98 / 100

98 / 100

Page 22

— Retail Properties Quarterly — February 2015

A

s I think about retail in Col-

orado, two specific trends

come to mind – shopping

centers have made an effort

to upgrade and big-box

retail is downsizing.

There has not been much new

shopping center development, but

there have been many redevelop-

ments of existing centers. Shopping

centers and strip malls provide an

ease of use and single-stop conve-

nience for a quick shopping outing.

Usually, a stop at the anchor retailer

is followed by a visit to a small shop

next to it and then you are on your

way. It is a great model that leads

to success for all retailers involved.

However, success for all is based on

success for one, the anchor tenant.

Time and time again, centers that

lose the anchor tenant struggle to

maintain business.

Courting a new anchor tenant can

require extra work. In order to com-

plete the deal, the anchor tenant

may want upgrades. The request for

a new façade for the anchor tenant,

and the rest of the center, is becom-

ing a typical scenario.

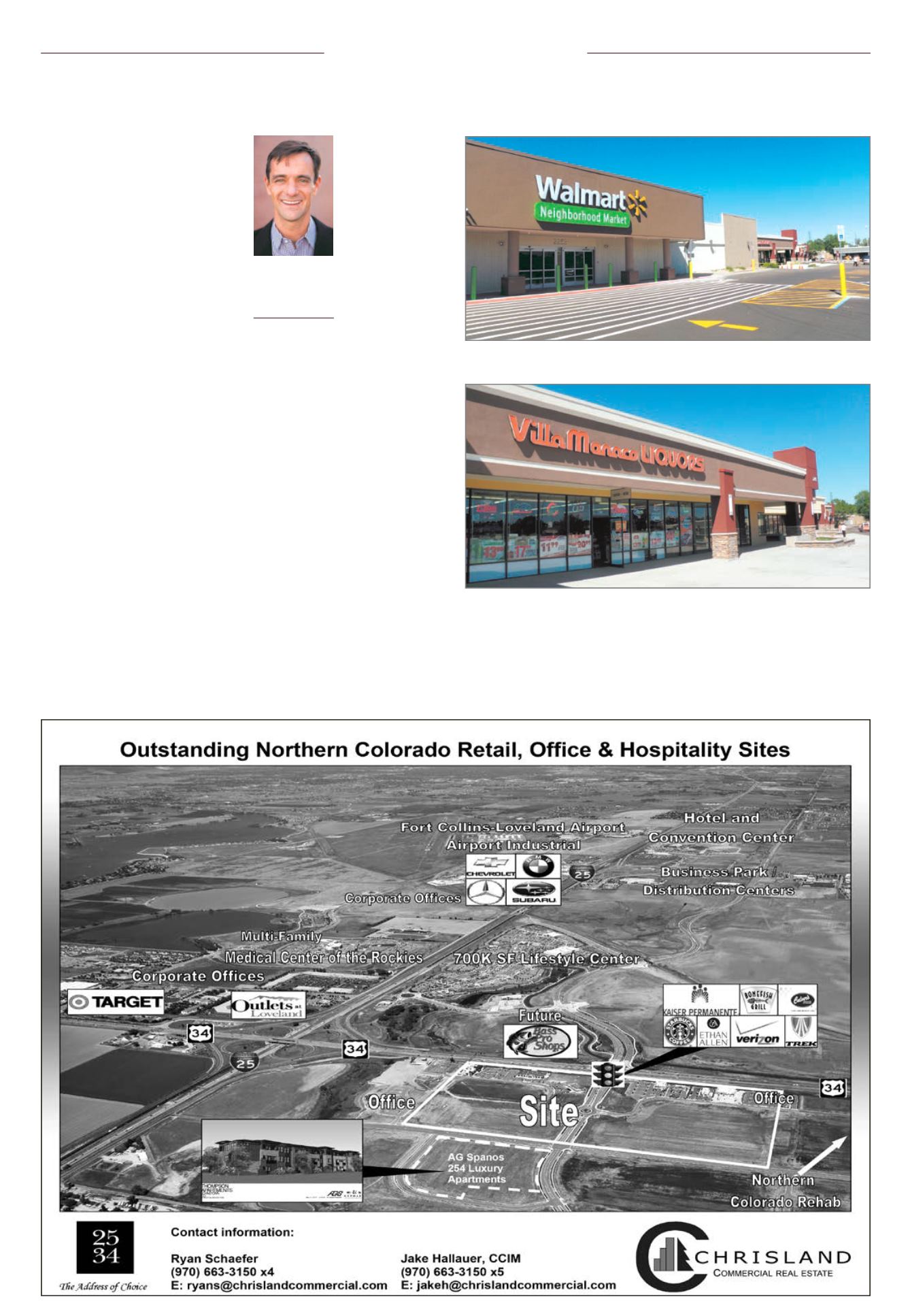

At centers like Villa Monaco in

Denver and Westminster City Cen-

ter, the new face-lifts are spurring

development. The center becomes

attractive not only to shoppers, but

also to new retailers who want to

get in on the action. The bottom line

is having a successful anchor tenant

and adding a new look can make

or break a shopping center. Think

about how many times customers

shop at the anchor store, and then

visit several of the small shops on

their way out.

Speaking of anchor tenants, the

grocery saturation

is still ongoing

with King Soopers

leading the way.

Walmart, Whole

Foods, Safeway,

Trader Joe’s and

Sprouts are fol-

lowing suit, and

soon Winco Food

also will have a

presence in the

Colorado market.

Smaller footprints,

which give the

impression of a

smaller local grocer, appear to be

the focus of these stores. However,

there are exceptions, such as the

new King Soopers, built by Maxwell,

at Broadway and Littleton, which

is 20,000 square feet larger than its

traditional stores.

The market also is busy with

urban, mixed-use properties. Quick-

serve restaurants and smaller users

are very popular, and we are seeing

lots of multitenant ground-up sub-

urban projects. The sites with better

visibility are in high demand, while

the market in general is experienc-

ing lower vacancy and higher rental

rates.

The larger developer/shopping

center owners have a strategy of

approaching underperforming big-box

retailers, renegotiating leases and tak-

ing back some space. This approach

allows those owners to lease smaller

space to smaller users, therefore gain-

ing more rent for their center.

The other theme we are see-

ing from large big-box retailers is

subleasing space to retailers to sell

their product inside of the main

tenant. JCPenney has subleased

space to Sephora, a skin care, make-

up and fragrance retailer. Walmart

has similar set ups with health care,

tax filing and eyeglass stores locat-

ed inside the large retailer. Sub-

leases enable the big-box retailer to

maximize return on investment – it

costs space, but the stores are able

to collect rent on it.

s

Shopping centers and big-box retail are adjustingDeveloper Spotlight

Chris Strom

Director of business

development,

Maxwell Builders,

Denver

Renovation of Villa Monaco shopping center at South Monaco Parkway and Evans

Avenue with anchor-tenant Walmart.

The Villa Monaco renovation continued throughout the center, providing a clean,

updated look.