Page 10B —

COLORADO REAL ESTATE JOURNAL

— September 21-October 4, 2016

Spotlight

he expansion of the

Denver office market

continued into the

second quarter of

2016, which marked the 26th

consecutive quarter of positive

net absorption. Vacancy has

stabilized at 13.7 percent, rep-

resenting a drop of more than

600 basis points from its peak

at year-end 2009, while total

net absorption has topped 8.4

million square feet and rental

rates in core submarkets have

reached historical highs. Net

absorption for second-quarter

2016 totaled 284,330 sf,

and year-to-date absorption

reached 538,157 sf.

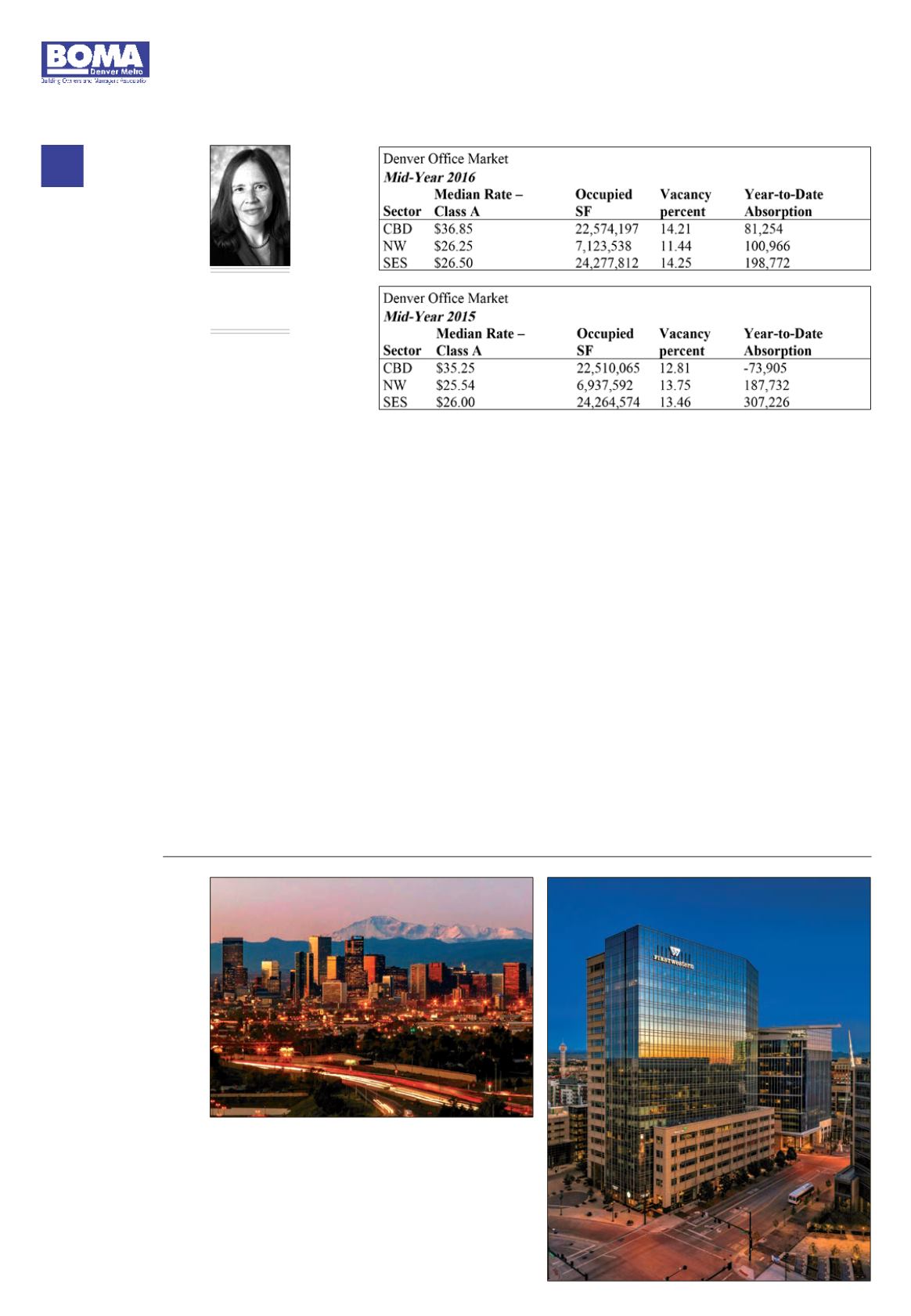

Occupancy in the central

business district (CBD) sub-

market contracted slightly in

second-quarter 2016, driven by

downsizing among oil and gas

firms totaling approximately

93,000 sf and a corporate relo-

cation. The CBD posted quar-

terly net absorption of negative

93,959 sf, but year-to-date

absorption remained positive

at 81,254 sf. Vacancy increased

to 14.2 percent from 13.9 per-

cent in the previous quarter

and year-over-year from 12.8

percent.

In the face of low oil prices

and global oversupply, Denver

has shown resilience due to its

diverse tenant mix. Downsizing

and closures by oil and gas

firms has accounted for close to

760,000 sf of negative absorp-

tion over the past six quarters,

but these losses were almost

entirely offset by growth in

other industry sectors, leaving

the CBD with flat absorption.

Though the oil and gas situa-

tion likely will get worse before

it gets better, significant move-

ins by Prologis, DaVita and

Antero Resources will drive

positive absorption of more

than 500,000 sf in the next

three to 12 months.

The northwest (NW) submar-

ket saw a continuation of the

strong performances posted

in 2014 and

2015, driven

by organic

growth.

Vacancy fell

to 11.4 per-

cent, the low-

est level since

2000, and

now is lower

than that of

the CBD or

southeast

suburban

(SES).

Quarterly

net absorp-

tion was

64,538 sf, bringing year-to-date

absorption to 100,966 sf. This

momentum is forecast to con-

tinue throughout 2016, driven

by continued growth in the

technology sector, which has

strong roots in the NW, and

new tenants in diverse indus-

tries attracted to the location

and quality of life. This growth

is fueling a housing boom,

which will further enhance the

draw of the area.

Having weathered the storm

of corporate downsizing in

2015, the SES posted positive

absorption in the first half

of 2016, driven by corporate

expansion. The SES ended the

second quarter with the mar-

ket’s strongest performance,

logging quarterly net absorp-

tion of 147,161 sf and year-to-

date absorption of 198,772 sf.

Vacancy decreased to 14.3

percent from 14.5 percent in

the previous quarter but was

up year-over-year from 13.5

percent. The Class A sector

was responsible for the major-

ity of the submarket’s absorp-

tion, with quarterly and year-

to-date absorption of 140,128

sf and 168,197 sf, respec-

tively. The SES is expected to

hold steady in 2016, buoyed

by continued organic growth

in financial services, profes-

sional and business services,

telecom, health care and

home-building-related sectors.

Direct asking rates increased

year-over-year in all submar-

kets, and rates in the core

submarkets continued to reach

record highs. In the CBD, Class

A rates rose 29.3 percent from

year-end 2009 to $36.85 per

sf, and Class B rates increased

28.9 percent to $29 per sf.

These rates continue to set

records for all-time highs. Class

A rates in some new buildings,

propelled upward by property

tax increases, have breached

$50 per sf, a level never before

seen in Denver. SES Class A

rates stood at $26.50 per sf

and have eclipsed the previous

cycle’s peak recorded at the

fourth quarter of 2008. Class B

rates were $22.35 per sf, which

beats the previous high record-

ed in 2008 and represents a

35.5 percent increase from

the cycle’s low of $16.50 per sf

recorded in 2009/2010.

In second-quarter 2016, sales

totaled 2.1 million sf valued at

$304.0 million, bringing year-

to-date totals to 5.2 million sf

for a total of $900 million. In

Denver’s red-hot investment

arena, now considered a top-

tier market, activity remains

strong, but with the exception

of core assets, pricing and

cap rates on all other product

classes are showing signs of

flattening. During the second

quarter, the office market saw

significant suburban sale activ-

ity and repricing of older Class

A office towers, particularly in

the northern part of the Denver

Tech Center, with this category

of buildings selling below or at

approximately equal pricing

from 10 years ago. This pric-

ing reflects the large capital

improvements needed for these

aging buildings despite excel-

lent locations.

Denver’s strong economy and

market fundamentals have

supported a development win-

dow for the past several years,

spurring the return of specula-

tive development. Sixteen proj-

ects totaling 3.5 million sf cur-

rently are under construction

or renovation. Although most of

the projects in the construction

pipeline are speculative, devel-

opers are still proceeding in a

disciplined manner. Current

new projects are either heav-

ily preleased or, if speculative,

confined to high-demand, niche

markets and transit-oriented

development (TOD) locations.

The future looks bright

for Denver’s economy and

office market. The University

of Colorado’s Leeds School

of Business forecasts that

Colorado will gain 65,100 jobs

and 95,000 residents in 2016.

The professional and business

services sector, one of the top

office-occupying industry sec-

tors, is projected to grow by

a robust 4.3 percent in 2016,

adding 15,000 jobs. Denver was

ranked sixth among U.S. mar-

kets to watch in 2016 in the

prestigious Emerging Trends in

Real Estate report, which cited

its quality of life, culture, grow-

ing concentration of technology

firms, strong local economy and

investment in public and pri-

vate infrastructure, all of which

will foster sustainable growth.

It is not surprising that Denver

is one of the fastest growing

metro areas, ranked seventh

for population growth from

2014 to 2015.

Lauren

Douglas

Director of Research

Newmark Grubb

Knight Frank

T

and population growth also

has brought its share of chal-

lenges to downtown. Those of

us who work or live in down-

town Denver recognize the

issues facing the city with our

proliferating homelessness

and transient population. A

number of blocks within the

16th Street Mall have become

an eyesore. It is a challenge

in major cities to care for the

homeless and Denver is no

exception.

Yet an even greater chal-

lenge has been to control and

enforce safety, littering and

sanitation. Many homeless

appear to be able-bodied and

find downtown Denver to be

a very comfortable and enjoy-

able area with a mild climate

that can sustain their lifestyle.

Fortunately, the city has rec-

ognized many of these issues

and is taking measures to

mitigate the crime and lack

of cleanliness that has come

along with the advancements

in downtown Denver.

Downtown Denver’s future

looks bright. On the heels of

over $5 billion of development

projects downtown over the

last five years that include

over 5,500 residential units,

3 million sf of office space

and 26 hotels; we have an

additional $2.5 billion in total

investments under construc-

tion and planned that include

1,200 hotel rooms, 4,600 addi-

tional residential units and

another 2.6 million sf of office

space.

Downtown Denver has

become one of the hottest cen-

ter cities in the United States.

In the last two years, Denver

has been ranked by numer-

ous publications as “best-in-

class” for business, careers,

livability, economic growth,

entrepreneurs, technology and

housing. Downtown Denver

has become a “model” down-

town with many cites wishing

to emulate. An idea and plan

that started in 1986 by some

very forward-thinking individ-

uals in a time of crisis changed

downtown Denver forever.

Downtown

1900 16th Street