November 2015 — Retail Properties Quarterly —

Page 15

Retail Trends

houses for pickup.

In order to give consumers this

opportunity for instant gratification,

stores such as Best Buy and Kohl’s

allow consumers to buy their products

online and pick up the items in the

store. This eliminates the need to walk

the aisles, deal with purchasing at the

register and talking to a salesperson,

yet delivers that instant gratification.

Kroger andWalmart are doing the

same thing with groceries and even

offering delivery services.

The takeaway is that the store in

your hometown is now the distribu-

tion point. This could mean that these

stores may not need as much space

for merchandise or display or as large

of an improvement allowance for

build-out. In turn, they may not pay as

much rent.

The Great Recession saw the rise of

the discount store, and more people

frequently shop at off-price retailers

like Nordstrom Rack and Marshall-

now. Any stigma that may have hurt

these retailers in the past is gone,

as consumers want to hold on to as

much hard-earned cash as they can.

We know that Web shopping is forcing

retailers to compete on price, but, as

consumers, we are pushing retailers

to focus on discount concepts because

we are buying less at the full-price

stores.

Everyone wants to feel like they

are getting a deal that they can’t

pass up. The retailers are seeing this

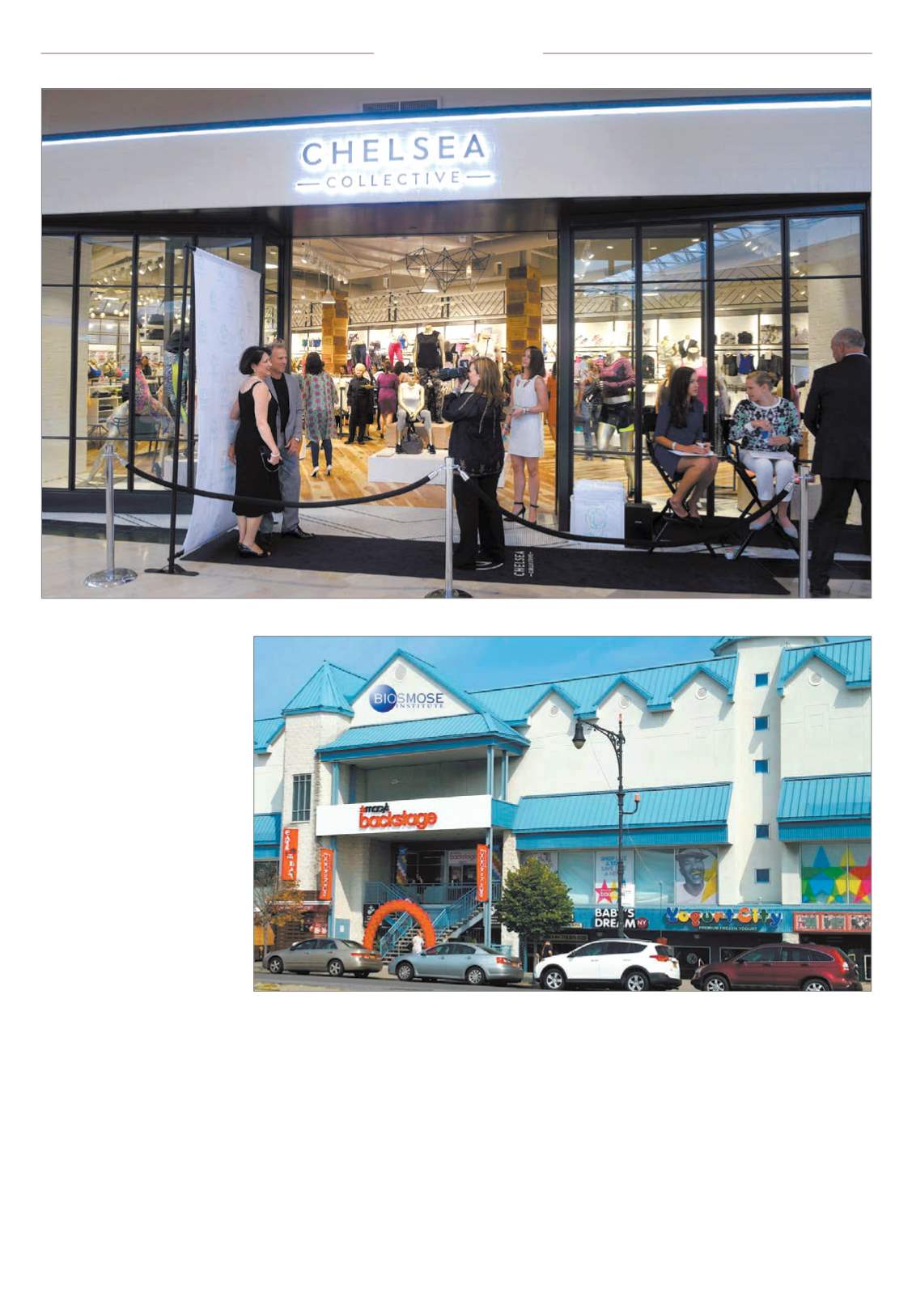

and responding. For example, Macy’s

is testing Backstage, a second-run

concept similar to Saks Off Fifth and

Nordstrom Rack. J.Crew opened J.Crew

Mercantile, which the company says is

not an outlet center, but offers outlet

pricing.

From the retailers’ perspective,

these are opportunities to diver-

sify and add stores in markets they

already may have fully built out with

full-price stores. Also, they are seeing

the opportunity to build the right-size

spaces in less-developed markets,

which allows them to be mindful of

capital expenditures. These discount

stores are less expensive to open, and

they are easily merchandised, often

with existing inventory.

New off-price concepts offer the

opportunity to expand in saturated

markets, but so do off-shoots of some

household name brands. National

retailers, especially those publicly

traded that must continually exceed

investor sales and growth expecta-

tions, are finding ways to add more

revenue sources in related businesses.

For example, Target is testing Target

Express, a neighborhood quick-stop

store for daily needs in urban environ-

ments. It also is testing Target Open

House, which will offer smart-home

elements like integrated baby moni-

tors, automated lighting and thermo-

stats for customers to learn about, test

and take home. H&M is pushing out

three new concepts – Cheap Monday,

Cos, and & Other Stories to offer hip

and cheap, luxury and high fashion,

respectively. Dick’s Sporting Goods is

trying a concept called Chelsea Col-

lective to compete with similar highly

successful athletic-fashion concepts

like Lululemon and The Gap’s offshoot

Athleta.

These specialty stores are not only

offering new revenue sources but also

are catering to the shift away from

box stores that consumers are asking

for, and instead offering stores where

consumers can get more personalized

purchasing experience for a specific

ware.

As a real estate professional, the

takeaway is to consider these con-

sumer trends and understand how

the retailers are reacting to them.

These are the uses and users we are

going to see looking for space in 2016.

As brokers, owners and developers, we

have a role in shaping the retail land-

scape.We can execute that role more

effectively if we are planning shopping

centers and merchandising plans that

recognize where retail is going and not

expecting the large-format traditional

anchors, but rather the smaller-format

spin-off and off-price bands.

With the discount stigma gone,

shoppers are looking for value and

will price shop in any avenue they

can. They are looking for a specialty

experience even if it is coming from

a national retailer. If centers are

positioned to give the retailers and,

in turn, the consumers what they

are looking for, we will fill shopping

centers.

s

Dick’s Sporting Goods is trying a concept called Chelsea Collective to compete with similar successful athletic-fashion concepts, such as The Gap’s offshoot Athleta.

Second-run concepts, such as Macy’s Backstage, try to capitalize on consumers’ desire to find a good deal.