8 / 32

8 / 32

Page 8

— Retail Properties Quarterly — May 2015

D

uring first-quarter 2015, the

overall leasing market, and

specifically the retail leasing

market in Colorado Springs,

gave positive signals for the

future.Turner Commercial Research

reports that total absorption of office,

retail and industrial space for first-

quarter 2015 was 237,425 square feet

– a 79 percent increase compared with

first-quarter 2014’s total absorption of

132,307 sf.Total absorption in 2014 was

528,645 sf, so more than half of the

total absorption from all of last year

took place in first-quarter 2015.That is

a good and much needed positive indi-

cator for the Colorado Springs market.

Retail absorption accounted for

21,559 sf of the total absorption report-

ed.That it is a very positive sign for the

Colorado Springs economy. Histori-

cally the retail sector posts a negative

absorption number in the first quarter

of the year because struggling retail-

ers will stay open through the holiday

season to harvest those high sales

figures then close the business early in

the new year. Because of this, normally

retail creates a higher-than-average

increase in vacated space in the first

quarter annually.

Total leasing activity of all categories

over the first quarter was 582,779 sf.

Retail leasing accounted for 182,165 sf,

which beat leasing numbers from the

first quarter of last year by 52,600 sf.

The combined vacancy rate of office,

retail and industrial fell 0.2 percent in

first-quarter 2015, dropping from 10.8

to 10.6 percent overall.The vacancy rate

in retail stayed about the same as it

was at year-end 2014 at 10.4 percent for

all retail centers.The market is still see-

ing continued prog-

ress from a year ago,

as the retail vacancy

rate for all centers

in first-quarter 2014

was 11.5 percent.

Colorado Springs

saw a 1.5 percent

decrease in vacancy

rate of anchored

shopping centers

between first-quar-

ter 2014 and the

same period in 2015.

The vacancy rate fell

from 7.1 percent to

where it currently

sits at 5.6 percent.The southeast quad-

rant recorded a 10 percent reduction in

vacancy of anchored centers over the

same period.

Nonanchored shopping centers

showed a slight year-to-year difference

in vacancy rate, as it was 1 percent

lower in 2015. However, the overall

vacancy rates are much higher in these

centers – 18.4 percent in 2014 and 17.4

percent this year.The northwest sector

of the market had a 9 percent decrease

in vacancy of nonanchored shopping

centers year to year.

As mentioned in the previous Colo-

rado Springs market update, specific

shopping centers and certain retail cor-

ridors may have higher vacancy rates

than the averages. However, there is a

positive change in retail leasing activity

in Colorado Springs that has occurred

since the end of last year.

Signs of improvement are visible at

several shopping centers throughout

the city – new tenants have opened up

in long-vacant spaces, tenant finish is

in process and new owners are mak-

ing improvements to common areas

of shopping centers. Making headway

on the absorption of retail space in

Colorado Springs is an important indi-

cator that the market may be on its

way to catching the wave of economic

improvement that already has graced

the metro area of Denver and the

Northern Front Range.

Sales prices of retail properties in Col-

orado Springs also have increased since

last year.Turner Commercial Research

said that 73 retail properties sold for an

average price of $98.71 per sf in 2014

and 15 properties sold at an increased

average price of $122.89 per sf in first-

quarter 2015. Adjusted retail property

sales have hovered around the $100

per-sf mark for the past two years.

Speaking with appraisers in the

market, capitalization rates on retail

properties have averaged 8 percent

on anchored, occupied shopping cen-

ters. Appraisers said that cap rates are

somewhat lower for special properties,

although not much lower, and cap

rates are higher for unanchored and

more vacant properties.

When the current cap rates are com-

pared with the 6 percent and lower

rates that are common in Denver and

other markets throughout the country,

Colorado Springs retail investment

properties continue to represent an

opportunity for investors of all descrip-

tions.

Construction of all types always

drives any economy toward improve-

ment. Generally and historically, com-

mercial construction lags residential

construction. In Colorado Springs,

residential construction was surpris-

ingly flat in 2014 and is not forecast

to improve much in 2015. Engineering

News Record forecasts a slight, 1.5 per-

cent increase in residential construc-

tion in 2015 in Colorado Springs. Build-

ers and suppliers of residential con-

struction products also agree with this

First-quarter 2015 numbers up across the boardColorado Springs Update

Jay Carlson

Managing broker

and co-founder,

Front Range

Commercial,

Colorado Springs

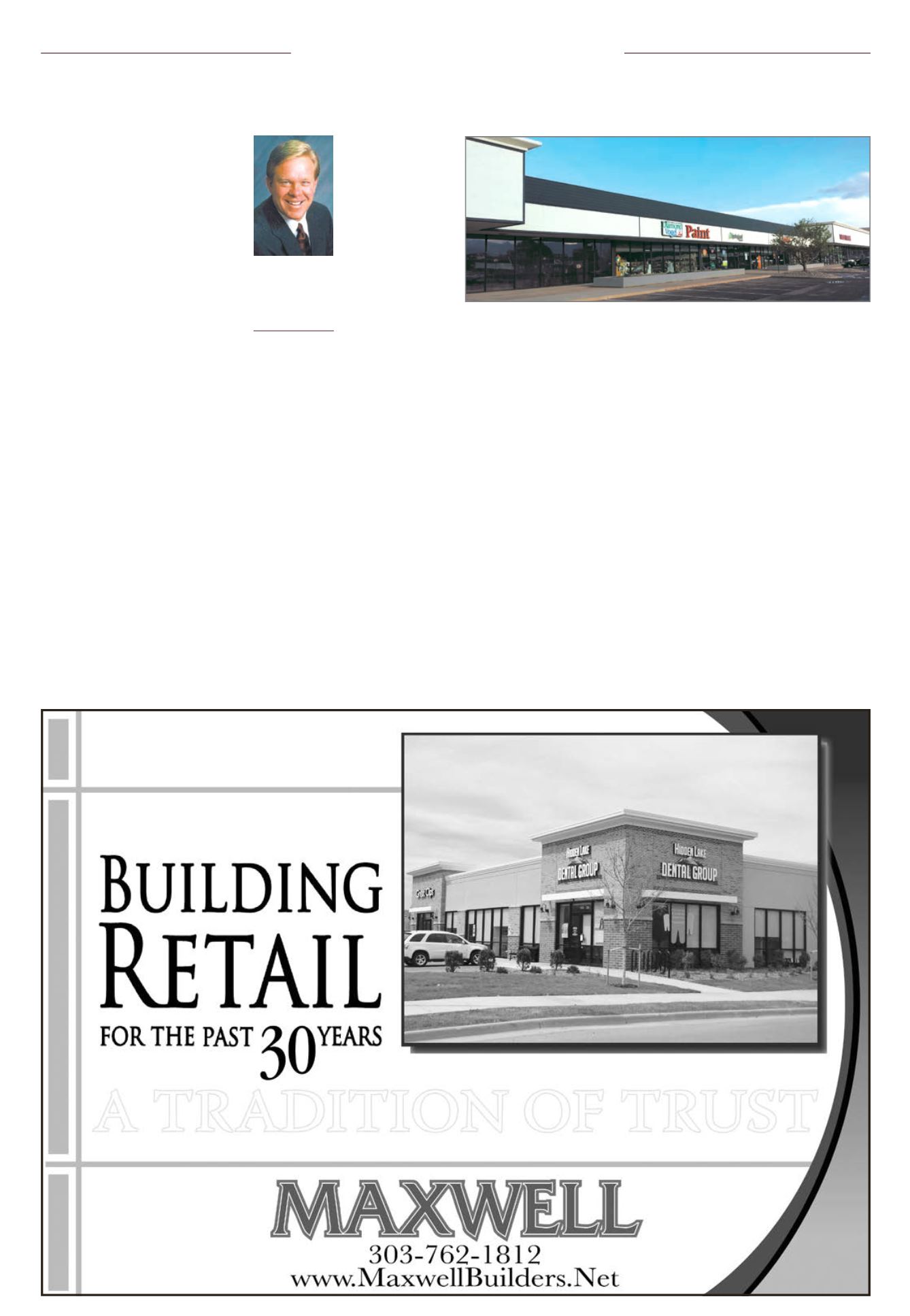

A new color scheme and architectural finishes at Center Point attract new tenants like

Diamond Vogel Paint.

Please see ‘First-Quarter,’ Page 27