Page 6AA —

COLORADO REAL ESTATE JOURNAL

— September 2-September 15, 2015

Self-Storage

L

ooking back over the

first half of 2015, self-

storage owners are

basking in their own glory and,

in general, self-storage proper-

ties continue to improve while

the Front Range market fun-

damentals remain as strong as

ever. It is time to look into the

crystal ball and examine the fac-

tors that will influence the self-

storage market in 2016.

There has been a 100 to 250

basis point compression in

cap rates over the last 12 to 36

months, andwe have seenmany

of the most aggressive national

buyers focusing on Denver for

new acquisitions. This largely is

due to Denver’s strong popula-

tion and job growth over the

last few years. This aggressive

pricing, along with the overall

lack of self-storage properties

for sale, is driving self-storage

values to record highs. This may

be as good as it gets!

Please forgive our optimism,

but we think that self-storage

fundamentals are strengthen-

ing along the Front Range, and

new supply is slow in coming.

The cost of new development

is rising at a

s t a g g e r i n g

pace. This,

paired with

a long and

cost-intensive

a p p r o v a l

process,

is

making new

self-storage

d e v e l o p -

ments more

challenging

and valuable

than ever.

Prices have

never been higher for self-stor-

age properties, either in abso-

lute dollars or in relation to the

income the properties produce.

This is driven by the lack of

quality product on the market

for sale (simple supply and

demand), newly found pub-

lic awareness and low interest

rates. It is worth noting, howev-

er, that not every market across

the nation is experiencing the

same uptick in value or lack

of sales velocity. This largely is

due to the increased intelligence

of the self-storage investment

community. Self-storage inves-

tors today are

focused on

market-spe-

cific demand

drivers, such

as migration

of popula-

tion, popula-

tion growth,

barriers

to

entry, income

growth levels

and employ-

ment basis.

It is fair to

say that we

have two distinct markets with-

in the self-storage investment

world, and we are not talking

about the top 50 metropolitan

statistical areas and rest of the

markets. We learned that small

and midsize markets could

be productive investments if

the demand drivers are pres-

ent. This is the case in markets

such as Greeley, Fort Collins

and Castle Rock. These mar-

kets enjoy strong rental veloc-

ity, rental rate growth, popu-

lation growth, income growth

and, most importantly, demand

growth for self-storage.

But before you get too excited

about the Colorado self-stor-

age market and our continued

prosperity, there are a few dark

clouds on the horizon. The first

is that interest rates may go up

in a meaningful way. The Fed-

eral Reserve has been trying to

justify raising rates for close to

a year, and self-storage doesn’t

have a government-subsidized

debt program that other prop-

erty types enjoy.

The second issue is overbuild-

ing; you guessed it, develop-

ment is back! The great returns

drew a crowd. We are in the

beginning stages of the develop-

ment cycle, but strong growth

markets, such as Colorado, are

seeing as much as 5 to 25 per-

cent new supply in the devel-

opment pipeline and readying

to come on line. Because self-

storage is a localized business,

new development and potential

overbuilding can have a drastic

effect on the market. There is

a finite number of self-storage

customers that exist in any sta-

bilized market and new devel-

opment won’t bring any new

customers into that market – it

will only take existing custom-

ers away from other operators,

leading to an overbuilt situa-

tion. A new self-storage build-

ing in and of itself doesn’t create

any new demand for the prod-

uct within a specific 3- to 5-mile

market.

Lastly, industry experts Self

Storage Data Services report

that the Denver-Aurora MSA

is at equilibrium with 6.57 rent-

able square feet per person.

The national average is 6.5 sf

per person. Current population

growth should offset additional

supply in the near term, but

there are concerns about the

potential for an overbuilt situa-

tion to develop.

Self-storage owners and inves-

tors’ ability to properly evaluate

the future demand and current

market is the most important

part in making the right invest-

ment decision. These absolutely

are the best times in self-storage

for careful buyers and sellers.

The prize will go to those who

analyze their competitive situa-

tion and take action during this

unique time in the self-storage

real estate cycle.

s

Joan Lucas

President, Joan Lucas

Real Estate Services,

Denver

Ben Vestal

President, Argus

Self Storage Sales

Network, Denver

W

hile it may not

seem like a compat-

ible land use with-

in a large shopping center or

mixed-use residential and retail

development, adding self-stor-

age to the mix can help maxi-

mize site coverage and rentable

square footage for an overall

development.

While you wouldn’t want a

large storage property to be the

anchor tenant, less desirable

sections of the mixed-use plan,

as long as they still provide

some visibility, can be trans-

formed into valuable rentable

sf by incorporating self-storage

into the plan.

The primary driver for this

is the lower parking spaces

requirement of self-storage rel-

ative to other land uses. Using

the town of Parker as an exam-

ple, the retail parking require-

ment is 1:300, while the storage

parking requirement is 1:10,000.

Thus, a four-story, self-storage

building with a 25,000-sf foot-

print would

require

10

p a r k i n g

spaces and

about

an

acre of land.

A 25,000-sf

retail build-

ing would

require

83

parking spac-

es and the

a d d i t i o n a l

land

area

to

accom-

modate the

parking. In

other words,

10 parking spaces could sup-

port 3,000 sf of retail or 100,000

gross sf of self-storage.

Today’s self-storage has

evolved into a retail establish-

ment. New facilities can offer a

combination of traditional stor-

age, postal services, and sales

of moving and storage sup-

plies (i.e., locks, boxes and bub-

ble wrap) with contemporary

full-service

work stations

and confer-

ence rooms

catered

to

l o c a l - a r e a

b u s i n e s s e s

and

sales

reps. Gone

are the days

of

orange

doors

and

razor wire.

These older,

outdated self-

storage facili-

ties are being

r e p l a c e d

by modern, architecturally

advanced vertical structures.

In addition, many munici-

palities recognize the need for

the product to complement

high-density urban residential

developments. The new devel-

opment of a self-storage facility

often is viewed as an amenity

within communities that have

a significant amount of existing

residential units and commer-

cial businesses.

Today’s modern facilities

come with fully air-conditioned

buildings, carpeted hallways,

extensive video surveillance,

high-speed Internet access, and

the use of a free truck and

driver to help with the move-

in. Finally, the consumer has

come to recognize the benefits

of indoor, climate-controlled

space vis-à-vis the more tradi-

tional drive-up units. The dif-

ferences between the twowould

be similar to storing items in

a bedroom closet versus your

garage, the former being clean-

er and a better option for more

valuable goods.

s

Jon Suddarth

Real estate

development, project

manager, The William

Warren Group Inc.,

Denver

Tim Hobin

Executive vice

president, real estate,

The William Warren

Group Inc., Costa

Mesa, California

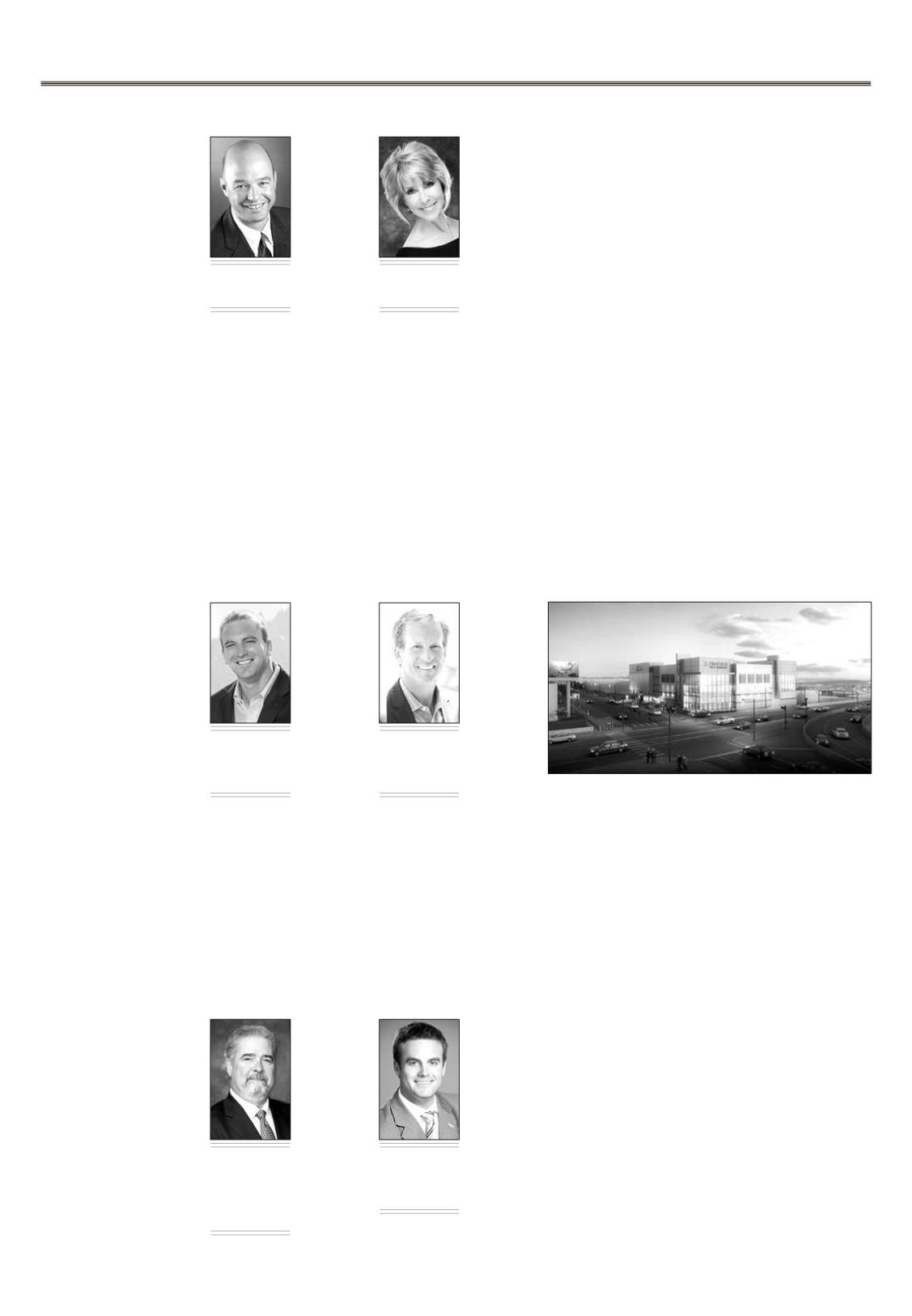

A rendering of a WilliamWarren Group development under construction

in Denver illustrates the architectural advancements in the self-storage

industry.

I

t’s hard to believe a niche

real estate sector that start-

ed out as nothing more

than a way to make a few bucks

on a land bank turned into one

of commercial real estate’s most

sought-after investments. But

that’s exactly what’s happened.

The self-storage industry is on

fire and everyone wants a piece.

An executive from one of the

nation’s largest self-storage real

estate investment trusts once

said that one day self-storage

cap rates would trade lower

than apartments. At the time

the statement raised some eye-

brows, but if that time isn’t

already here, it’s certainly close.

The Great Recession proved

the resiliency of the self-storage

sector as the “big four” publicly

traded REITs outperformed its

counterparts

in all the other

major

real

estate sectors.

You

won’t

find a better

risk-adjusted

return over

a five- to

10-year hold,

and every-

one

from

Wall Street to

investors here

in Denver has

taken notice.

As long as

people buy

stuff, there

always will be a need to store it

and, with the growth of the Den-

ver economy, it looks like we’ll be

seeing a lot more of both.

The market

for self-stor-

age is flush

with cash and

there

isn’t

enough prod-

uct to feed

the appetite.

The availabil-

ity of cheap

debt

and

high demand

has driven

values to a

place never

before seen

in the indus-

try. Fundamentals in Denver are

some of the best in the country,

posting 15 percent rental growth

over the trailing 12 months and

physical occupancies pushing

99 percent in many of the first-

and second-ring suburbs. Prices

per square foot have reached

a point where it makes more

sense to build than buy. Devel-

opers are scrambling to get as

much product out of the ground

as quickly as they can. Proj-

ects delivered across the Front

Range blew away traditional

lease-up projections. What used

to take 36 months to stabilize is

now taking under a year and,

in some cases, as little as eight

months. We’re currently track-

ing more than 50 projects in

various phases of planning and

development along the Front

Range, and the number contin-

ues to grow.

Many caution that we’ve seen

this before – seasoned self-stor-

age developers haven’t forgot-

ten about the 1990s, when the

Denver market was flooded

with new development leading

up to the savings-and-loan cri-

sis, or the mid-2000s to a lesser

degree. While you can draw

some comparisons between

these past two cycles and the

current one, there also are some

notable differences.

Financing for new self-storage

projects is cheap and available

but primarily is limited to sea-

soned operators, which makes

it challenging for new investors

to secure loans and enter the

market. In addition, officials at

the county and local levels are

making it difficult to obtain the

zoning and entitlements needed

for new self-storage projects.

Taking into account these fac-

Adam Schlosser

Vice president

investments, director,

National Self Storage

Group, Marcus &

Millichap, Denver

Charles “Chico”

LeClaire

Senior vice president

investments, senior

director, National

Self Storage Group,

Marcus & Millichap,

Denver