91 / 100

91 / 100

February 2015 — Retail Properties Quarterly —

Page 15

Shopping Trends

R

etail in central Denver

neighborhoods is booming

with strong job growth, new

millennials arriving daily

and a limited supply of real

estate. This creates not only oppor-

tunities, but also several challenges

for the central retail markets. All

the new, young people downtown

is driving demand for housing as

well as places for these folks to eat,

shop, socialize and recreate. Central

Denver retailers are now defined as

hip, progressive, artisan, foodie and

trendy, which is what its young, rap-

idly growing population is looking

for.

The growing demographic is just

what retailers are looking for as well

– young, employed and without kids,

which means, unlike me, they have

time and money to spare.

The challenge for landlords, devel-

opers and investors is how to bal-

ance the need for predictable, stable

and creditworthy tenants with a

track record that banks and inves-

tors desire, with the demand for

hip and progressive entrepreneurs.

Something new and exciting could

be great for a property, but which

cool new restaurant or retailer is

going to have the long-term success

that makes the bank and investors

happy?

The other prevalent market

dynamic in central Denver has

been the new ground-floor retail

opportunities that have come with

the boom in multifamily develop-

ments. Though it has been great

to have new product provided in

mixed-use developments, it also has

been a challenge for retailers to get

comfortable with this product type.

Retailers are used to single-story

buildings with visibility, access and

ease of parking as top priorities

when choosing locations, and many

of these fundamentals are tested in

a mixed-use project.

My company is spending more

time than ever helping landlords

and tenants navigate these trends.

Our experience with urban proper-

ties, as well as with retailers and

landlords in traditional shopping

centers, has given us an opportunity

to help bring these two together.

The landlords of urban properties

take advantage of the hot market,

and the owners of traditional shop-

ping centers are able to attract new

active tenants.

Mixed-use retail.

Millennials are

driving demand for urban housing

and thus creating the multifamily

construction boom we are currently

seeing. The good news for retail ten-

ants looking for space is that almost

all of the new large multifamily

developments include ground-floor

retail, which is helping to balance

some of the demand for new space.

The challenge is that many mixed-

use projects are built with the resi-

dential units as the primary focus,

leaving ground-floor retail spaces

struggling because they are not

traditional real estate assessment

models.

Access, visibility, parking and

other key aspects that retailers

typically are looking for are differ-

ent in an urban

setting than in a

traditional shop-

ping center, which

makes it difficult

for retailers to

assess these sites.

Since retail is only

a small portion of

the overall project,

there is not a con-

sistency in retail

dynamics that one

would find in more

traditional retail

settings, making it more difficult

to prelease some of these projects.

Because retailers have difficulty

applying traditional formulas (traf-

fic counts, ingress, egress, parking

stalls) and their spaces can be less

visible because they are a part of a

large vertical building, they prefer

to wait until projects are substan-

tially complete, and physically walk

the site to feel comfortable with

it. These projects tend to lease up

later into the development pro-

cess than single-story retail, and a

retailer who is not local has to be

really interested in order to make a

trip to walk the site. Working with

landlords to help gain perspective

on what retailers are looking for

at these sites, and tenants to help

them assess which opportunities

are right for them, is key throughout

this process.

From the developer perspective,

it is important to know that not

all ground-floor space has to be

retail. There are other ways to use

the ground-floor space if the cor-

rect retail dynamics are not there.

However, it is enticing because it

boosts the pro forma and activates

the front door of the project, while

empty ground-floor retail does noth-

ing to help the bottom line or the

appearance of a new development.

For retail in mixed-use buildings to

be successful, there has to be strong

pedestrian traffic and a surrounding

cluster of active retailers creating

enough activity to overcome a retail-

er’s traditional dependence on auto

traffic, easy access and parking.

Restaurants.

The central Denver

restaurant market is hot, but beware

of the revolving door. 2014 was a

record year for restaurant openings

in Denver, as Westword tracked over

300 restaurant openings through-

out the year. (Almost one per day!)

Compare that with 2013, when there

were 200 restaurant openings. Hip,

new restaurants tend to open with

great fanfare and are quick to be

touted as a smashing success, while

restaurant closings seem to get

lost in the noise created by all the

grand-opening celebrations. West-

word also reported 100 restaurant

closings in 2014. This is still a very

healthy restaurant market for land-

lords, with a net gain of 200 restau-

rants. The challenge is how to avoid

being in the situation where your

space becomes a revolving door of

openings and closings, a trend that

never seems to work out for anyone.

With demand high and a limited

supply of restaurant space, the law

of supply and demand says rents

will keep pushing higher. With

higher lease rates and new entre-

preneurial restaurateurs who either

overlook their occupancy costs

due to the desire to get a space, or

are inclined to inflate their poten-

tial sales, many restaurants are in

trouble the day they sign their lease.

Restaurants generally look to keep

their rent plus triple-net expenses

in the range of 6 to 8

percent of their total

sales.

It is important for

landlords to under-

stand that the long-

term success of their

tenants is dependent

on keeping rents in

line with a restaurant’s

potential sales. Col-

lecting the highest

potential rent requires

finding tenants that

will achieve the high-

est sales in a particular

location. This can be

challenging because

much of the current

activity for restaurant

space is coming from

new one-off concepts.

A look at the sales-per-

square-foot numbers

of national brands can

help landlords under-

stand what the rent-to-

sales ratio looks like,

since most are familiar

with these concepts

and the average unit

sales are made public.

Restaurant chains like

Chipotle are attractive

to developers not only

because of their credit

rating (or because their

burritos are so tasty),

but also because they

have some of the stron-

gest sales-per-sf numbers of any

restaurant concept out there. A Chi-

potle store will average $2.17 million

in sales out of a regular size space of

2,580 sf. This breaks down to $840.69

per sf at 6 to 8 percent, meaning this

store can be profitable with gross

lease rates in the $50 to $65 per-sf

range for base rent plus triple-net

expenses.

With rents plus triple net expens-

es in central Denver reaching record

numbers, developers need to look

at whether the tenants they choose

can sustain high enough sales to

stay in business and avoid the costs

of the revolving door.

s

Retail product takes different forms in DenverJohn Livaditis

President, Axio

Commercial Real

Estate, Denver

Restaurants are repurposing old, industrial spaces like Linger, which used to be a

mortuary.

Over time vacancy rates have decreased while rental rates have increased for both

retail and restaurants.

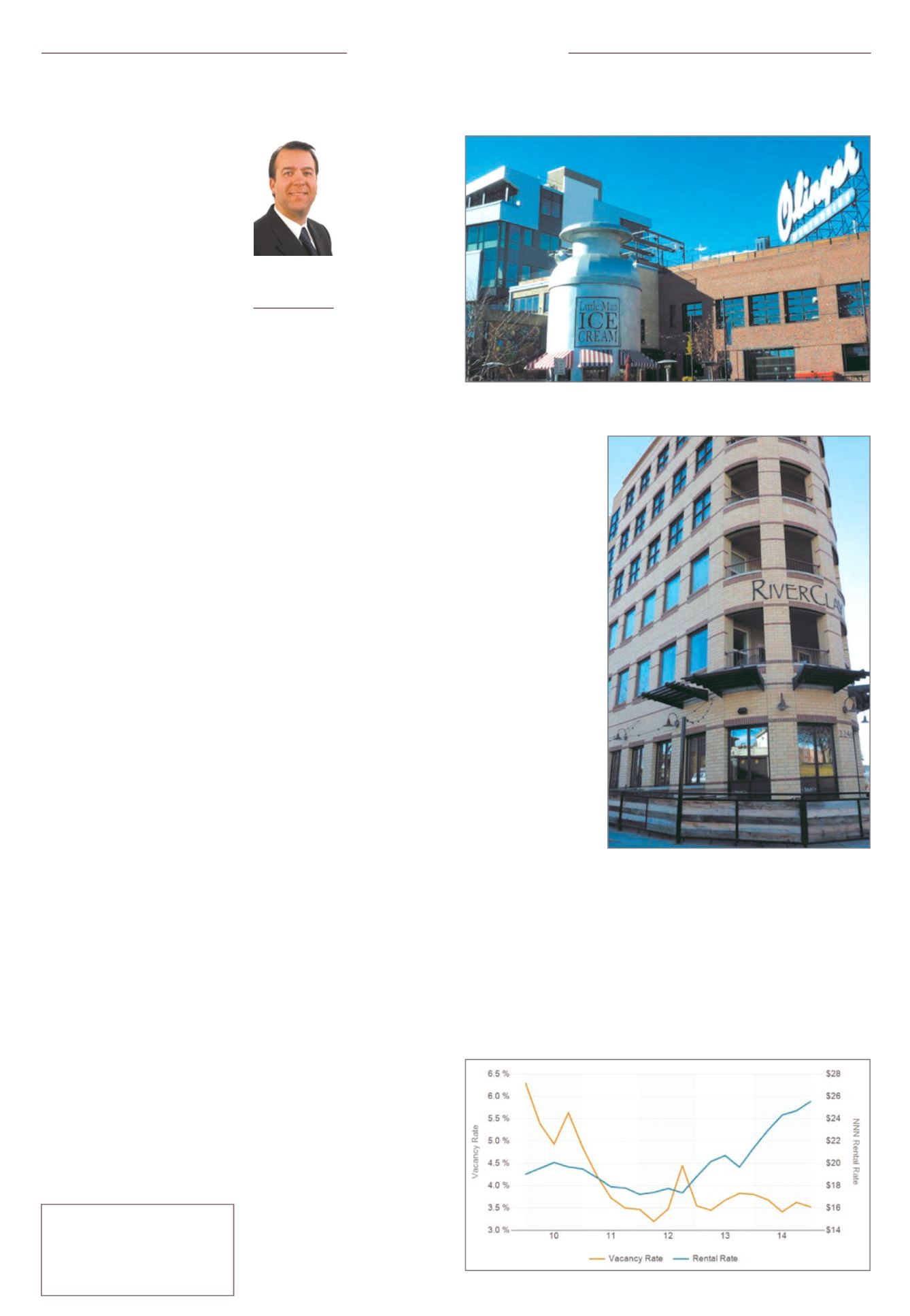

Many developments incorporate mixed-used elements with

ground-floor retail space in apartment buildings, like at

River Clay.

Chipotle

$840.69 per sf

Panera Bread

$548 per sf

Noodles & Co.

$453.46 per sf

Average gross sales