Page 10

— Retail Properties Quarterly — September 2015

R

eal estate opportunity, like

any other market-driven

discipline, goes through

cycles. For years the rolling

green open fields and subur-

ban parcels just waiting for an idea

were plentiful. New homes were

in demand with affordable financ-

ing and there was

an aggressive and

expanding stable

of national retail-

ers who followed

the housing and

filled retail devel-

opments. New

development was

build-to-suit and

retailers and res-

taurateurs would

knock out cookie-

cutter designs and

stores aimed at

keeping costs low

and operations as much the same as

possible.

Today’s real estate realities are

higher costs for all aspects of devel-

opment and construction, challeng-

ing financing and fewer retailers

to help populate new centers. It is

becoming more difficult to find clean

opportunity locations and, once

developed, to price it affordably. In

addition, the suburbs, traditional

hotbeds of development, are becom-

ing harder to be positioned where

and how people want to live. While

open-space development continues

in the outer edges of the metro area,

developers, retailers and restaura-

teurs are looking to older and pre-

viously underdeveloped neighbor-

hoods and cities as the location for

their next great idea or concept.

Enter urban and transit-oriented

development. As connectivity and

lifestyle choices become real deci-

sion points for today’s customer,

finding locations within the older

parts of the market is good business.

An urban infill project requires cre-

ativity and vision by all parties in a

development – developer, investor,

tenant, retailer and, in many cases,

the cities where the opportunities

lie. The most successful projects in

recent years have had a distinctive

urban flair to them – Lower Down-

town, Union Station, Highlands,

Stapleton and Lowry are examples

of crown jewels of development in

recent years. Newer projects like

River North and northwest Aurora’s

Westerly Creek area are poised to

offer developers and entrepreneurs

alike wonderful opportunities to cre-

ate livable, creative and profitable

projects.

The proliferation and success of

the light-rail system has opened up

new development possibilities in

many communities. In Aurora alone,

there are nine light-rail stations, all

with development opportunities for

residential, office or retail. Unlike

other urban infill projects, TODs offer

the retailers and developers new and

well-positioned space in established

neighborhoods. Because most of the

neighborhoods already are located

close to the core of downtown and

offer housing that has character and

mature landscaping, this is attractive

to young professionals. TODs can be

new while still offering what’s best

about an existing neighborhood.

Since many of the new residents to

Colorado appear to be living near

and around downtown, TODs meet

the needs for urban living, transpor-

tation and connectivity without hav-

ing to go to the suburbs to find an

interesting place to live.

For retailers and restauranteurs,

urban infill locations provide unique

challenges. While the suburbs offer

uniformity and space, infills and

retrofits tend to have irregular space,

parking issues and infrastructure

expenses needed to bring the best

locations to code. In the past, that

was not worth the hassle, but urban

neighborhood demographics are

changing and as the lack of quality

suburban locations become scarce,

many retailers are embracing the

challenges of urban locations, flexing

their design and operational muscle,

and looking for their place in serving

these markets. Sprouts built its first

urban store in Colorado on Colfax,

and it is one of its top stores in the

country. Nearby, Chic-fil-A designed

a new urban prototype, and it is

performing strong in sales. These

successes, in part, spawned a mini

development phase in the surround-

ing area.

Cities also have to be willing to

work with developers and retailers

to help make infill projects work.

Aurora is proactively working with

large and small developers who are

interested in updating potential

locations for retail and residen-

tial development, especially in the

northwest neighborhoods. Incen-

tives for major tenants, concepts and

developments aimed at growing the

surrounding neighborhoods, increas-

ing housing density and increasing

sales tax revenue are part of the

support and focus of the city’s pro-

gram. An example of urban infill

development partnership is Stanley

Marketplace, slated to open spring

2016. Located in a refurbished avia-

tion factory, Stanley Marketplace

will host restaurants, including

the newest Kevin Taylor concept,

shops, services and entertainment

venues. Like its national counter-

parts, Chelsea Marketplace, The

Ferry Building and Gotham Market,

Stanley Marketplace will offer metro

customers a regional destination,

while servicing the nearby needs

of the Aurora, Stapleton, Anschutz

and Lowry neighborhoods. Since

its announcement, Stanley Market-

place has served as the conduit for

new residential, retail, restaurant

and innovation office development

activity in the Westerly Creek and

northwest Aurora area. Couple Stan-

ley Marketplace’s commercial infill

development with the facts that the

immediate surrounding area is one

of the most affordable housing mar-

kets in the metro area and is less

than 30 minutes from downtown,

and you have a recipe for potential

development success.

Urban infill is a trend that is

expected to drive much of the metro

area’s new and most interesting

development growth over the next

few years.

s

Development

Tim Gonerka

Retail specialist,

city of Aurora,

Aurora

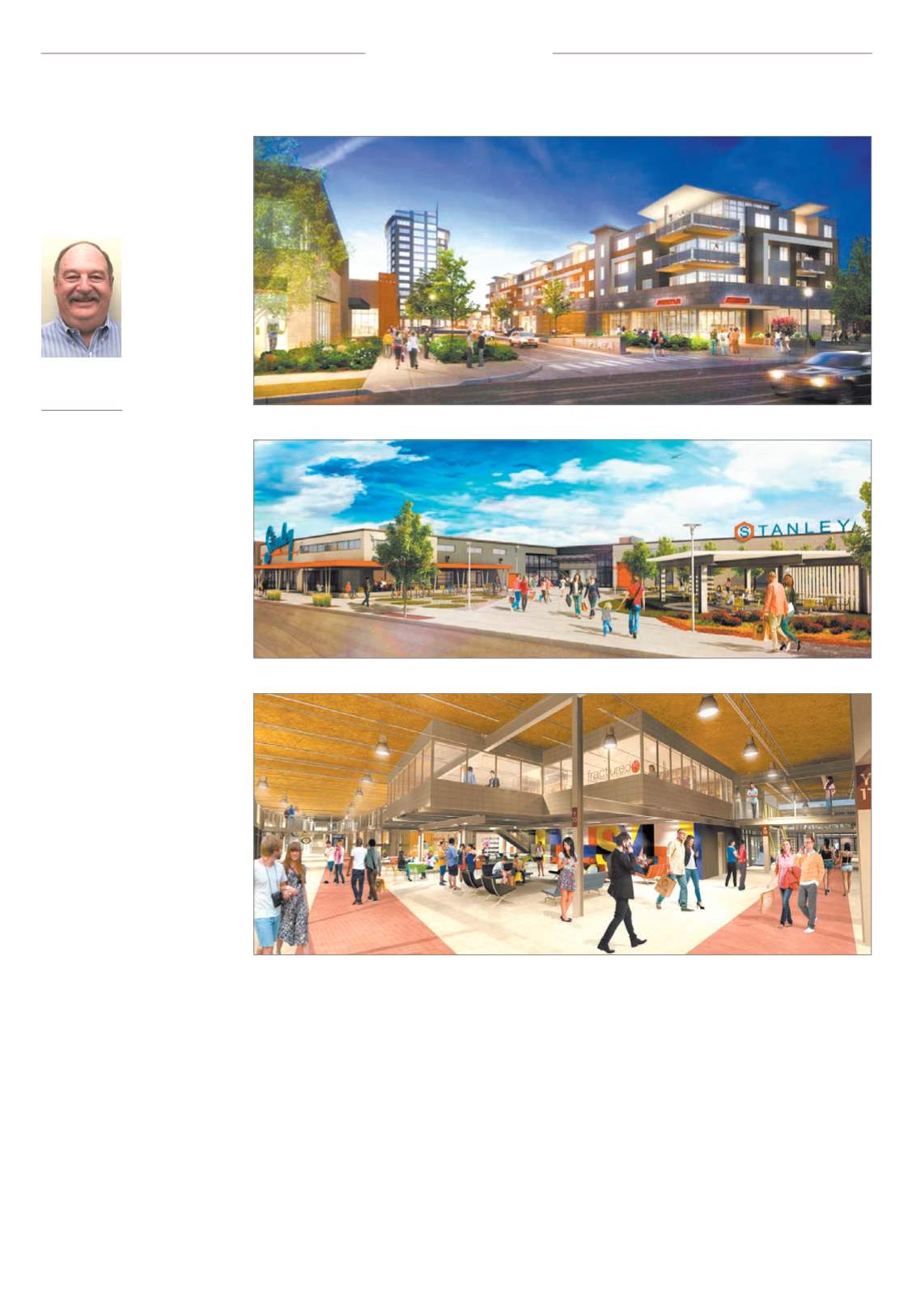

Photo courtesy: Mile High Development

The Regatta Plaza TOD redevelopment sits at S. Parker Road and S. Peoria Street.

Photo courtesy: Flightline Development

The Stanley Marketplace is a refurbished aviation factory.

Photo courtesy: Flightline Development

The Stanley Marketplace will host restaurants, service shops and enetertainment venues.