Page 10

— Office Properties Quarterly — June 2016

A Different Approach to Denver Commercial

Real Estate Solutions and Services

In a partnership focused on your strategic business objectives, Avison Young

delivers intelligent commercial real estate solutions that add value and build

competitive advantage for your enterprise.

Our office offers a full range of real estate solutions:

• Leasing and sales brokerage

• Property management

Learn how our approach might help you at:

Partnership. Performance.

For further information

please contact:

AlecWynne,

Principal, Managing Director

720.508.8112

• Project and construction management

• Lease administration

D

enver consistently is ranked

as one of the best places to

live and work. Our economy

is growing and vibrant,

population and employ-

ment rates are rising and the real

estate market is booming. Our state

attracts large employers due to the

strength of its economy as well as a

highly educated and growing work-

force. Denver is a hub for innova-

tion and entrepreneurship and has

been named one of the best places

for business and careers. The life-

style and recreational opportunities

offered in Colorado enable com-

panies to retain top talent as they

grow. While Denver is ideally posi-

tioned for continued office develop-

ment, one of the byproducts of our

strong economy and commercial

real estate boom is a steady increase

in office construction costs.

Historical inflation of materi-

als and building costs is estimated

at about 2 to 2.5 percent annually.

However, in the past six months, the

cost of developing office space in the

area has increased noticeably. What

are some of the key factors driving

this increase, and how can develop-

ers successfully deliver new office

facilities in this increasingly com-

petitive landscape?

Contributing factors.

When the

real estate market suffered dur-

ing the recession, many tradesmen

left the construction and develop-

ment industry, and the skilled labor

workforce was significantly con-

solidated. As the economy became

more robust and the commercial

construction industry strengthened

in Denver, subcontractors began

experiencing an imbalance between

the volume of work

and the size of

today’s qualified

workforce, signifi-

cantly driving up

the cost of office

development. This

is compounded

by the increased

demand for resi-

dential develop-

ment to accom-

modate the new

jobs resulting from

Denver’s growing

economy, further

adding to the need for subcontrac-

tors.

The continued investment

in major public improvements

strengthens our economy, such

as the expansion of Interstate 70

and the FasTracks transit program,

including the opening of the com-

muter rail to the airport. While these

public improvements are enormous-

ly beneficial for our community, they

strain the capacity of the construc-

tion community to manage public-

and private-sector work.

There was a notion that labor

costs would plateau or decrease due

to returning labor from the oil and

gas industry, but this has not widely

occurred – in part because of the

variance in wages for the oil and

construction trades as well as differ-

ences in specialties and experience.

The industry is not experiencing

savings from the lower commodity

costs of key construction materials.

While the costs of steel and oil have

decreased, we haven’t seen those

savings translate into the stabiliza-

tion of construction prices in the

local market. In fact, research indi-

cates that commodity prices actually

increase when the real estate mar-

ket is performing well.

Additionally, land value plays a

major factor in elevated office devel-

opment costs. The cost per buildable

square foot has increased from pre-

vious cycles by $10 to $30, depend-

ing on location. Land value in the

Denver metro area has nearly dou-

bled in some areas due to inflation,

improvement of the local economy

and, subsequently, the increased

buying power of tenants to afford

higher rent. Increased development

in other sectors, like multifamily,

also has influenced higher land

prices, which in turn affects office

development.

Parking, which often is a major

consideration for employers, is

noticeably more expensive for both

above-grade and subgrade options.

When compared to costs from past

cycles, above-grade parking in down-

town Denver increased by approxi-

mately $4,000 to $9,000 per stall and

subgrade parking increased by about

$10,000 to $20,000 per stall. With the

cost of parking being highly depen-

dent upon the location of the proj-

ect and the efficiency of each stall,

strategic design is critical and can

Marshall Burton

President and

CEO, Confluent

Development,

Denver

Market Drivers

Britt Nemeth

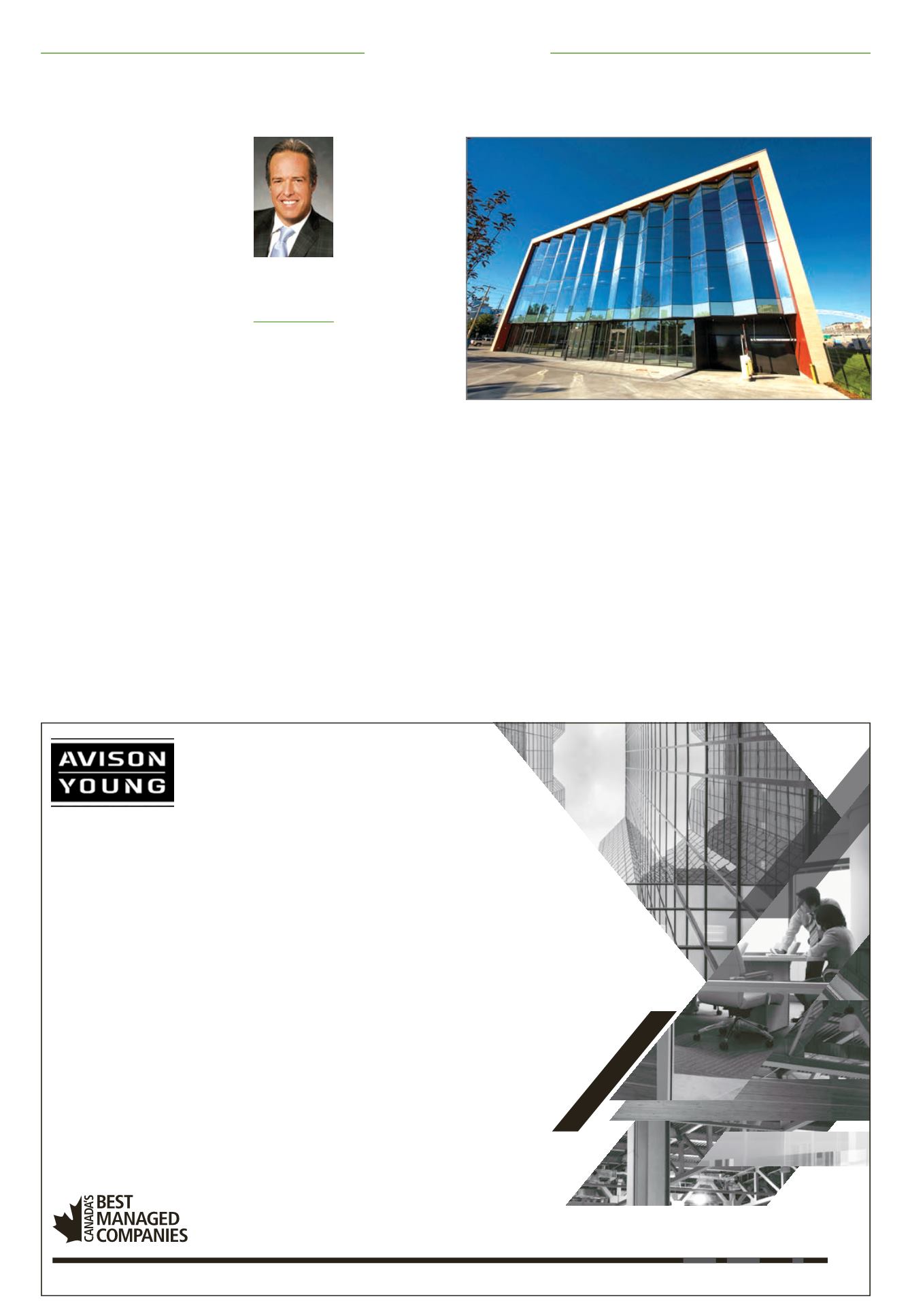

When done right, building in today’s competitive environment still makes sense. For

example, the LAB, co-developed by Confluent Development and Brue Capital Partners,

recently won NAIOP’s Innovative Project of the Year award.