Page 22 —

COLORADO REAL ESTATE JOURNAL

— September 21-October 4, 2016

Finance

Holliday Fenoglio Fowler LP

secured a $16.35 million refi-

nancing for Rangeview IV, an

82,381-square-foot, single-tenant

office building in Loveland.

Working on behalf of the bor-

rower, RVAA LLC, an affiliate

of McWhinney, HFF placed the

15-year, fixed-rate loan with Vec-

tra Bank (Zion’s Bancorp). Ear-

lier in the year, HFF worked on

behalf of an affiliate of McWhin-

ney to arrange $25.99 million in

construction financing through

Vectra Bank for the development

of the adjacent property, Ran-

geview V.

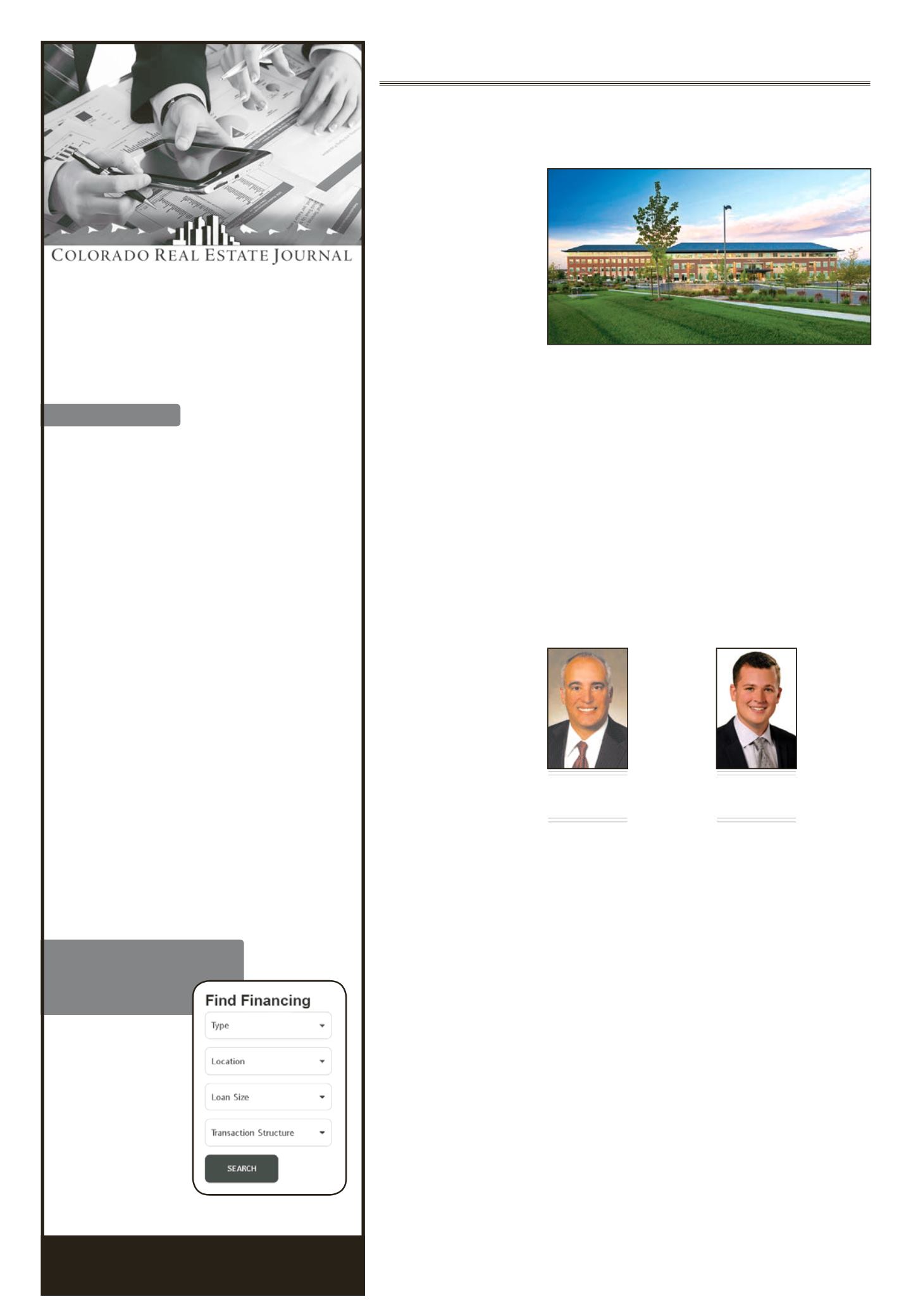

Completed in 2010, Rangeview

IV is a Class A office building

located in Centerra, a 3,000-acre

master-planned community at

Interstate 25 and U.S. Highway

34. The building is fully leased

to Agrium Inc., a major distribu-

tor of crop inputs and services

in North America, South Amer-

ica and Australia, and a leading

global producer and marketer of

agricultural nutrients.

The location serves as the

national headquarters for Agri-

um’s U.S. retail operations and

operates as Crop Production

Services. Rangeview IV has easy

access to Interstate 25 and is

within close proximity to the

Fort Collins/Loveland Airport

and Colorado State University,

a leading agricultural school

and a large recruitment base for

Agrium.

The HFF debt placement team

representing the borrower was

led by Senior Managing Director

Eric Tupler and Associate Direc-

tor Brock Yaffe.

“The financing provided by

Vectra was well-structured as a

competitive market interest rate,

fixed via a SWAP for the full term

of the loan, which is commensu-

rate with the term of the lease,

and will enable us to optimize

long-term recurring cash flow at

a very attractive cost of capital,”

said Joshua Kane, vice president

of finance for McWhinney.

s

Rangeview IV serves as the national headquarters for Agrium’s U.S.

retail operations, which operates as Crop Production Services.

C

ommercial mortgage-

backed securities have

long been a source for

high-leverage financing of real

estate assets that did not qualify

for more friendly balance sheet

financing executions. In the lat-

est real estate cycle, CMBS has

become a black sheep lending

source. According to Commer-

cial Mortgage Alert, the first half

of 2016 saw $30.7 billion of total

transaction volume. This repre-

sents an approximate 43 percent

decline in transaction volume

from the first half of 2015. As

borrowers continue to see CMBS

as a last-ditch effort for financ-

ing, it is expected that transac-

tion volumes will continue to

decline.

Further complicating this pro-

cess is the implementation of risk

retention, which is the final act

of the Dodd-Frank Wall Street

Reform and Consumer Protec-

tion Act of 2010. The new rule

will go into effect Dec. 24, and

was designed to discourage reck-

less mortgage-backed security

lending that was a large contrib-

utor to the financial catastrophe

seen in 2008. All conduit trans-

actions sold after Dec. 24, 2016,

must comply with risk retention

regulations. Major CMBS issu-

ers have scrambled to determine

how to implement risk retention

into their programs and how it

will affect the pricing of conduit

deals going forward.

Risk retention requires the

issuer, or major affiliate of the

issuer (B-piece buyer), of CMBS

bonds to hold a 5 percent piece

of the securitization on its bal-

ance sheet for the initial five

years of the bond’s life. There are

two main methods to structure

this risk retention, an “eligible

vertical risk piece” and an “eli-

gible horizontal risk piece.”

Vertical risk piece.

The spon-

sor or issuer of the CMBS trans-

action

is

required to

retain 5 per-

cent of the

face

value

of each class

of securities

issued in the

CMBS trans-

action.

Horizontal

risk piece.

The sponsor

is required

to retain the

most subordi-

nate class or classes of securities

issued in the CMBS transaction

in an amount equal to 5 percent

of all the “fair value” of all the

CMBS transactions issued. This

form of risk retention is more

commonly known as the B-piece

buyer retention option.

Hybrid risk piece.

A final

hybrid structure permits the

sponsor to satisfy the risk reten-

tion requirement by a combina-

tion of horizontal and vertical

retention, knownmore common-

ly as the “L” slice. This provision

would allow CMBS sponsors

to supplement the horizontal

piece by retaining themselves, or

through a B-piece buyer affiliate,

an additional vertical interest to

“top off” the amount by which

the securities retained in the hor-

izontal risk piece falls short of

the required fair market value.

Similar to the vertical risk piece

method, the sponsor would be

required to retain a portion of

the CMBS bond that represents

an interest in each class of the

CMBS, including an interest in

the class or classes retained by

the B-piece buyer.

The legislation further states

that a sponsor cannot retainmore

than its pro rata share (based on

collateral contributed) of the risk

retention obligation, nor may

any originator retain less than

20 percent of

the sponsor’s

risk retention

ob l i ga t i on .

T h e r e f o r e ,

sponsors who

c o n t r i b u t e

less than 20

percent of the

collateral for a

CMBS trans-

action are not

permitted to

retain any of

the required

risk piece. What this means in

the market is that smaller CMBS

originators who contribute to

larger CMBS pools will not be

able to retain any portion of the

required risk piece and will like-

ly see more expensive pricing

from the main book runners in

order to cover the cost of risk

retention. This cost will then be

passed on to the borrower in

the form of wider interest rate

spreads.

In early August, the first con-

duit transaction to comply with

the risk retention regulationswas

priced in the market. The $870.6

million transaction was led by

Wells Fargo, Bank of America

and Morgan Stanley. The three

book runners chose to retain a

vertical risk retention piece total-

ing approximately $43.5 million.

The 10-year AAA tranche priced

at SWAPs+94 basis points, with

the BBB- tranche pricing at

SWAPs+425 basis points. This

pricing presented the tightest

spreads seen in a conduit trans-

action in 2016. Though some

of this favorable pricing was

driven by larger market factors,

including a lack of recent CMBS

supply, this pricing also proves

investors’ confidence in the abil-

ity of major national banks to

navigate risk retention and sup-

Eric Tupler

Senior managing

director, HFF, Debt &

Equity Team, Denver

Tyler Dumon

Real estate analyst,

HFF, Debt & Equity

Team, Denver

FIND FINANCING

I N D U S T R Y D I R E C T O R Y

COMMERCIAL REAL ESTATE

LENDERS

Arbor Commercial

Mortgage, LLC

Bank of America Merrill

Lynch – Commercial

Real Estate

Bank of Colorado

Bank of the West

Berkadia Commercial

Mortgage, LLC

Bloomfield Capital

Partners, LLC

CBRE|Capital Markets

Chase Commercial Term

Lending

Citywide Banks

Colorado Business Bank

Colorado Lending Source

Commerce Bank

Essex Financial Group

Fairview Commercial Lending

FirstBank Holding Company

Front Range Bank

Grandbridge Real Estate

Capital LLC

Hunt Mortgage Group

JCR Capital

JVSC-CBRE Capital Markets

KeyBank N.A., KeyBank Real

Estate Capital

Merchants Mortgage and

Trust Corp.

Midland States Bank

Montegra Capital Resources,

Private Lender

Mutual of Omaha Bank

NorthMarq Capital, Inc.

RNB Lending Group

TABS

TCF Bank

Terrix Financial Corporation

U.S. Bank – Commercial

Real Estate

Vectra Bank Colorado, N.A.

Westerra Credit Union

@

EASY LENDER

SEARCH TOOL

profiles

photos

contacts

social links

videos

and more

GET LISTED

Jon Stern | 303-623-1148