50 / 76

50 / 76

Page 2B—

COLORADO REAL ESTATE JOURNAL

—

March 4-March 17, 2015

T

he Denver metro

area is experiencing

extremely strong

medical office building and

hospital facility development. In

fact, from 2010 to 2014, MOB

and hospital facility development

outpaced the office market, with

over 5 million square feet of new

product in the area, compared

with 3.7 million sf of office

development during the same

time. Today, Denver remains

fertile ground for medical and

hospital facility development,

with over 2 million sf under

construction or planned for

2015.

Who is behind this

development? Between 2010

and 2014, health systems were

the major catalyst, with over 3.6

million sf constructed. Catholic

Health Initiatives’ Centura

Health led the way with over

1.6 million sf, followed by

SCL Health System (formerly

Exempla) with over 800,000 sf.

Developers were the next largest

group, building over 800,000 sf.

Medical practices finished third,

accounting for approximately

400,000 sf developed.

Development was strongest

in 2011, with 1.7 million sf

constructed, including St.

Anthony Hospital in Lakewood,

operated by Catholic Health

Initiatives’ Centura Health;

Fitzsimons Village 100, developed

by Corporex; and Red Rocks

Medical Center, which just sold

to a private investment group for

$52 million, or $442/sf.

Let’s look more closely at

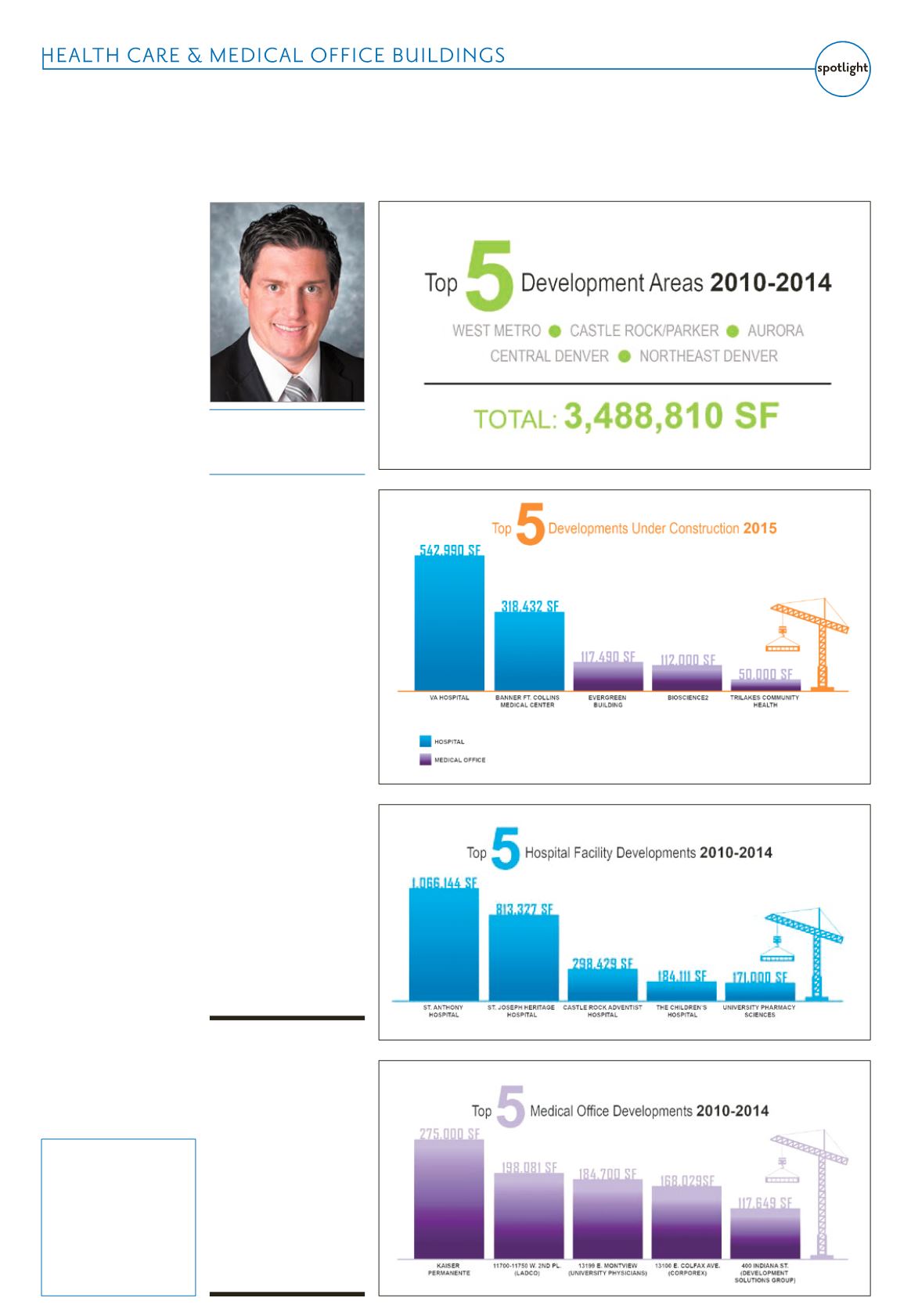

health care facility development.

Of the 5 million sf of developed

health care space, 3 million sf

were hospital facilities and 2

million sf were medical office

space. Further, on-campus

medical office buildings – those

that are located next to hospitals

– accounted for over 760,000 sf.

This number, combined with 3

million sf of hospital facilities,

equates to over 3.8 million sf

of hospital facilities and related

on-campus MOBs, and 75

percent of the total health care

development in the metropolitan

area from 2010 to 2014.

Several factors account for

the emphasis on on-campus

development. Practitioners and

medical groups often prefer

locations on affiliated hospital

campuses, and these facilities

are in high demand. On-campus

MOBs closed 2014 with a vacancy

rate of 4.29 percent, compared to

an off-campus MOB vacancy rate

of 11.67 percent, and the Denver

metro office market vacancy

rate of 14.38 percent. This low

vacancy equates to high demand;

Denver began 2015 with another

1.2 million sf of health care

facilities under construction, and

an additional 1 million sf on the

drawing boards.

With 1.2 million sf already

under construction, 2015 is on

track to be a record year for

development. The vast majority

under construction – 1 million

sf – consists of hospitals or

on-campus MOBs. Notable

developments include the

Department of Veterans Affairs

Eastern Colorado Health Care

campus in Aurora and a Banner

Hospital in Fort Collins. Of the

nearly 1 million sf of proposed

development, approximately half

are off-campus MOBs.

The outlook for health care

development in 2015 is extremely

positive with 2.2 million sf of new

deliveries forecasted – the highest

amount since 2011. New regional

and neighborhood developments

by health systems will lead the

way, and competition for market

share between health systems will

continue to drive new buildings

in growing areas including,

Northern Colorado, north

Denver, Aurora and Denver’s

southeast suburban market.

Aurora is expected to lead the

market in new development in

2015 with continued expansion

at the Anschutz Medical Campus

and with biotech and innovations

companies targeting Fitzsimons.

Other development sector

opportunities in 2015 will include

behavioral health, skilled nursing,

biotech/life sciences and off-

campus medical buildings.

Robust medical development outpacing office marketJohn Gustafson

Director, Newmark Grubb

Knight Frank, Denver

1. Denver Health – 250,000 sf

2. Fitzsimons 200 – 208,000 sf

3. 17th Avenue Pavilions –

94,360 sf

4. Medical Center at

Powerwood – 64,000 sf

5. Castle Rock Adventist,

Bldg. 2 – 60,000 sf

Top 5 Proposed

Developments

This number,

combined with 3

million sf of hospital

facilities, equates to

over 3.8 million sf of

hospital facilities and

related on-campus

MOBs, and 75 percent

of the total health care

development in the

metropolitan area from

2010 to 2014.