Page 6

— Retail Properties Quarterly — November 2015

Featuring

HIGH-DEFINITION SURVEYING

SERVICES INCLUDE:

Boundary & Topographic Surveys

ALTA/ACSM Land Title Surveys

Subdivision & Annexation Plats

Architectural Design Surveys

Improvement Survey Plats

Right-of-Way Services

Elevation Surveys

Land Survey Plats

Design Surveys

Route Surveys

GIS Mapping

LAND

SURVEY

SERVICES

We are pleased to announce

Please contact us for a quote on

your next project!

Survey team led by Lyle Bissegger

& Perry Bassett, each with nearly

40 years of survey experience.

Utilizing laser scanning & real-time virtual GNSS reference networks

C

olorado Springs finally is start-

ing to see improved retail

activity, and the box-space

component is no exception.

The 18-month lag in the

economy that Colorado Springs nor-

mally sees in relation to Denver is

narrowing in 2015 as occupancy for

box space increased over the past year

and a half.

Driven by strong retail sales, the

vacancy for box space remains low in

the majority of the Colorado Springs

submarkets and is resulting in new

retail developments throughout the

area. The Colorado Springs market

has four prime retail trade areas:

North Academy, Powers, Broadmoor

and Citadel.

The North Academy area is located

betweenWoodmen Road and Inter-

state 25 in northwest Colorado

Springs. This trade area has no box

space available. Recent additions to

the market include Sky Zone, occupy-

ing 31,372 square feet in April 2014,

and GolfSmith, which took 34,043 sf in

March 2014. Nordstrom Rack is occu-

pying 31,047 sf at Chapel Hills East

Shopping Center, which is scheduled

to open in April. To make room for

Nordstrom Rack, Office Depot reduced

its existing footprint and relocated,

absorbing the 16,500-sf vacancy next

to Barnes & Noble. The North Acad-

emy submarket continues to be very

strong, seeing 100 percent box occu-

pancy for the last two years, with

average lease rates ranging from $10

to $13 per sf and $16 to $20 per sf for

junior-anchor space.

The Powers submarket in east Colo-

rado Springs has a lone box vacancy

of 84,000 sf, formerly occupied by

Kmart at Palmer

Park Boulevard and

North Powers Bou-

levard on the south

end of the submar-

ket. The area saw

some significant

new tenants with

the October open-

ing of Sierra Trad-

ing Post, operating

in 25,377 sf. Other

recent additions

over the last two

years include Planet

Fitness and Big R,

located at Con-

stitution Avenue and North Powers

Boulevard. The new Sprouts-anchored

shopping center at Barnes and Pow-

ers is slated for mid-2016 delivery and

will bring new box opportunities to

the north part of the submarket.

The Broadmoor submarket in south-

west Colorado Springs is tight for

box retailers as well. The former Alb-

ertsons at Cheyenne Hills Shopping

Center is the only vacancy. New box

development began at South Acad-

emy Highlands with the opening of a

national chain discount-department

store and a national chain discount-

warehouse store, and phase two of

that development will bring more box

options for the southwest submarket.

The Citadel area in central Colorado

Springs has the most opportunities

for box retailers, as the area’s average

annual household income of $41,000

prevents some traditional retailers

from entering the submarket. Cur-

rently, there is approximately 500,000

sf of space available, including Rustic

Hills North and South, the former

Macy’s department store at The Cita-

del mall and several other smaller box

spaces. In the last two years, Conn’s

Home Plus and At Home – The Décor

Superstore absorbed large blocks of

space. The two retailers combined

to take 170,843 sf, which was very

impactful in the submarket.

The strong box occupancy is sup-

ported by the increased retail sales

throughout the entire trade area.

The city of Colorado Springs recently

released the Sales and Use Tax Rev-

enue Report for August showing 2015

sales tax collections were up 10.4

percent year over year. Specifically,

restaurant sales tax collections were

up 7.98 percent and clothing store

sales and department and discount

store sales were up 3.5 percent and

2.76 percent, respectively. In Septem-

ber, sales tax revenues dropped 1.3

percent from the high seen in August.

However, restaurant sales tax collec-

tions in September totaled $2 million,

which is the largest collection record-

ed by an industry in the month.

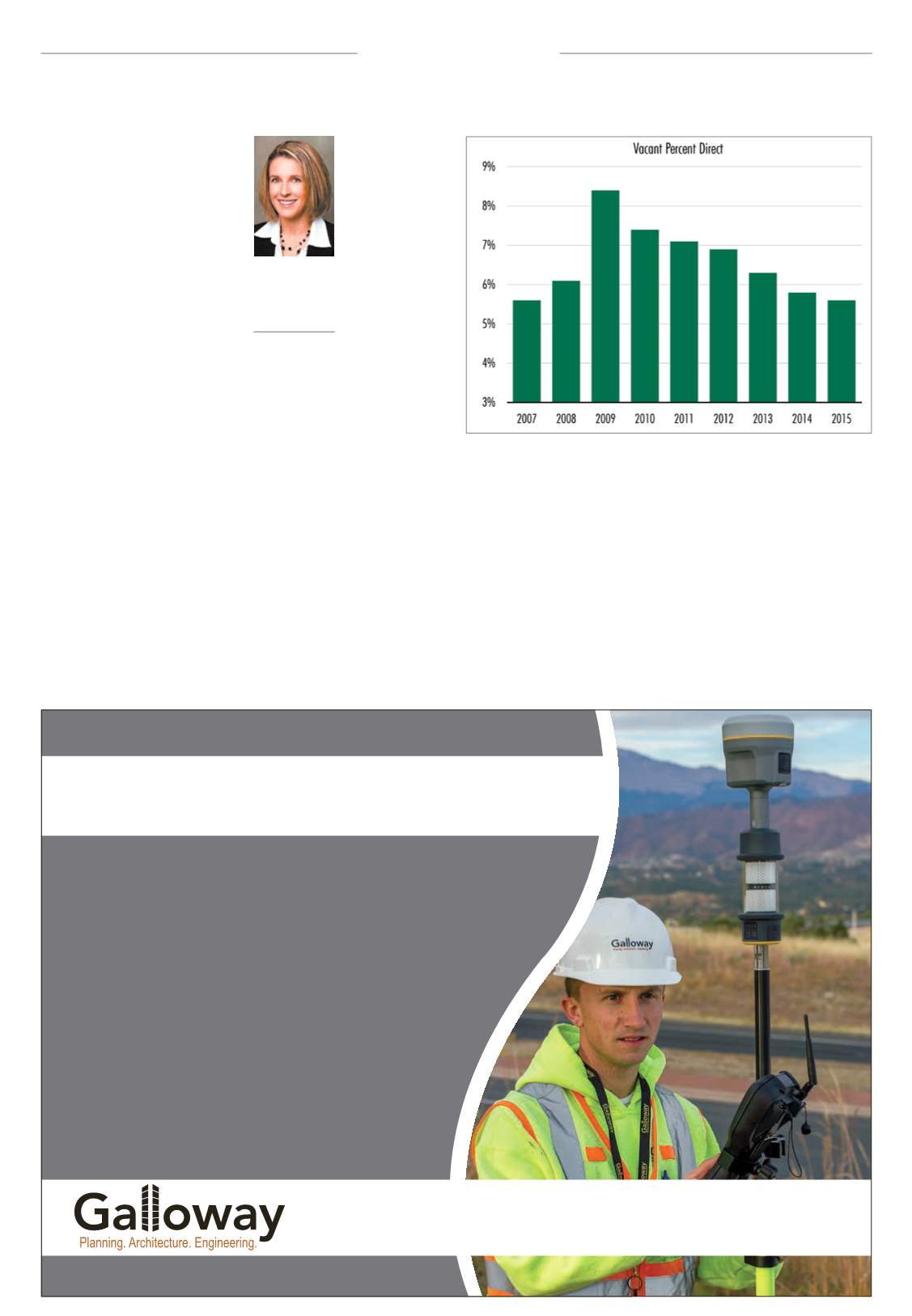

Retail vacancy in the market has

consistently declined over the last

seven years to 5.5 percent in the third-

quarter 2015, compared with a high

of over 8 percent in 2009, according to

Whitney

Johnson

Associate broker,

retail services,

CBRE, Colorado

Springs

Market Update

Courtesy CBRE