52 / 100

52 / 100

Page 4B —

COLORADO REAL ESTATE JOURNAL

— July 1-July 14, 2015

D

emand for income-pro-

ducing property comes

from both popula-

tion growth and employment

growth. Payroll employment

grew 2.6 percent in 2014,

which was 6.5 percent above

the prerecession peak, putting

Denver in the top 10 percent

of U.S. metro areas for employ-

ment growth. 2015 is forecast

to increase by 2.2 percent and

then improve to 3.1 percent in

2016. This strong employment

growth is boosting earnings,

putting Denver 17 percent

higher than the national aver-

age wage.

Tourism, the state’s No. 1

economic base industry, is sup-

porting much of the overall

job growth. Lower oil prices

have not had the impact they

did in the 1970s as the Denver

economy has diversified with

professional and business ser-

vices, leisure and hospitality,

and financial activities topping

the list of economic base indus-

tries. High-tech employment

also is 2 percent higher than

the U.S. average.

All this employment growth

also has driven the commercial

and residential markets into

the expansion phase of the

cycle. Occupancies and rents

drive the earnings of proper-

ties, and these follow the eco-

nomic cycle with a lag.

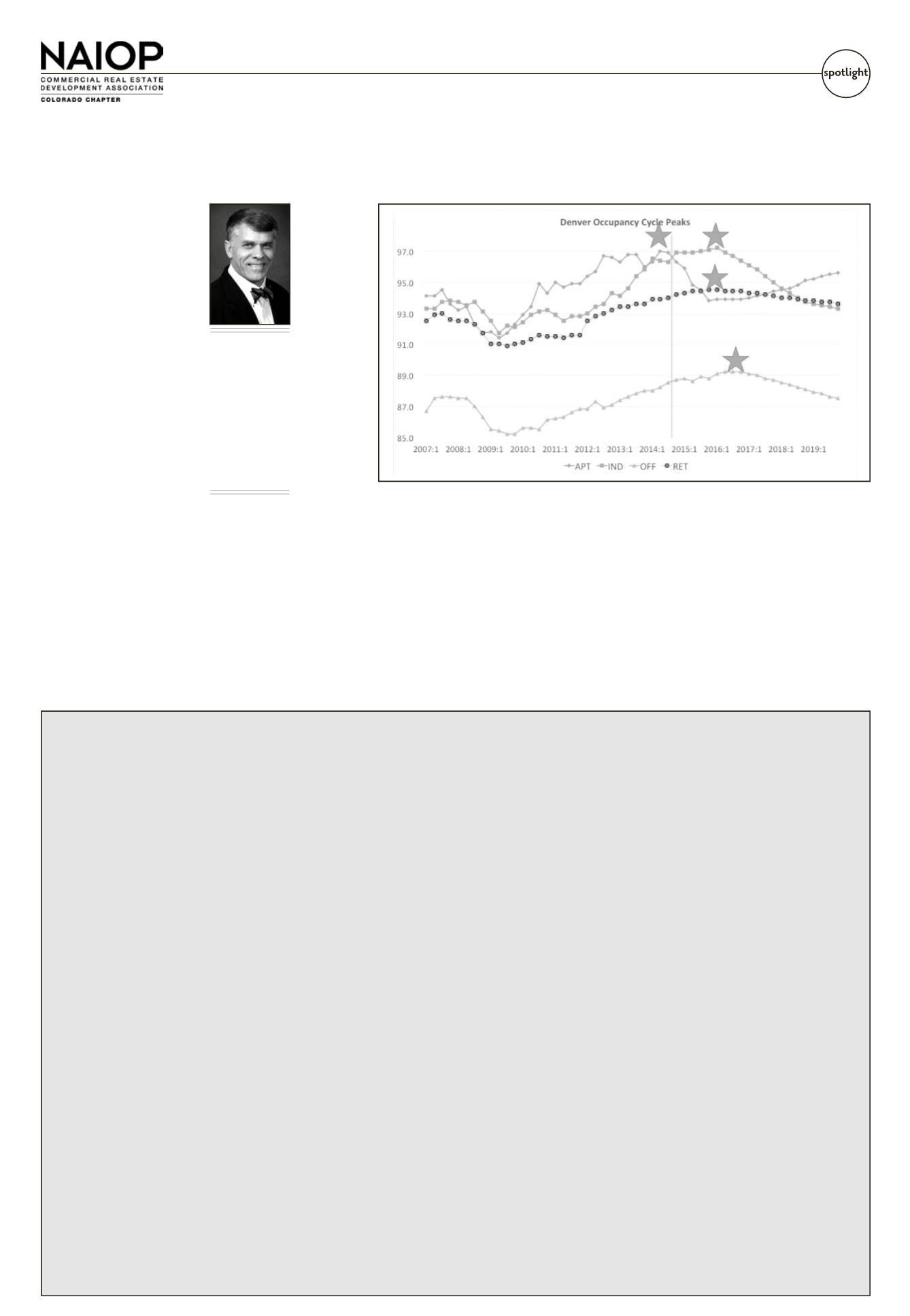

Office

occupancies

continue

their very

slow, but

steady, climb

from their

bottom in

the fourth

quarter of

2009 and are

expected to

peak in the

first quar-

ter of 2017.

Demand has

been more

moderate

than previ-

ous cycles as

tenants are

putting more

people into

less space

as they use

work shar-

ing, work-at-home, benching

(versus cubicles) and other

concepts to reduce space

needs. The historic 200 square

feet per employee usage has

dropped to 150 SFPE. Open

floor plates are needed for the

new workspace, but many old

buildings can be reconfigured.

Rent growth was over 5 per-

cent in 2014 and is expected

to be over 6 percent in 2015

before moderating back to

about 3 percent in 2017.

Industrial occupancies are

still rising and expected to

peak at over 97 percent in

the first quarter of 2016, then

moderate slightly over the next

two years. The demand from

marijuana growers has been

very strong and has absorbed

much of the old and outdated

stock in the market. Now it

appears that larger bulk space

may be in demand in the

future as growers do not have

to be connected to a specific

retail space; therefore this

new demand is not tied to

the Denver metro area, where

rents have grown substantially.

Industrial rents grew at just 3

percent in 2012 following three

years of small declines, but the

marijuana business legislation

demand in 2013 produced

over 11 percent rental growth

followed by over 14 percent in

2014. Rent growth is expected

to slow to just over 6 percent in

2015 and then drop back to a

moderate inflation level (2 per-

cent) growth in 2016.

Retail occupancies continue

to improve from their bottom

in third-quarter 2009 with a

peak of over 94 percent expect-

ed in the fourth quarter of

2016. Completions were high

in 2013 but moderated in 2014

and are expected to moder-

Glenn R.

Mueller,

Ph.D.

Professor, Franklin

L. Burns School

of Real Estate

& Construction

Management,

University of

Denver

Mueller is a real

estate investment

strategist at

Dividend Capital

in Denver.

E C ONOM I C F O R E C A S T

Denver CRE: In growth phase, headed into hyper-supply?The graph shows the property-type occupancy cycles and their peak points going forward.

Please see Economic, Page 13BPresident

J. Jeffrey Riggs

President, Baron Properties/

Essex Financial Group

303-796-9006

jriggs@essexfg.comPresident-Elect

Kevin Kelley

Vice President Development,

Colorado Office, United Properties

720-898-5872

kkelley@uproperties.comImmediate Past President

Lea Ann Fowler

Partner, Brownstein Hyatt Farber

Schreck LLP

303-223-1100

lfowler@bhfs.comLegislative Affairs Chair

Timothy Reilly

Fairfield & Woods, P.C., Esq.

303-894-4449

treilly@fwlaw.coMembership Chair

Doris Rigoni

Vice President, Kirkpatrick Bank Denver

303-907-8740

drigoni@kirkpatrickbank.comProgram Chair

Michael Strand

Associate, Snell & Wilmer LLP

303-634-2021

mrstrand@swlaw.comDirector/At-large Officer

James Mansfield

Senior Managing Director,

Cushman & Wakefield of Colorado Inc.

303-813-6400

James.Mansfield@cushwake.comDirector/Developing Leaders Chair

Ian Nichols

CPA/Controller, Gart Properties

303-270-0358

inichols@gartproperties.comDirector

Marshall Burton

Partner, Confluent Development

Services LLC

303-704-8148

mburton@confluentdev.comDirector

Jonathan Bush

Principal, Littleton Capital Partners

303-797-9119

jbush@lcpartners.netDirector

Alan Colussy

Principal, gkkworks

303-893-1990

acolussy@gkkworks.comDirector

Sherri Goldstein

Assisant Vice President,

Land Title Guarantee Company

303-331-6226

sgoldstein@ltgc.comDirector

Randall Hertel

Senior Vice President,

Majestic Realty Co.

303-371-1400

rhertel@majesticrealty.comDirector

Christopher King

President, DPC Development Company

303-796-8288

cking@dpccompanies.comDirector

Thomas Kooiman

Director of Business Development-

Western Region, Brinkmann

Constructors

303-657-9700

tkooiman@askbrinkmann.comDirector

Paul Luber

Vice President, NorthMarq Capital Inc.

303-225-2117

ptluber@northmarq.comDirector

James Neenan

Senior Vice President,

Prime West Companies

303-741-0700

jim.neenan@primew.comDirector

Tim Swan

Executive Vice President & Managing

Director, CBRE Inc.

303-628-1766

tim.swan@cbre.comDirector

Celeste Tanner

Partner, Confluent Development

Services LLC

303-803-4697

ctanner@confluentdev.comCorporate Board Member

William Lawrence

Senior Vice President-Development

Services, Transwestern

303-639-3000

bill_lawrence@transwestern.netCorporate Board Member

James Mulligan

Partner, Snell & Wilmer LLP

303-634-2000

jmulligan@swlaw.comHonorary Lifetime Director

Robert Moody

Denver Energy Network

bob@moodyres.comHonorary Lifetime Director

John O'Meara

Retired

303-877-6750

Ex Officio/2015 Rocky Mountain Real

Estate Challenge Chair

Tim Schlichting

Principal, Littleton Capital Partners

303-797-9119

tschlichting@lcpartners.netExecutive Director

Kathie Barstnar

NAIOP Colorado Chapter

303-782-0155

kbarstnar@wmrdenver.comNAIOP – Colorado 2015 Board of Directors