Page 4

— Property Management Quarterly — July 2016

Colliers International | Denver Property Management team has

a proven track record of adding value to commercial real estate

assets. Our approach to property management is unique to our

industry. We have identified the subtle drivers that enable us to

manage property at a higher standard and maximize asset value.

BRAD CALBERT

303 283 4566

4643 South Ulster Street

|

Suite 1000

|

Denver, CO 80237

|

303 745 5800

|

303 745 5888 fax

INDUSTRIAL

|

FLEX

|

RETAIL

|

OFFICE

|

MEDICAL

A step above the rest.

BOB MILLER

303 283 4577

A

ll you have to do is look at

the cranes dotting the sky-

line from Boulder to the

Denver Tech Center to see

that Denver has a thriving

real estate market. Real estate trans-

actions are plentiful and prices have

reached record highs in the last few

years. Office space vacancy rates

have stabilized, rental rates have

increased and capitalization rates

have stabilized. All of which are nec-

essary for a thriving real estate mar-

ket. With all of the positives in the

real estate market, there are down-

sides to owners and building tenants

– property taxes have risen.

Property taxes are a function of

market value and the mill levy. In

Colorado, all properties are reap-

praised every two years on Jan. 1

of the odd year. Since the Great

Recession, starting in 2013, average

property values have increased. The

largest increase was in 2015 when

assessors had more transactions to

review than they’d had in the past

to set market values for the 2015

reappraisal. Additionally, sale prices

pointed to increased property val-

ues.

The mill levy is the second fac-

tor in determining property taxes.

The mill levy is made up of city and

county services such as the general

fund, bond repayment, social ser-

vices, police and fire, and capital

maintenance. These services make

up a little less than half of the mill

levy and the school districts make

up the remainder of the levy. Some

properties are located in special

districts that have

additional mills for

operations, bond

interest and repay-

ment.

Legislative

Tax Policies

There are sev-

eral legislative

tax policies that

impact the mill

levy. First is the

Taxpayer Bill of

Rights, also known

as the TABOR

amendment, that says state and

local governments cannot raise tax

rates without voter approval and

cannot spend revenues collected

under existing tax rates if revenues

grow faster than the rate of popula-

tion growth and inflation, without

voter approval. Revenues in excess

of TABOR limits are refunded to

taxpayers unless taxpayers vote

to allow governments to keep the

surplus. Through 2012, 85 percent

of Colorado’s local jurisdictions had

received voter approval to remove

some or all of the revenue limits set

by TABOR.

Second is Tax Measure 2A, passed

in the city and county of Denver

in 2012. The measure permanently

removed TABOR restrictions on the

city’s tax base and eliminated four

credited mills with 2.22 credited

mills still in place. It implemented

an antispiking provision that pro-

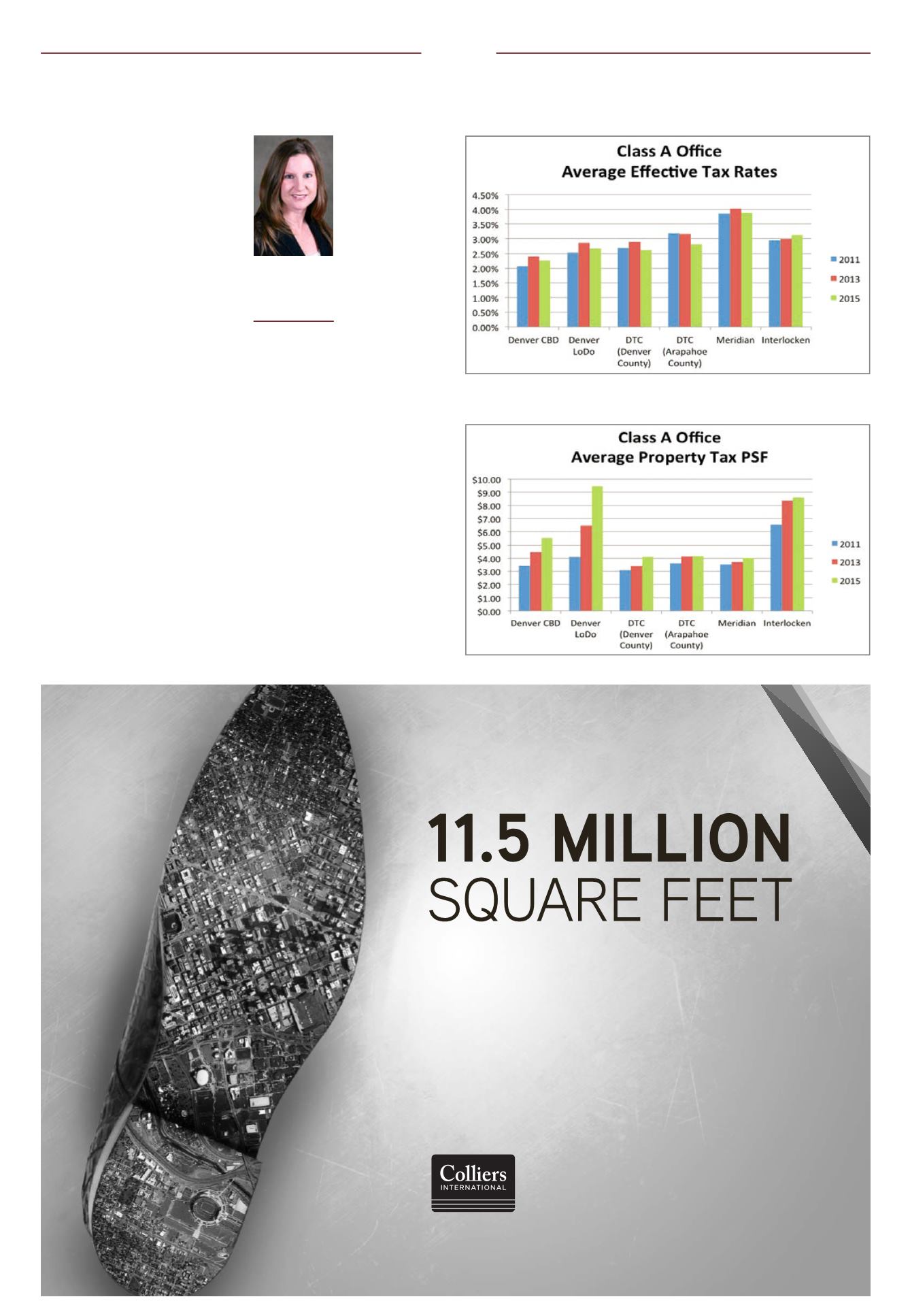

Taxes

Jodi Sullivan,

MAI, CCIM

Director, property

tax, Duff & Phelps

LLC, Denver

Data collected from Costar, Denver County Assessor Records, Arapahoe County Assessor

Records, Douglas County Assessor Records and Broomfield County Assessor Records.