15 / 76

15 / 76

March 4-March 17, 2015 —

COLORADO REAL ESTATE JOURNAL

— Page 15

Finance

2

015 is anticipated to be

a very active year in

commercial real estate

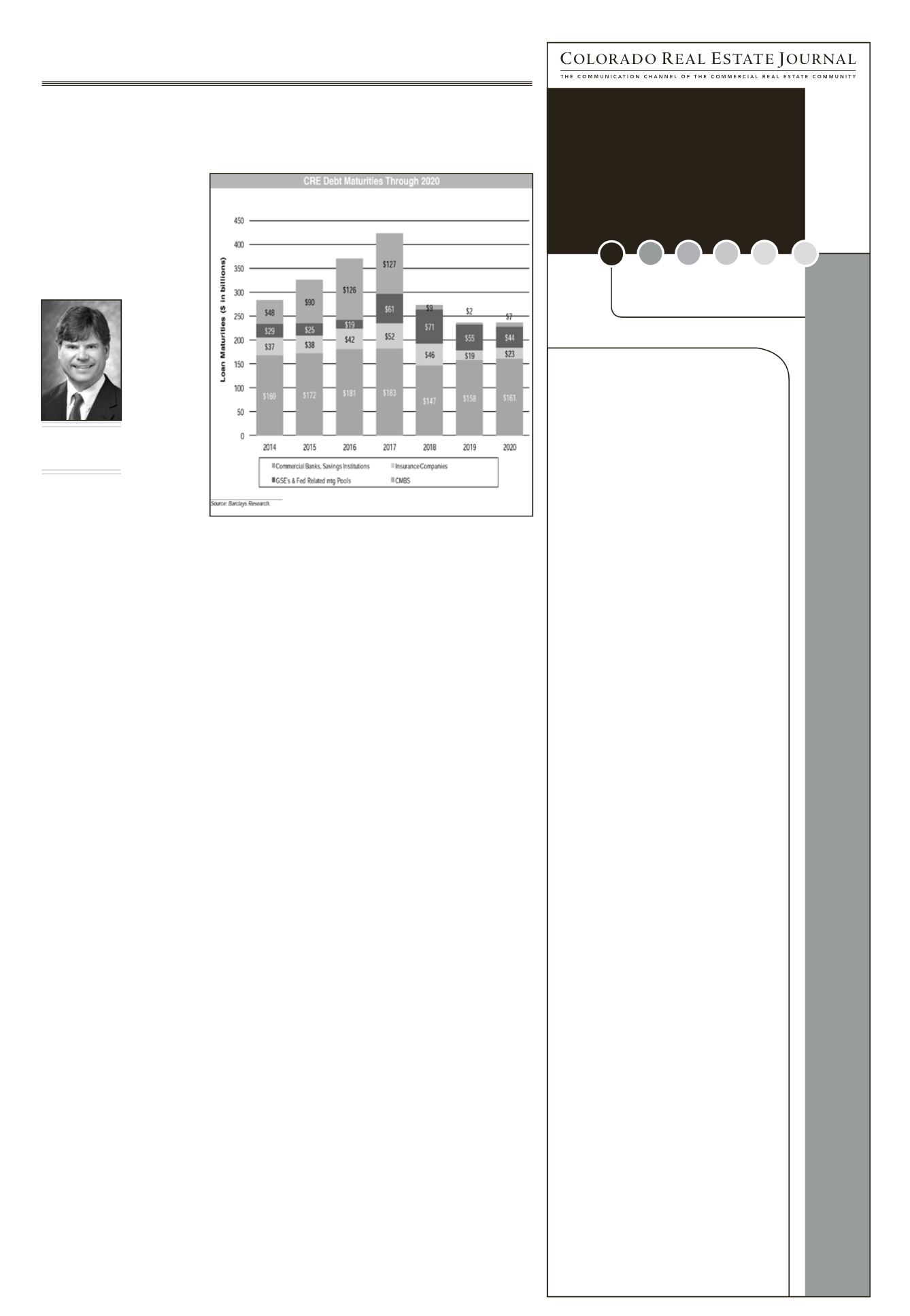

finance. 2015 is the start of

a three-year wave of increas-

ing debt maturities. The 2015

MBA CREF convention, the

largest annual gathering of

commercial mortgage bankers

and nonrecourse lenders, was

once again

held over the

Super Bowl

w e e k e n d .

The

atten-

dance was up

over the pre-

vious year

and so is the

amount of

capital. Other

good news is

I didn’t lose

any money

on the Bron-

cos, unlike

last year. Following are the key

takeaways from the conference:

n

Insurance companies.

Life

companies have increased their

2015 mortgage allocation tar-

gets marginally over last year.

The total life company volume

in 2014 was around $40 billion

and the 2015 forecast is $45

billion.

Life companies are not get-

ting more aggressive on under-

writing and generally are stick-

ing to the same rules. They’re

anticipating more takeout risk,

especially when rates start ris-

ing and cap rates follow.

A few lenders announced

“bridge light” programs. These

loans are targeted for proper-

ties that are cash flowing but

usually have a vacancy rate

between 30 and 50 percent. A

Class B multitenant property

that is 60 to 70 percent occu-

pied with no major tenant roll

risk is an ideal candidate.

There still is a lack of middle

market life insurance compa-

nies offering floating rate loans

less than $20 million. Two of

them announced new pro-

grams to compete in this area

in the second half of last year.

Out of the 25 life companies

we met with, none wants to

provide forward takeout loans

longer than 12 months. Most

won’t go past nine months and

it’s apparent they’re thinking

rates are going up and don’t

want to leave money on the

table.

Nothing has changed with

preferred product types and

preference is roughly in the fol-

lowing order:

1. High-clear industrial dis-

tribution warehouse

2. Multifamily

3. Grocery-anchored retail

4. CBD office

5. Unanchored infill urban

retail

6. Suburban office

7. Flex

8. Flagged hotels

n

CMBS.

The commercial

mortgage-backed securities

industry forecast $100 billion of

originations in 2014 and total

volume ended up around $92

billion. The forecast for 2015 is

$110 billion.

A few more conduit shops

ramped up last year and

there are now approximately

40 originators in the market

with virtually the same menu.

Although there is a larger vol-

ume of CMBS loans maturing

in 2015 vs. 2014, there appears

to be too many originators in

the market.

The demand for refinancing

is much higher than acquisi-

tion financing and CMBS lend-

ers are anticipated to get the

majority of their market share

from refinances on loan balanc-

es exceeding 70 percent loan to

value.

Consolidation is anticipated

and the first originators to fold

up the tent will be those that

are table funding for other

investors as they can’t compete

with those that have the large

balance sheets.

Bond investors have been

pushing back on aggressively

underwritten collateral. Maxi-

mum LTVs are still at 75 per-

cent with three years interest

only on average. Although

interest-only terms increased

one to two years more in 2014,

maximum LTV did not.

Interest-only terms are not

getting out of control as they

did in the last cycle. At full

leverage of 75 percent, the

typical maximum interest-only

period is three years, even with

a spread premium. Full-term

10-year interest-only loans

were getting done at 80 percent

LTV in 2007, at the peak of the

last cycle.

Fixed-rate terms are still

five, seven and 10 years with

minimal ability (without being

cost prohibitive) to time a flex-

ible exit strategy anywhere in

between.

Full-term 10-year interest-

only loans are still getting done

at 65 percent LTV or less.

n

GSEs (FNMA, Freddie

Mac, FHA).

FNMA and Fred-

die Mac did approximately $50

billion in volume last year and

the target is up 20 percent to

$60 billion in 2015. There are

no caps on volume with either

type of lender.

FHA 221 (d)(4) (new con-

struction) multifamily lending

reached a high point of approx-

imately $25 billion in volume

in 2013. 2014 volume was less

than half and 2015 is expected

to be cut in half again.

FHA 223 (f) (refinance) pro-

gram is expected to be where

most FHA originators will be

focusing in 2015.

n

Banks.

Money center,

regional and local banks were

very active last year and most

plan to increase volume this

year. The money center banks

are mainly targeting loan

amounts above $30 million on

stabilized Class A- and B-qual-

ity properties with strong bor-

rowers. The threshold for non-

recourse and/or no collateral

enhancement is approximately

55 to 60 percent LTV. Rates are

as low as LIBOR plus 175 for

high-quality assets.

Local and regional banks

focused on CRE lending are

trying to form better relation-

ships with mortgage bankers

to increase market share vs. go

direct to their borrower rela-

tionships. The longtime bor-

rower relationship seems to be

difficult to maintain due to the

amount of competition.

2015 is anticipated to be a

great year for refinance volume

as investor frustration contin-

ues due to the lack of alterna-

tive investments with similar

returns and risk. The scarcity

of quality properties located in

the top 20MSAs combinedwith

fears of cap rates following ris-

ing interest rates is influencing

many key decision makers to

refinance and refinance early.

Loans maturing in early 2016

are expected to be refinanced

this year. The 10-year Trea-

sury rate has increased from a

low point of 1.68 percent Feb

2 to 2.15 percent two weeks

later, a 28 percent increase. If

international issues continue to

subside in the media as they

have so far this year, 2015 could

be a year of a rate spike in the

second half. However, given

the volatility in a flattening

world with a high probability

of becoming more violent, who

knows what the odds are of

the opposite occurring. The big

picture shows rates are still at

all-time lows and the big ques-

tion with as many arguments

vs. counterarguments remains

– when will rates spike?

s

2015 to be very active year in commercial real estate financePeter Keepper

Managing principal,

Essex Financial Group,

Denver

For Company Profiles, Contact

Information & Links, Please Visit

www.crej.comCommercial Real Estate

Lenders

Directory

COMMERCIAL REAL ESTATE LENDERS DIRECTORY

If you would like to include your firm in this directory,

please contact Jon Stern at 303-623-1148 o

r jstern@crej.com.@

Academy Bank

Acre Capital LLC

Bank of Colorado

Bank of the West

Berkadia Commercial

Mortgage, LLC

Capital Source

CBRE|Capital Markets

Chase Commercial Term Lending

Colorado Business Bank

Colorado Lending Source

Commerce Bank

Commercial Federal Bank

Essex Financial Group

Fairview Commercial Lending

FirstBank Holding Company

Front Range Bank

Grandbridge Real Estate Capital LLC

Heartland Bank

JCR Capital

Johnson Capital

JVSC-CBRE Capital Markets

KeyBank N.A., Key Commercial

Mortgage Inc.

Merchants Mortgage and Trust Corp.

Montegra Capital Resources,

Private Lender

Mutual of Omaha Bank

NorthMarq Capital, Inc.

RNB Lending Group

TCF Bank

Terrix Financial Corporation

Trans Lending Corporation

U.S. Bank – Commercial Real Estate

U.S. Bank SBA Division

Vectra Bank Colorado, N.A.

Wells Fargo SBA Lending

Wells Fargo N.A. – Commercial

Real Estate Group

West Charter Capital Corp.