June 2016 — Office Properties Quarterly —

Page 11

At North Forest Office Space, we make leasing easy.

We offer affordable lease rates and guaranteed pricing with no hidden costs and upscale amenities.

Your clients can lease what they need today, and then add space as they grow.

Professional, medical and dental space in Brighton, Commerce City, Westminster, Firestone & Thornton • (303) 862-6367 •

DENVER • BUFFALO • ROCHESTER • AUSTIN

Offer your clients

office space

that grows

with them.

Market Drivers

because they don’t adjust for pres-

ence factor (i.e., the percentage of

employees who many not drive to

work on a given day or may not be

present at peak hours due to meet-

ings, paid time off, travel and tele-

commuting). Also, employers often

underestimate the impact of transit

use and other transportation alterna-

tives on parking needs, especially in

markets where monthly parking rates

are high. It’s a mistake to assume that

all employees want to drive to work

or can afford to do so.

In many markets, an increase in

employee density does not necessar-

ily lead to a need for more parking

spaces. Many of the industries men-

tioned above as candidates for higher

density are also the same industries

that attract younger, more urban and

more progressive employees.

In markets like Denver, it is typical

to expect drive-to-work numbers in

the range of 30 to 40 percent within

the downtown core, largely because

much of the available monthly park-

ing is expensive. For example, an

unreserved permit sells for roughly

$190 a month. Meanwhile, transit

alternatives are plentiful as is the

availability of new housing options

located within walking or biking dis-

tance.With so many alternatives for

getting to work and a healthy market

for competing commercial parking,

it doesn’t make sense to build to a

very high ratio for new construction,

regardless of the projected density of

the building.

Outside of the downtown core,

much of the new and proposed office

building development is occurring at

transit-oriented locations such as the

River North neighborhood, Belleview

Station, Orchard, the Fitzsimons cam-

pus, and along the new RTD lines

servicingWestminster, Lakewood

and Aurora. At these station areas,

some owners may be considering the

option of developing higher-density

buildings and must decide whether

they should park these buildings at a

high ratio. They should keep in mind

that high parking ratios often lead to

more surface parking spaces and less

density overall. This tends to coun-

teract the effect of being at a location

that is transit adjacent.

Many developers that are experi-

enced with urban infill and transit-

oriented development projects are

seeking to park office buildings at a

lower ratio with a plan to share this

parking with a mix of evening and

nighttime uses. An example would

be One Belleview Station, which,

at build-out, is expected to have a

mix of residential, office and retail

on a relatively dense infill footprint;

the overall parking ratio provided is

around 2.5:1,000.

At this and similar TOD locations,

a lower ratio of parking spaces com-

bined with appropriate parking poli-

cies – car share, eco pass, bike facili-

ties on site and pay parking – can

allow the development to function

effectively. Tenants for this type of

development generally are aware that

there will be less parking available

than at a more suburban location,

and their employees typically value

having access to transit and a mix of

on-site uses over plentiful parking.

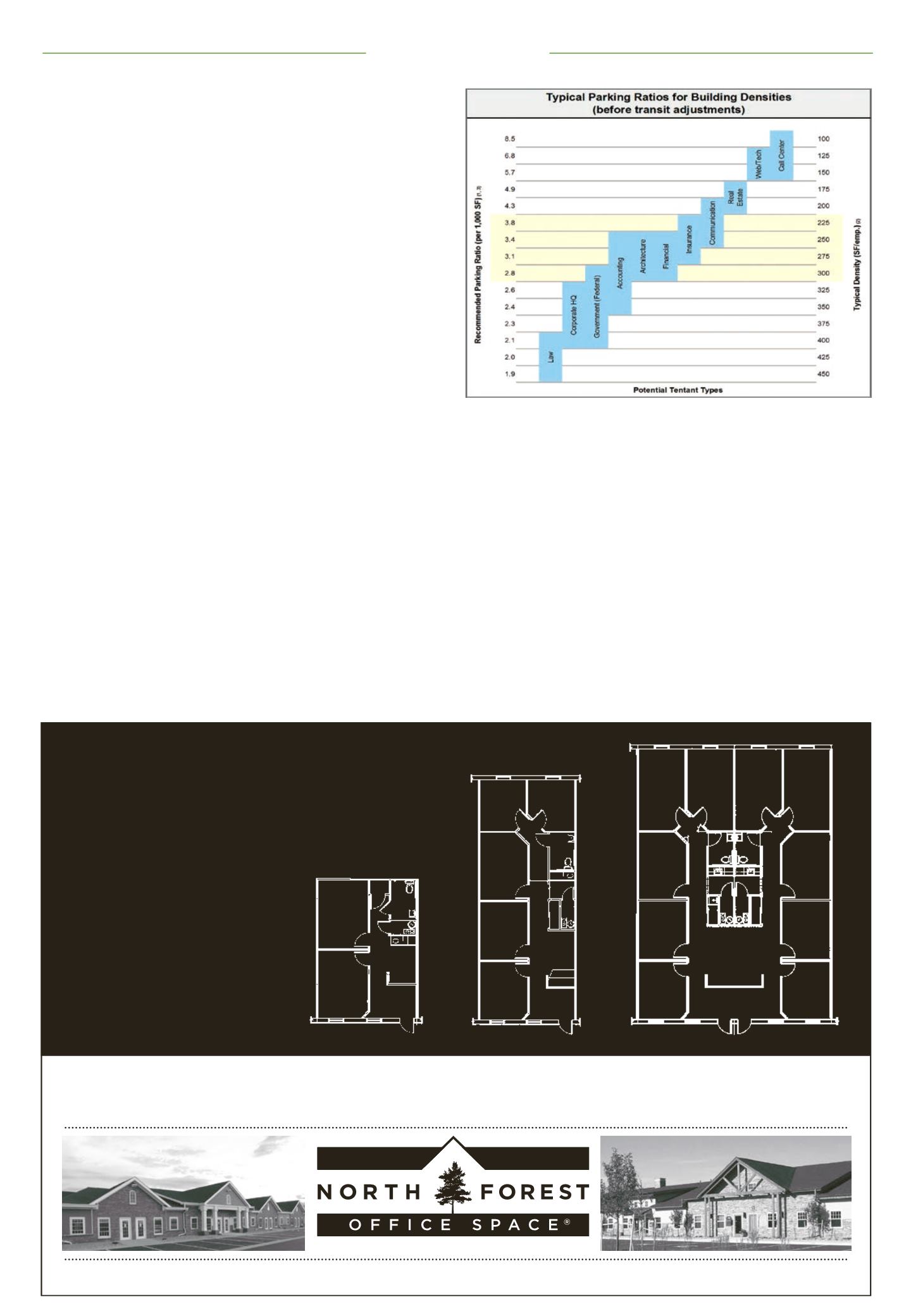

According to the Urban Land Insti-

tute, the typical parking demand

generation rate for office is 2.55 to

3.55 spaces per 1,000 sf, based on the

building size and density. Background

research from the Institute of Traf-

fic Engineer’s (Parking Generation,

4th Edition), confirms that this ratio

should be enough to satisfy parking

for up to at least the 95th percentile

in terms of potential building densi-

ties. This statistic excludes medical

office buildings, which have a higher

need for parking than typical offices.

Evidence suggests that office build-

ing densities are increasing and some

in the industry argue that this should

mean that more parking spaces are

required for new buildings. However,

due to the trends in office build-

ing development, TOD projects and

the needs of younger employees, it

might prove shortsighted to build

more parking for offices as a default.

Instead, owners and developers

should work with their consultants to

approach each site as a new location

and find a parking ratio that is a right

fit for that building type, keeping in

mind density, local alternatives and

the impact of transit on the site.

In addition, developers working in

today’s environment need to be aware

of trends in technology that may

change the way the industry views

parking and access. Technologies

such as driverless vehicles, the rise of

Uber and Lyft, car sharing and other

services are all trends to watch when

planning for new buildings.

Does a plan for building density

make sense when considering the

parking supply? Absolutely. But is

6:1,000 sf the right parking ratio for

higher-density offices? In many cases,

I would suggest considering all the

alternatives before building to a ratio

that may not be needed in the near

future.

s

Walker Parking Consultants

Typical industry-average parking demand ratios and building densities are shown

above. The range recommended by Urban Land Institute for new buildings is highlighted.