8 / 24

8 / 24

Page 8

— Health Care Properties Quarterly — January 2018

www.crej.comMarket Update

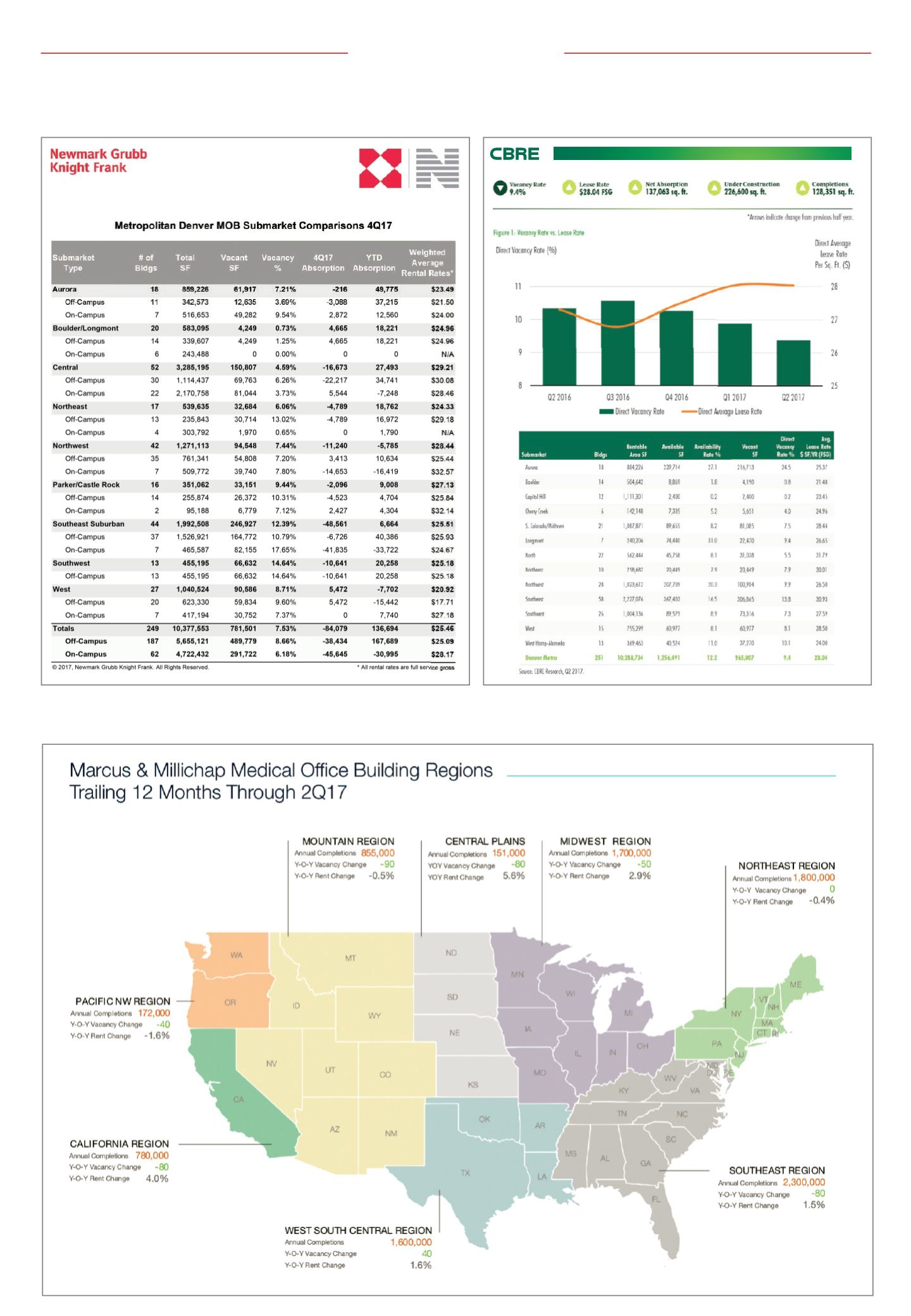

A look at recent numbers defining the metro Denver and national medical office building market

H1 2017

CBRE Research

© 2017 CBRE, Inc. | 1

MARKETVIEW

Vacancy Rate

9.4%

Under Construction

226,600 sq. ft.

Completions

128,351 sq. ft.

Net Absorption

137,063 sq. ft.

Denver’s medical office building (MOB) market

experienced solid fundamentals in the first half

of 2017 due to strong demand for quality space

and favorable demographic trends. Positive net

absorption of 137,063 sq. . was achieved in H1

2017. The direct vacancy rate decreased to 9.4%

versus 10.3% a year ago, and the overall

availability rate remained stable at 12.2%. The

average direct asking lease rate was $28.04 per sq.

. full service gross (FSG), an increase of 2.7%

year-over-year. Investment sales activity increased

by 87.6% year-over-year, with transaction volume

reaching $72.8 million through H1 2017.

25

26

27

28

8

9

10

11

Q2 2016

Q3 2016

Q4 2016

Q1 2017

Q2 2017

Direct Vacancy Rate (%)

Direct Average

Lease Rate

Per Sq. Ft. ($)

Direct Vacancy Rate

Direct Average Lease Rate

Source: CBRE Research, Q2 2017.

*Arrows indicate change from previous half year.

• Direct vacancy decreased to 9.4% in Q2 2017,

down 96 bps year-over-year.

• Year-to-date net absorption totaled 137,063

sq. ft. in H1 2017, which helped bring down

the overall vacancy rate to 9.4%.

• Availability of 12.2% decreased 57 bps from

the previous six-month period.

• In H1 2017, 128,351 sq. ft. of medical ofce

space was completed in ve buildings with 74%

of the space preleased.

Figure 1: Vacancy Rate vs. Lease Rate

Lease Rate

$28.04 FSG

Denver Medical Ofce, H1 2017

Medical ofce remains an

attractive niche