeal to inves-

tors more familiar with single-tenant,

Denver’s retail market riding RockyMountain highsRyan Bowlby

Senior associate,

Marcus &

Millichap, Denver

Drew Isaac

First vice president

investments,

Marcus &

Millichap, Denver

Marcus & Millichap

While the third quarter saw a slight increase in the vacancy rate due to new product coming on

line, the full-year 2017 absorption levels will once again outpace new inventory, resulting in the

vacancy rate dropping 20 basis points and building on last year’s 40-basis-point drop.

Please see Bowlby, Page 26