Page 6

— Retail Properties Quarterly — February 2016

T

he Northern Colorado com-

mercial real estate markets

have experienced remarkable

growth over the past decade.

Fort Collins-Loveland and

the Greeley metro market combined

added over 3,600 jobs to the local

economy during the past 12 months,

led primarily by strong growth in the

professional and business services

industry, which added over 1,100 jobs.

Despite the decline in the oil sector,

vacancy remains tight throughout all

product types with average asking

rates increasing during the last quar-

ter in office and retail product types.

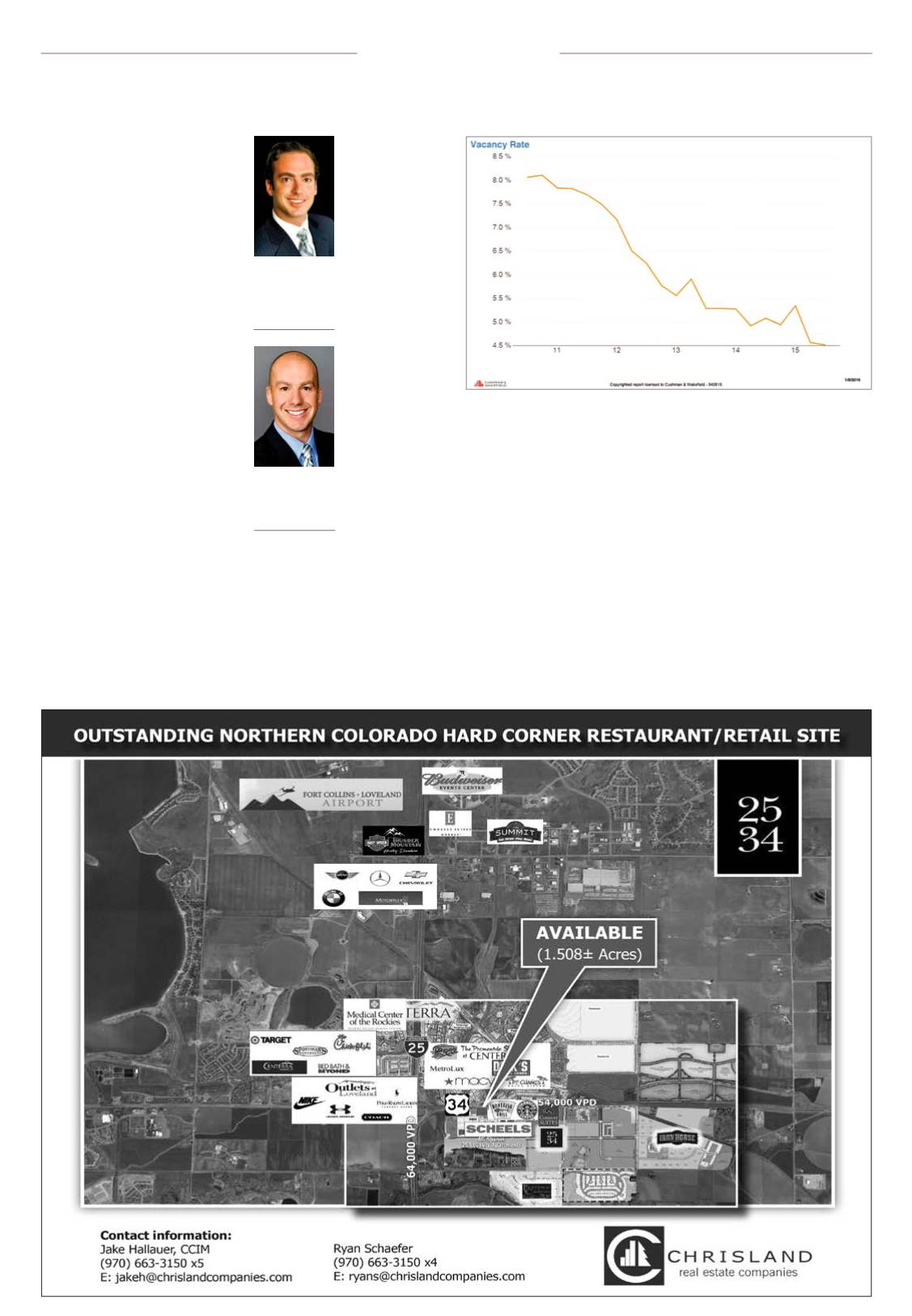

Retail occupancy levels rose a fair

amount in 2015, with net absorption

increasing to 96,604 square feet and

occupancy levels to approximately

96 percent. Vacancy rates continue

to decline, reaching their lowest level

since prior to the Great Recession,

hovering around 4.5 percent through-

out Fort Collins, Loveland and Greeley.

This is well below the historical five-

year average of 6.2 percent.

Northern Colorado experienced a

surge in new construction prices due

to a shortage of quality subcontrac-

tors and tradesmen and an increased

appetite for development. During

the recession, construction jobs were

eliminated, leaving many with no

option but to take other career paths.

We have seen a rise in the demand

for new construction projects, pre-

dominantly in the multifamily sector

but retail and office developers also

are dusting off projects and looking to

move those forward. The big question

is whether developers can justify their

projects with the increased construc-

tion costs.

On the retail

investment front,

the net-lease sector

noticed a significant

cap rate compres-

sion over the course

of 2015. Triple-net

retail properties

registered lower

cap rates across

all submarkets in

Northern Colorado.

The competition

for quality assets

pushed closing

prices higher, espe-

cially for the most

coveted properties,

which include bank

branches, pharma-

cies and national

food chains. Anoth-

er variable of cap

rate compression

is the low-interest-

rate environment.

A low interest

rate coupled with

increasing demand

to place funds,

whether it is from

a 1031 exchange,

private or institu-

tional investors’ interest, or increased

demand for quality assets. Buyers are

getting into bidding wars for these

types of assets, sometimes seeing

multiple offers once listed. It became

a sellers’ market.

The redevelopment of the Foothills

Mall by Alberta Development and

Walton Street Capital proved to be a

catalyst project in Fort Collins. The

$320 million redevelopment of the

mall is in the final stages of comple-

tion and is attracting new tenants to

our region, such as H&M and Nord-

strom Rack.

In addition,Woodward Governor is

in the final stages of completing its

new corporate headquarters near Old

Town Fort Collins at the former Link

N’ Greens golf course. Bohemian Cos.,

in a partnership with Sage Hospitality

and McWhinney, is in the final stages

of planning before it breaks ground on

a 165-room, 85,000-sf luxury hotel in

Old Town Fort Collins.

In June 2015 a developer announced

an 830,000-sf retail center to be built

at Interstate 25 and U.S. 34 in John-

stown, anchored by a giant Scheels

sporting goods store. The North Dako-

ta retailer plans to open a 250,000-sf

“retail shopping adventure” that will

be the second-largest sporting goods

store in the country.

In addition, we cannot forget to

mention the investment that Colo-

rado State University is making for its

new on-campus football stadium and

new on-campus facilities.

We continue to see the rise in

exposure as being one of the top

places to live in America. Northern

Colorado has a bright future.With the

population increasing, we’ll see strong

demand in the retail sector.With a

strong education base at universi-

ties such as CSU and University of

Northern Colorado, as well as a strong

primary employment, we are going to

see commercial real estate values and

rents continue to increase.

s

Jim Palmer

Associate vice

president,

Cushman &

Wakefield, Fort

Collins

Aki Palmer

Vice president,

Cushman &

Wakefield, Fort

Collins

Market Update

Courtesy Cushman & Wakefield

Vacancy rates in Northern Colorado from 2011 to 2015