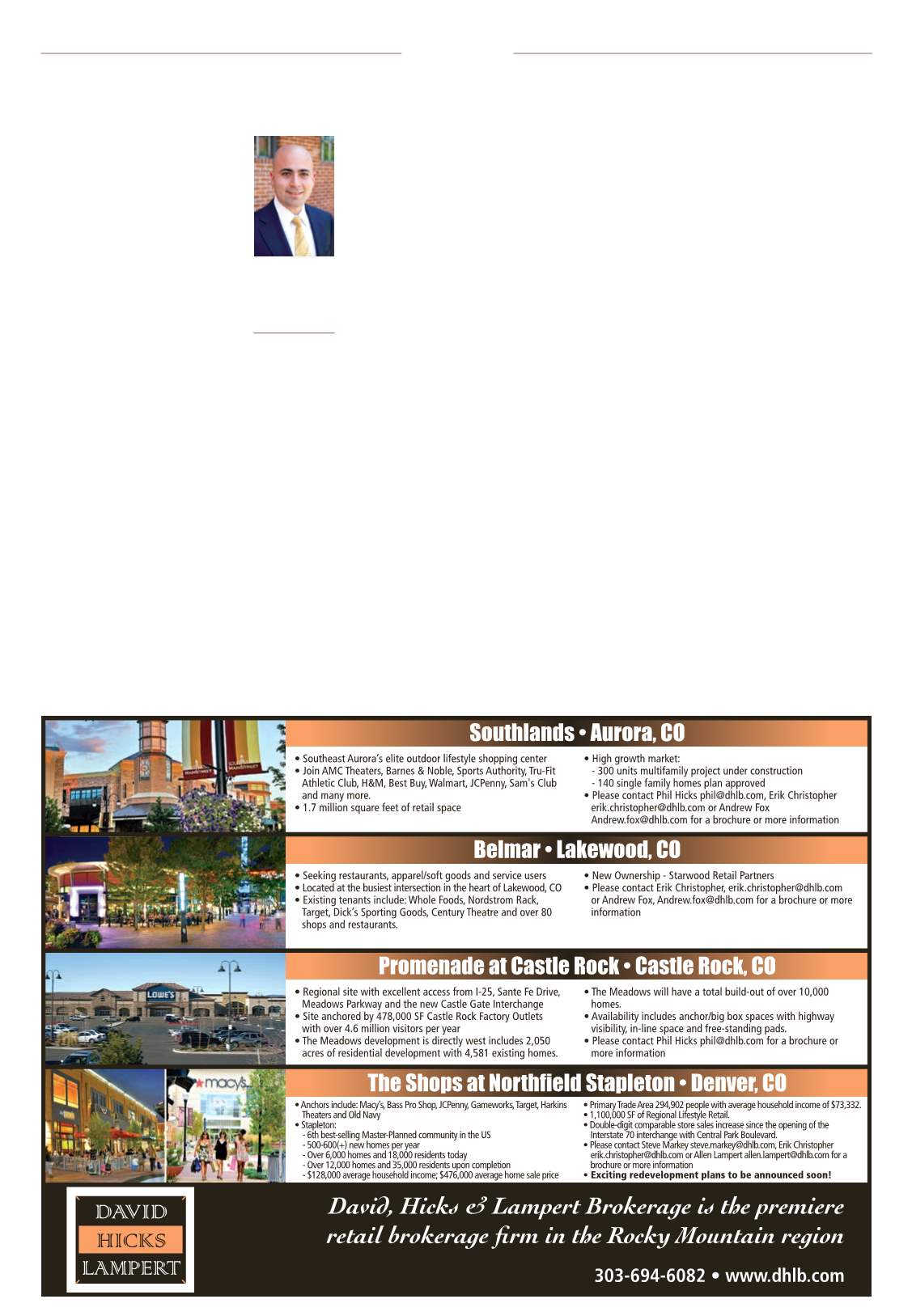

Page 8

— Retail Properties Quarterly — February 2016

I

n the first quarter of 2015, I

wrote an article for Colorado

Real Estate Journal highlighting

how different types of com-

mercial real estate lenders had

unique lending appetites for retail

properties. The retail market can be

tricky, especially in an environment

where online sales are cutting into

brick-and-mortar revenues. Accord-

ing to a December Bloomberg report,

brick-and-mortar retail sales fell 10

percent compared to the prior year.

Despite the headwind of online

sales, the capital markets remain

robust, and lenders have plenty of

capital available for retail real estate.

Over the course of the 2015 cal-

endar year, I closed over $200 mil-

lion of retail loans, here in Colorado

and out of state. These loans were

arranged through a wide variety of

capital sources including life compa-

nies, commercial mortgage-backed

securities lenders, banks and credit

unions. Lenders are continuing to

offer extremely competitive terms,

sustaining a favorable environment

for borrowers. I’d like to highlight a

few trends that I expect will carry

forward into 2016.

Life Companies

There are a few notable ways life

companies will continue to compete

for retail business. First, their con-

tinued willingness to offer forward

commitments, which allow borrow-

ers to rate-lock far in advance of

closing, will be a perfect cure for the

anxiety some property owners have

about interest rates. Even though the

Fed’s decision to begin tightening

monetary policy doesn’t necessar-

ily mean mortgage

rates will increase

– in most cases,

mortgage rates are

derived from mar-

ket Treasury yields,

not the discount

rate or federal

funds rate – many

investors are con-

sidering refinanc-

ing early. They are

considering this

even if it means

paying a prepay-

ment penalty in

order to lock a cur-

rent market mortgage rate.

The forward-commitment option

offered by many life companies

eliminates the need for this trade-

off altogether, as borrowers have the

option to lock their mortgage rate up

to 12 months prior to closing, allow-

ing the prepayment penalty associ-

ated with their existing debt to burn

off. This is an attractive strategy for

borrowers. Forward commitments

were made on approximately half of

the life company loans I originated

last year.

Another way life companies will

continue to win retail business is

by offering longer-term, fixed-rate

financing – loans with rates fixed

longer than 10 years. Many life

companies can offer mortgage rates

fixed for 15 to 30 years with nego-

tiable amortization schedules. This

is powerful for retail owners who

plan to hold assets long term since,

for the most part, the only other

commercial real estate lenders who

can offer longer-term fixed rates are

agency lenders in the multifamily

space.

There are a few ways life compa-

nies may become more aggressive in

2016. In my aforementioned article, I

noted that life companies often were

sensitive to leverage points where

the loan-per-square-foot exceeded

$200. The CMBS market won many

of the loan requests falling into this

category last year; consequently,

many life companies’ portfolios are

underweight retail.

Moving forward, there’s a good

chance some life companies will

warm up to higher loans per foot

for select retail assets, especially

grocery-anchored centers and prop-

erties located in strong urban-infill

areas. Life companies also might

seek transitional assets more aggres-

sively. Last year, a few insurance

companies began offering nonre-

course bridge loans for assets with

short-term business problems that

could be solved in the near term,

but might not be ready for a tradi-

tional permanent loan. These debt

offerings come with competitive

rates compared with the traditional

nonrecourse bridge lending market.

Investors should keep an eye out

for expansion of these programs in

2016.

CMBS Lenders

Since CMBS lenders typically are

willing to lend up to 75 percent

loan-to-value on stabilized assets,

they’ve been a common source for

high-leverage nonrecourse loans.

But for the past few years, a handful

of CMBS lenders have become more

aggressive. For select properties, 80

to 85 percent leverage now is attain-

able via the addition of on-book

mezzanine debt, where CMBS lend-

ers make higher-interest-bearing

second-position loans on their own

balance sheet (behind their own first

mortgage). While the first loan is

securitized, the mezzanine debt is

not sold in the bond market and is

available in sizes of $2 million and

up. This eliminates the need to go

to a separate mezzanine debt lender

and makes smaller “mezz pieces”

available. Historically, traditional

mezzanine debt lenders haven’t

offered loans this small.

The availability of mezzanine

debt could meaningfully benefit

retail real estate, because many of

the loans maturing this year were

arranged 10 years ago, in 2006-2007

at prerecession valuations. For retail

assets in markets where cap rate

compression has not been enough to

counteract decreasing rental rates,

mezzanine financing will prevent

borrowers from having to bring cash

to the closing table to refinance their

asset. Mezzanine financing also adds

flexibility for transactions with mov-

ing pieces.

For example, I arranged a CMBS

loan to refinance a retail asset

where a large big-box lease renewal

was pending, and its execution was

uncertain. In order to provide the

borrower comfort that the existing

debt would be refinanced by the

maturity date, regardless of whether

the pending big-box lease was

renewed, we negotiated a loan appli-

cation stipulating that if the lease

Michael

Salzman

Vice president of

loan production,

Essex Financial

Group, Denver

Lending